|

[#1]

Originally Posted By rfoxtrot: That's the part that gets me every time. Everyone focus on the rates alone.. Yet completely ignores the equity they are sitting on due to the run up in values. In many many cases it's six figures worth of equity. If where your at is doing what you want then great. But it's a bit short sided I think to sit parked delaying life and goals on account of a rate change. It's enough money in equity in many cases to completely change your life. We decided that most likely things weren't going to get cheaper around here. More likely it would just get more, way more expensive as time goes on. So we took the plunge. Best decision we've made yet. Originally Posted By rfoxtrot: Originally Posted By ride_the_lightning: It's strange to not be able to move because you are locked into a 2.5% APR despite having hundreds of thousands in equity That's the part that gets me every time. Everyone focus on the rates alone.. Yet completely ignores the equity they are sitting on due to the run up in values. In many many cases it's six figures worth of equity. If where your at is doing what you want then great. But it's a bit short sided I think to sit parked delaying life and goals on account of a rate change. It's enough money in equity in many cases to completely change your life. We decided that most likely things weren't going to get cheaper around here. More likely it would just get more, way more expensive as time goes on. So we took the plunge. Best decision we've made yet. rates matter because generally speaking if people want to move to a similar property they need that equity to purchase the new same house with same loan or bigger house with bigger loan so when the rates go up so does their mortgage payment unless they are moving to downsize. |

|

|

|

|

[Last Edit: exponentialpi]

[#2]

Those 20% rate increases are starting to sting. Those 20% rate increases are starting to sting.

|

|

|

|

|

[#3]

Originally Posted By exponentialpi: Those 20% rate increases are starting to sting.

Bold move cotton lets see how that plays out |

|

|

|

USA

|

[#4]

Bad week for doomers

Home resales, which account for a large portion of U.S. housing sales, fell 3.3% on a year-on-year basis in February. Despite the increase in supply, housing inventory is still well below the nearly 2 million units before the COVID-19 pandemic. Multiple offers remain in many areas, especially in the Northeast, and most of the houses sold last month were above the listing prices, Yun said. At February's sales pace, it would take 2.9 months to exhaust the current inventory of existing homes, up from 2.6 months a year ago. A four-to-seven-month supply is viewed as a healthy balance between supply and demand. Many homeowners have mortgages with rates below 4%, discouraging them from selling their houses, contributing to the supply crunch and higher home prices. The median existing home price increased 5.7% from a year earlier to $384,500 in February. Home prices increased in all four regions. Properties typically stayed on the market for 38 days in February, up from 34 days a year ago. First-time buyers accounted for 26% of sales, compared to 27% a year ago. That share is well below the 40% that economists and realtors say is needed for a robust housing market. All-cash sales made up 33% of transactions, up from 28% a year ago. Distressed sales, including foreclosures, represented 3% of transactions, virtually unchanged from last year. U.S. existing home sales increased to a one-year high in February as supply improved, a trend that together with retreating mortgage rates could support activity during the spring selling season. Home sales jumped 9.5% last month to a seasonally adjusted annual rate of 4.38 million units, the highest level since February 2023, the National Association of Realtors said on Thursday. The monthly increase in sales was also the largest since February 2023. Economists polled by Reuters had forecast home resales would fall to a rate of 3.94 million units. https://finance.yahoo.com/news/us-existing-home-sales-rise-140311081.html |

|

|

|

[#5]

Originally Posted By Silverbulletz06: Where did you come up with these numbers? Assuming a 2-3 inflation, the real cost on cash for loaned money at 7% would have a real rate of 4-5%. Historically, we are around average interest rates. Originally Posted By Silverbulletz06: Originally Posted By MikeMilligan: Am I expected to be angry about this. Money should cost money to borrow. 7% mortgage is a bit high; 5% mortgages are reasonable; 3% mortgages just encourage stupid behavior that wages will never keep up with. Where did you come up with these numbers? Assuming a 2-3 inflation, the real cost on cash for loaned money at 7% would have a real rate of 4-5%. Historically, we are around average interest rates. I’ve owned three houses over 25 years. I think my first mortgage was 7.5% or so and I was incentivized to refinance to 6 something; at which point I was satisfied. That’s my point-rates will always be screwed with and 7% is my unofficial pain number. That’s as scientific as any other statistic out there that isn’t based on actual historical returns. |

|

|

|

|

[#6]

Originally Posted By anothermisanthrope: Bad week for doomers https://finance.yahoo.com/news/us-existing-home-sales-rise-140311081.html Originally Posted By anothermisanthrope: Bad week for doomers Home resales, which account for a large portion of U.S. housing sales, fell 3.3% on a year-on-year basis in February. Despite the increase in supply, housing inventory is still well below the nearly 2 million units before the COVID-19 pandemic. Multiple offers remain in many areas, especially in the Northeast, and most of the houses sold last month were above the listing prices, Yun said. At February's sales pace, it would take 2.9 months to exhaust the current inventory of existing homes, up from 2.6 months a year ago. A four-to-seven-month supply is viewed as a healthy balance between supply and demand. Many homeowners have mortgages with rates below 4%, discouraging them from selling their houses, contributing to the supply crunch and higher home prices. The median existing home price increased 5.7% from a year earlier to $384,500 in February. Home prices increased in all four regions. Properties typically stayed on the market for 38 days in February, up from 34 days a year ago. First-time buyers accounted for 26% of sales, compared to 27% a year ago. That share is well below the 40% that economists and realtors say is needed for a robust housing market. All-cash sales made up 33% of transactions, up from 28% a year ago. Distressed sales, including foreclosures, represented 3% of transactions, virtually unchanged from last year. U.S. existing home sales increased to a one-year high in February as supply improved, a trend that together with retreating mortgage rates could support activity during the spring selling season. Home sales jumped 9.5% last month to a seasonally adjusted annual rate of 4.38 million units, the highest level since February 2023, the National Association of Realtors said on Thursday. The monthly increase in sales was also the largest since February 2023. Economists polled by Reuters had forecast home resales would fall to a rate of 3.94 million units. https://finance.yahoo.com/news/us-existing-home-sales-rise-140311081.html You neglected to quote some of the non-rosy propaganda: "Home resales, which account for a large portion of U.S. housing sales, fell 3.3% on a year-on-year basis in February." and "Properties typically stayed on the market for 38 days in February, up from 34 days a year ago." There's another part which is interesting: "First-time buyers accounted for 26% of sales, compared to 27% a year ago. That share is well below the 40% that economists and realtors say is needed for a robust housing market." I'm guessing that's more an indicator of the broader economy than home sales per se. |

|

|

|

|

[#7]

Originally Posted By anothermisanthrope: Bad week for doomers https://finance.yahoo.com/news/us-existing-home-sales-rise-140311081.html Originally Posted By anothermisanthrope: Bad week for doomers Home resales, which account for a large portion of U.S. housing sales, fell 3.3% on a year-on-year basis in February. Despite the increase in supply, housing inventory is still well below the nearly 2 million units before the COVID-19 pandemic. Multiple offers remain in many areas, especially in the Northeast, and most of the houses sold last month were above the listing prices, Yun said. At February's sales pace, it would take 2.9 months to exhaust the current inventory of existing homes, up from 2.6 months a year ago. A four-to-seven-month supply is viewed as a healthy balance between supply and demand. Many homeowners have mortgages with rates below 4%, discouraging them from selling their houses, contributing to the supply crunch and higher home prices. The median existing home price increased 5.7% from a year earlier to $384,500 in February. Home prices increased in all four regions. Properties typically stayed on the market for 38 days in February, up from 34 days a year ago. First-time buyers accounted for 26% of sales, compared to 27% a year ago. That share is well below the 40% that economists and realtors say is needed for a robust housing market. All-cash sales made up 33% of transactions, up from 28% a year ago. Distressed sales, including foreclosures, represented 3% of transactions, virtually unchanged from last year. U.S. existing home sales increased to a one-year high in February as supply improved, a trend that together with retreating mortgage rates could support activity during the spring selling season. Home sales jumped 9.5% last month to a seasonally adjusted annual rate of 4.38 million units, the highest level since February 2023, the National Association of Realtors said on Thursday. The monthly increase in sales was also the largest since February 2023. Economists polled by Reuters had forecast home resales would fall to a rate of 3.94 million units. https://finance.yahoo.com/news/us-existing-home-sales-rise-140311081.html That's one interpretation.... A more succinct one is that sales are down 4% since last year, which was already dead. Median sale price for Q1 23 vs Q1 24 is down ~3%. Inventory continues to climb despite being in peak season. Time on the market continues to climb. No rate relief is coming. The 5 D's never sleep (death, divorce, downsizing, diapers, diamonds) Unemployment continues to accelerate. California and several other states appear to already be in recession. There's this too:  |

|

|

|

USA

|

[Last Edit: anothermisanthrope]

[#8]

Originally Posted By planemaker: You neglected to quote some of the non-rosy propaganda: "Home resales, which account for a large portion of U.S. housing sales, fell 3.3% on a year-on-year basis in February." and "Properties typically stayed on the market for 38 days in February, up from 34 days a year ago." There's another part which is interesting: "First-time buyers accounted for 26% of sales, compared to 27% a year ago. That share is well below the 40% that economists and realtors say is needed for a robust housing market." I'm guessing that's more an indicator of the broader economy than home sales per se. Originally Posted By planemaker: Originally Posted By anothermisanthrope: Bad week for doomers Home resales, which account for a large portion of U.S. housing sales, fell 3.3% on a year-on-year basis in February. Despite the increase in supply, housing inventory is still well below the nearly 2 million units before the COVID-19 pandemic. Multiple offers remain in many areas, especially in the Northeast, and most of the houses sold last month were above the listing prices, Yun said. At February's sales pace, it would take 2.9 months to exhaust the current inventory of existing homes, up from 2.6 months a year ago. A four-to-seven-month supply is viewed as a healthy balance between supply and demand. Many homeowners have mortgages with rates below 4%, discouraging them from selling their houses, contributing to the supply crunch and higher home prices. The median existing home price increased 5.7% from a year earlier to $384,500 in February. Home prices increased in all four regions. Properties typically stayed on the market for 38 days in February, up from 34 days a year ago. First-time buyers accounted for 26% of sales, compared to 27% a year ago. That share is well below the 40% that economists and realtors say is needed for a robust housing market. All-cash sales made up 33% of transactions, up from 28% a year ago. Distressed sales, including foreclosures, represented 3% of transactions, virtually unchanged from last year. U.S. existing home sales increased to a one-year high in February as supply improved, a trend that together with retreating mortgage rates could support activity during the spring selling season. Home sales jumped 9.5% last month to a seasonally adjusted annual rate of 4.38 million units, the highest level since February 2023, the National Association of Realtors said on Thursday. The monthly increase in sales was also the largest since February 2023. Economists polled by Reuters had forecast home resales would fall to a rate of 3.94 million units. https://finance.yahoo.com/news/us-existing-home-sales-rise-140311081.html You neglected to quote some of the non-rosy propaganda: "Home resales, which account for a large portion of U.S. housing sales, fell 3.3% on a year-on-year basis in February." and "Properties typically stayed on the market for 38 days in February, up from 34 days a year ago." There's another part which is interesting: "First-time buyers accounted for 26% of sales, compared to 27% a year ago. That share is well below the 40% that economists and realtors say is needed for a robust housing market." I'm guessing that's more an indicator of the broader economy than home sales per se. Oh FFS if you're going to try and correct me you could at least read the first line quoted in my post. Now do supply and demand. |

|

|

|

[#9]

Originally Posted By anothermisanthrope: Oh FFS if you're going to try and correct me you could at least read the first line quoted in my post. Now do supply and demand. Inventory in FL is currently 98% of the Feb 2020 figure and trending up.

|

|

|

|

|

[Last Edit: hicap]

[#10]

I know you've heard it before, mortgages waere 12.75% in 1985, payment was around 950, I made $27K and wife made $19K.

|

|

|

|

|

[#11]

Originally Posted By anothermisanthrope: Oh FFS if you're going to try and correct me you could at least read the first line quoted in my post. Now do supply and demand. Originally Posted By anothermisanthrope: Originally Posted By planemaker: Originally Posted By anothermisanthrope: Bad week for doomers Home resales, which account for a large portion of U.S. housing sales, fell 3.3% on a year-on-year basis in February. Despite the increase in supply, housing inventory is still well below the nearly 2 million units before the COVID-19 pandemic. Multiple offers remain in many areas, especially in the Northeast, and most of the houses sold last month were above the listing prices, Yun said. At February's sales pace, it would take 2.9 months to exhaust the current inventory of existing homes, up from 2.6 months a year ago. A four-to-seven-month supply is viewed as a healthy balance between supply and demand. Many homeowners have mortgages with rates below 4%, discouraging them from selling their houses, contributing to the supply crunch and higher home prices. The median existing home price increased 5.7% from a year earlier to $384,500 in February. Home prices increased in all four regions. Properties typically stayed on the market for 38 days in February, up from 34 days a year ago. First-time buyers accounted for 26% of sales, compared to 27% a year ago. That share is well below the 40% that economists and realtors say is needed for a robust housing market. All-cash sales made up 33% of transactions, up from 28% a year ago. Distressed sales, including foreclosures, represented 3% of transactions, virtually unchanged from last year. U.S. existing home sales increased to a one-year high in February as supply improved, a trend that together with retreating mortgage rates could support activity during the spring selling season. Home sales jumped 9.5% last month to a seasonally adjusted annual rate of 4.38 million units, the highest level since February 2023, the National Association of Realtors said on Thursday. The monthly increase in sales was also the largest since February 2023. Economists polled by Reuters had forecast home resales would fall to a rate of 3.94 million units. https://finance.yahoo.com/news/us-existing-home-sales-rise-140311081.html You neglected to quote some of the non-rosy propaganda: "Home resales, which account for a large portion of U.S. housing sales, fell 3.3% on a year-on-year basis in February." and "Properties typically stayed on the market for 38 days in February, up from 34 days a year ago." There's another part which is interesting: "First-time buyers accounted for 26% of sales, compared to 27% a year ago. That share is well below the 40% that economists and realtors say is needed for a robust housing market." I'm guessing that's more an indicator of the broader economy than home sales per se. Oh FFS if you're going to try and correct me you could at least read the first line quoted in my post. Now do supply and demand. You mean supply being up and demand down? "Housing inventory surged 5.9% to 1.07 million units last month. It was up 10.3% from one year ago." |

|

|

|

|

[#12]

How old is this thread? Supply/demand. Better learn it.

|

|

|

|

|

[#13]

Originally Posted By Chromekilla: Bold move cotton lets see how that plays out Originally Posted By Chromekilla: Originally Posted By exponentialpi: Those 20% rate increases are starting to sting.

Bold move cotton lets see how that plays out Getting more attention. Insurance coverage is going to squeeze lots of people.

|

|

|

|

|

[Last Edit: spidey07]

[#14]

Originally Posted By exponentialpi: Getting more attention. Insurance coverage is going to squeeze lots of people.

Originally Posted By exponentialpi: Originally Posted By Chromekilla: Originally Posted By exponentialpi: Those 20% rate increases are starting to sting.

Bold move cotton lets see how that plays out Getting more attention. Insurance coverage is going to squeeze lots of people.

That’s why you don’t escrow. Let the fools get squeezed. They signed it. |

|

|

|

MS, USA

|

[Last Edit: Wildfowler]

[#15]

Originally Posted By exponentialpi: Getting more attention. Insurance coverage is going to squeeze lots of people.

Wife and I moved to some rural land four years ago and thought this is just what it was going to cost us. I'm making this as a public service announcement to anyone who reads this to please consider checking to make sure that what you were paying on your homeowners policy for fire protection service matches what your actual fire protection service rating is at your address. I just discovered that I was overpaying for fire protection service on a piece of land that my wife and I purchased five years ago and built a house and moved there 4 years ago. Anyway we were within a specific distance from the local volunteer fire department and I happen to have a fire hydrant at the end of my driveway which is less than 1000 feet from my home and this combined with the fact that my local volunteer department did some major upgrades to their facility a year or two before we moved means that I am in a better protection rating zone then I've been paying my insurance company. To the tune of four figures per year. So take a moment and review your policy and then contact your local insurance commissioners office to verify what your fire protection rating is at your residence and make sure it matches with what you were being charged for on your homeowners policy. |

|

|

|

[#16]

Originally Posted By hicap: I know you've heard it before, mortgages waere 12.75% in 1985, payment was around 950, I made $27K and wife made $19K. And electrical was about $20, wsg maybe 75 max. Car insurance probably $300 per year. Home insurance maybe $1000. Food maybe $500 a month for a family of 4. And maybe a down payment of 20% on a 95,000 house. |

|

|

|

|

[#17]

|

|

|

|

|

[#18]

Originally Posted By exponentialpi: Price cuts are increasing. Demand seems to be stagnant. https://www.ar15.com/media/mediaFiles/200878/IMG_3798_jpeg-3165856.JPG This matches my observations. I just keep waiting for a bit then I can tell the seller well you best sharpen that pencil up a bit. |

|

|

|

|

[#19]

Originally Posted By exponentialpi: Price cuts are increasing. Demand seems to be stagnant. https://www.ar15.com/media/mediaFiles/200878/IMG_3798_jpeg-3165856.JPG |

|

|

|

|

[#20]

In my house-hunting recently, I'm seeing homes go "contingent" or "pending" then a couple of weeks later go back on the market. One place has done it 4 times since the beginning of the year. If it were one or two times, I'd say buyers weren't able to get financing. But four times? That's just odd and tells me there's something weird going on with that property. But, I'm seeing this happening more and more. Am also seeing the actual selling prices start to be significantly less than the asking prices (well, if you consider 5-7% less "significant").

There's one house that has been for sale off and on since summer of 2022. It appears they are asking way too much but they keep pulling the listing then putting back on at the same (too high) price a month or so later. They must not be too eager to sell the place. |

|

|

|

|

[#21]

State Farm singing a little NSYNC. I got a great idea for a new commercial.

*NSYNC - Bye Bye Bye (Official Video) https://www.ar15.com/forums/t_1_5/2714653_State-Farm-Discontinuing-72-000-Home-Policies-In-California-In-Latest-Blow-To-State-Insurance-Market.html |

|

|

|

|

[#22]

Originally Posted By planemaker: In my house-hunting recently, I'm seeing homes go "contingent" or "pending" then a couple of weeks later go back on the market. One place has done it 4 times since the beginning of the year. If it were one or two times, I'd say buyers weren't able to get financing. But four times? That's just odd and tells me there's something weird going on with that property. But, I'm seeing this happening more and more. Am also seeing the actual selling prices start to be significantly less than the asking prices (well, if you consider 5-7% less "significant"). There's one house that has been for sale off and on since summer of 2022. It appears they are asking way too much but they keep pulling the listing then putting back on at the same (too high) price a month or so later. They must not be too eager to sell the place. They have been doing that, and taking a stagnant listing and relisting as a new listing at the same price. I believe the thing you are referencing is called priming the pump, or at least how I was taught it back in the day. Basically in sales, if you are having a slow time you take an item, or two and put a SOLD banner on it. It makes others think they are the not the only one buying it, and bumps up sales. |

|

|

|

|

[#23]

Originally Posted By Chromekilla: And electrical was about $20, wsg maybe 75 max. Car insurance probably $300 per year. Home insurance maybe $1000. Food maybe $500 a month for a family of 4. And maybe a down payment of 20% on a 95,000 house. Originally Posted By Chromekilla: Originally Posted By hicap: I know you've heard it before, mortgages waere 12.75% in 1985, payment was around 950, I made $27K and wife made $19K. And electrical was about $20, wsg maybe 75 max. Car insurance probably $300 per year. Home insurance maybe $1000. Food maybe $500 a month for a family of 4. And maybe a down payment of 20% on a 95,000 house. Internet and iphones took a smaller bite out of the monthly budget too. |

|

|

|

|

[#24]

Originally Posted By FuriousYachtsman: Internet and iphones took a smaller bite out of the monthly budget too. If you are smart you buy older, NIB cell phones, and use your unlimited data plan as a hot spot. Thus saving $200 a month. |

|

|

|

|

[#25]

Originally Posted By planemaker: In my house-hunting recently, I'm seeing homes go "contingent" or "pending" then a couple of weeks later go back on the market. One place has done it 4 times since the beginning of the year. If it were one or two times, I'd say buyers weren't able to get financing. But four times? That's just odd and tells me there's something weird going on with that property. But, I'm seeing this happening more and more. Am also seeing the actual selling prices start to be significantly less than the asking prices (well, if you consider 5-7% less "significant"). There's one house that has been for sale off and on since summer of 2022. It appears they are asking way too much but they keep pulling the listing then putting back on at the same (too high) price a month or so later. They must not be too eager to sell the place. Not being able to get the financing is probably true, although they should have that ironed out before making a bid. Expect more of that with buyers "going it alone" now. My guess is not meeting appraisal and buyer not having enough cash to meet the difference. Could be something really bad constantly showing up in the inspection and the seller is too cheap/stupid to get it fixed. |

|

|

|

MI, USA

|

[Last Edit: DaddyShark]

[#26]

In the process of buying a home, just waiting for closing now. It's still really bad. I thought it was getting better because you noticed quite a few homes sitting on the market for many months. But after going out and seeing those homes, it was obvious to see why they weren't selling. Either something very wrong with the home that you couldn't tell from the listing or the house was in a terrible location. Like being on a very busy road with the house very close to the road. And inside and out, the sound of traffic driving by was insane. Some of the others ones that aren't selling is because the seller wants wayy too much money (even for this market). And it's obvious that's the case because you can see much nicer homes selling for the same price or less in the same area. Also, very expensive homes are taking a long time to sell. But if it's a home like I was looking for, nothing fancy, but a decent livable house that a middle class family could afford, those types are homes are gone within days or even hours after being listed...

|

|

|

|

[#27]

Originally Posted By exponentialpi: Price cuts are increasing. Demand seems to be stagnant. https://www.ar15.com/media/mediaFiles/200878/IMG_3798_jpeg-3165856.JPG I've seen a few articles and videos on deflation, the sky is falling now. Prices need to come down or the economy is going to stall out, if it hasn't already. From what I'm seeing it's not a supply/demand issue it's companies and people have gotten used to fat margins. Problem is families margins shrunk, something has to give question is which breaks 1st? |

|

|

|

|

[#28]

Originally Posted By 2tired2run: I've seen a few articles and videos on deflation, the sky is falling now. Prices need to come down or the economy is going to stall out, if it hasn't already. From what I'm seeing it's not a supply/demand issue it's companies and people have gotten used to fat margins. Problem is families margins shrunk, something has to give question is which breaks 1st? Originally Posted By 2tired2run: Originally Posted By exponentialpi: Price cuts are increasing. Demand seems to be stagnant. https://www.ar15.com/media/mediaFiles/200878/IMG_3798_jpeg-3165856.JPG I've seen a few articles and videos on deflation, the sky is falling now. Prices need to come down or the economy is going to stall out, if it hasn't already. From what I'm seeing it's not a supply/demand issue it's companies and people have gotten used to fat margins. Problem is families margins shrunk, something has to give question is which breaks 1st? |

|

|

|

|

[#29]

It appears that mortgage rates dropped this week and the 30 year sits at 6.91% average.

FWIW a neighbors place sold, closed this week. Took 30 days to go contingent on a 10k over asking price offer. Slowest pace to sold in the last 3 years. |

|

|

|

|

[#30]

Yikes Phoenix.

|

|

|

|

|

[Last Edit: The_Master_Shake]

[#31]

Originally Posted By wookie1562: That's one interpretation.... A more succinct one is that sales are down 4% since last year, which was already dead. Median sale price for Q1 23 vs Q1 24 is down ~3%. Inventory continues to climb despite being in peak season. Time on the market continues to climb. No rate relief is coming. The 5 D's never sleep (death, divorce, downsizing, diapers, diamonds) Unemployment continues to accelerate. California and several other states appear to already be in recession. There's this too: https://pbs.twimg.com/media/GJNOWU2XAAEx53m?format=png&name=small I like the 5 D's phrase I'm going to use that |

|

|

|

USA

|

[#32]

lol

Multiple offers are already here Homebuyers were more active last month, with some regions even seeing the rekindling of multiple offers despite prices of homes ticking higher. According to the NAR, all four regions registered year-over-year gains in prices. In the West, existing home sales vaulted nearly 17% from a month ago, and the median price was $593,000, up 9% annually. Sales in the South jumped by nearly 10% from January, and the median price increased 4% from last year to $354,200. In the Midwest, home sales surged more than 8% from a month earlier, and the median price was $277,600. As for the Northeast, sales of existing homes were unchanged from January but were down almost 8% from a year ago. The average price of homes sold was $420,600, up 11.5% from a year ago, the largest year-over-year gain out of all regions. “The Northeast is somewhat unique in terms of why sales did not increase … simply due to the fact that there's lack of inventory and presence of large multiple offers happening because of lack of inventory,” Yun said. “The Northeast is actually seeing the strongest price increases. So [demand] can hamper due to the lack of inventory situation.” https://finance.yahoo.com/news/home-sales-surge-as-buyers-make-peace-with-elevated-mortgage-rates-182958706.html |

|

|

|

[#33]

|

|

|

|

|

[#34]

Originally Posted By spidey07: That’s why you don’t escrow. Let the fools get squeezed. They signed it. Originally Posted By spidey07: Originally Posted By exponentialpi: Originally Posted By Chromekilla: Originally Posted By exponentialpi: Those 20% rate increases are starting to sting.

Bold move cotton lets see how that plays out Getting more attention. Insurance coverage is going to squeeze lots of people.

That’s why you don’t escrow. Let the fools get squeezed. They signed it. Whether you escrow or not is completely irrelevant to this conversation.

|

|

|

|

|

[#35]

Originally Posted By wookie1562:

https://pbs.twimg.com/media/GJhtj2GWQAAO3XX?format=jpg&name=smallhttps://pbs.twimg.com/media/GJhtjz7XgAAgynT?format=jpg&name=small https://pbs.twimg.com/media/GJhtk15WwAEapzG?format=png&name=smallhttps://pbs.twimg.com/media/GJhtk2bXMAA5dHY?format=png&name=small https://pbs.twimg.com/media/GJhvmYgW0AAS8_l?format=jpg&name=smallhttps://pbs.twimg.com/media/GJhvmZUXEAAsvUW?format=png&name=small This time is different. |

|

|

|

|

[#36]

Originally Posted By exponentialpi: This time is different. I know people that sold three years ago that are still renting waiting for the crash. |

|

|

|

|

[#37]

Originally Posted By OregonShooter: It appears that mortgage rates dropped this week and the 30 year sits at 6.91% average. FWIW a neighbors place sold, closed this week. Took 30 days to go contingent on a 10k over asking price offer. Slowest pace to sold in the last 3 years. Going to suck being the last one in. |

|

|

|

|

[#38]

Originally Posted By OregonShooter: I know people that sold three years ago that are still renting waiting for the crash. Aka wise people  |

|

|

|

|

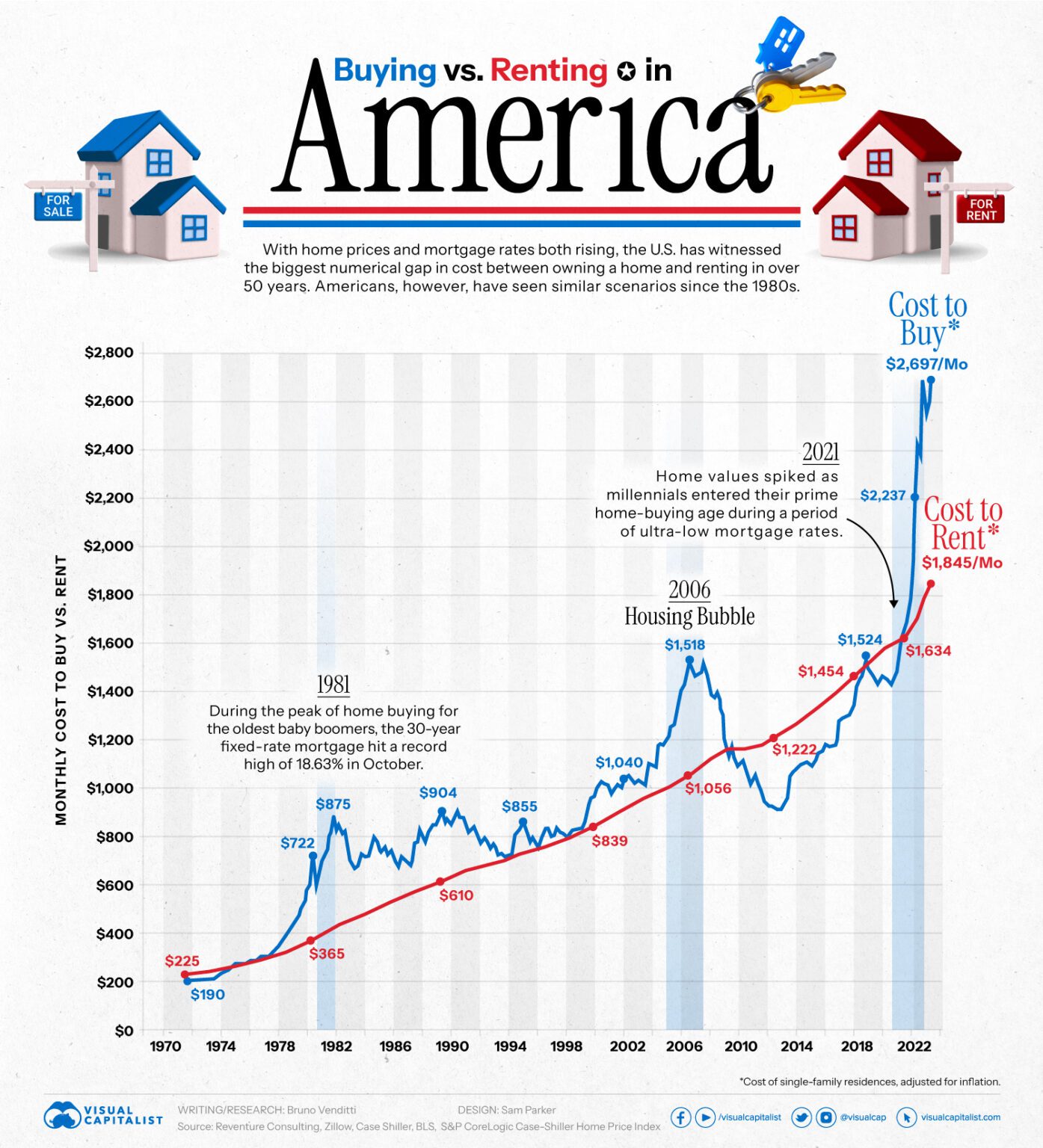

[#39]

Originally Posted By wookie1562: Aka wise people https://www.visualcapitalist.com/wp-content/uploads/2023/09/Buying-vs-Renting-in-America_Sept_1-1395x1536.jpg So the difference is $400/month or under $5000 a year I'd rather own with a fixed payment (except taxes and insurance) versus rental increases Plus mu property taxes and interest are tax deductible, rent is not for your residence |

|

|

|

USA

|

[#40]

Man the doomers just can't catch a break - this morning's CSI report:

Prices nationally climbed 6% in January from a year earlier, according to data from S&P CoreLogic Case-Shiller. That’s bigger than the 5.6% annual gain in December. The housing market has been tough to navigate since borrowing costs started soaring in 2022, squeezing the purchasing power of many shoppers. While inventory has started to rise recently, homes listed for sale remain low by historical standards and the tight supply has helped keep prices high. “Homeowners most likely saw healthy gains in the last year, no matter what city you were in, or if it was in an expensive or inexpensive neighborhood,” Brian Luke, head of commodities, real and digital assets at S&P Dow Jones Indices, said in a statement. “No matter which way you slice it, the index performance closely resembled the broad market.” A measure of values in 20 cities was up 6.6% in January from a year earlier, compared with a 6.2% gain in the previous month. San Diego led those cities with an 11.2% increase, while prices in Los Angeles were up 8.6%. https://finance.yahoo.com/news/us-home-price-growth-picks-130000757.html |

|

|

|

[Last Edit: STJ]

[#41]

Originally Posted By colt_thompson: So the difference is $400/month or under $5000 a year I'd rather own with a fixed payment (except taxes and insurance) versus rental increases Plus mu property taxes and interest are tax deductible, rent is not for your residence Originally Posted By colt_thompson: Originally Posted By wookie1562: Aka wise people https://www.visualcapitalist.com/wp-content/uploads/2023/09/Buying-vs-Renting-in-America_Sept_1-1395x1536.jpg So the difference is $400/month or under $5000 a year I'd rather own with a fixed payment (except taxes and insurance) versus rental increases Plus mu property taxes and interest are tax deductible, rent is not for your residence most take the standard deduction. |

|

|

|

|

[#42]

Originally Posted By LesBaer45: I have a former co-worker that's looking to move to FL as well. Trying to remember where exactly thinking it was gulf coast pan handle area I think. I meant to ask him was he concerned with insurance availability / rates just to get a response. So I'll ask you? Originally Posted By LesBaer45: Originally Posted By BillofRights: I’m finally seeing some downward movement in my area of interest. FL, N of Orlando Still not down to what I want, but it’s getting there. As far as a “fair price” I’m waiting for 2020 prices, adjusted for inflation. I have a former co-worker that's looking to move to FL as well. Trying to remember where exactly thinking it was gulf coast pan handle area I think. I meant to ask him was he concerned with insurance availability / rates just to get a response. So I'll ask you? Yes. FL has special requirements. I want Cement Block construction. Most two story houses are stick built on the upper half. So, single story is most likely what I’ll get. In addition you need all the FL wind mitigation, so you really need to buy a fairly new house, or you’ll be dealing with Insurance bs. Additionally, you have to be very careful about flood zones. Floods have happened recently, in unexpected areas. |

|

|

|

|

[#43]

Originally Posted By wookie1562: Inventory in FL is currently 98% of the Feb 2020 figure and trending up.

https://pbs.twimg.com/media/GJOHKUWW8AApmU0?format=jpg&name=medium Originally Posted By wookie1562: Originally Posted By anothermisanthrope: Oh FFS if you're going to try and correct me you could at least read the first line quoted in my post. Now do supply and demand. Inventory in FL is currently 98% of the Feb 2020 figure and trending up.

https://pbs.twimg.com/media/GJOHKUWW8AApmU0?format=jpg&name=medium That’s very good news. Thanks for posting it! A-Misinintrope, what’s the point in posting negative information while calling it positive info? What’s your angle? |

|

|

|

|

[#44]

Listed fiancés house on a Friday a couple of weeks ago. Received a cash offer above asking with no inspection that day. There were other bids but as stated, high bids can outrun appraisals.

|

|

|

|

|

[Last Edit: BillofRights]

[#45]

Originally Posted By OregonShooter: I know people that sold three years ago that are still renting waiting for the crash. Originally Posted By OregonShooter: Originally Posted By exponentialpi: This time is different. I know people that sold three years ago that are still renting waiting for the crash. Let’s say they netted $350k. That money is earning them $1458 a month just sitting at Fidelity at 5%. If they put the money into a simple pipeline LP, such as ET, they would be getting $28,000/year or $2333 per month. -And, their total investment would have also Doubled in that time. If they invested some in any S&P 500 ETF, they would have gained 20%, or $70,000 -just saying; things are not as simple as you think, when managing large amounts of capital. |

|

|

|

USA

|

[Last Edit: anothermisanthrope]

[#46]

Originally Posted By BillofRights: Let’s say they netted $350k. That money is earning them $1458 a month just sitting at Fidelity at 5%. If they put the money into a simple pipeline LP, such as ET, they would be getting $28,000/year or $2333 per month. -And, their total investment would have also Doubled in that time. If they invested some in any S&P 500 ETF, they would have gained 20%, or $70,000 -just saying; things are not as simple as you think, when managing large amounts of capital. Originally Posted By BillofRights: Originally Posted By OregonShooter: Originally Posted By exponentialpi: This time is different. I know people that sold three years ago that are still renting waiting for the crash. Let’s say they netted $350k. That money is earning them $1458 a month just sitting at Fidelity at 5%. If they put the money into a simple pipeline LP, such as ET, they would be getting $28,000/year or $2333 per month. -And, their total investment would have also Doubled in that time. If they invested some in any S&P 500 ETF, they would have gained 20%, or $70,000 -just saying; things are not as simple as you think, when managing large amounts of capital. What if home appreciates, while building more equity? |

|

|

|

[#47]

Originally Posted By BillofRights: Let's say they netted $350k. That money is earning them $1458 a month just sitting at Fidelity at 5%. If they put the money into a simple pipeline LP, such as ET, they would be getting $28,000/year or $2333 per month. -And, their total investment would have also Doubled in that time. If they invested some in any S&P 500 ETF, they would have gained 20%, or $70,000 -just saying; things are not as simple as you think, when managing large amounts of capital. Originally Posted By BillofRights: Originally Posted By OregonShooter: Originally Posted By exponentialpi: This time is different. I know people that sold three years ago that are still renting waiting for the crash. Let's say they netted $350k. That money is earning them $1458 a month just sitting at Fidelity at 5%. If they put the money into a simple pipeline LP, such as ET, they would be getting $28,000/year or $2333 per month. -And, their total investment would have also Doubled in that time. If they invested some in any S&P 500 ETF, they would have gained 20%, or $70,000 -just saying; things are not as simple as you think, when managing large amounts of capital. plus a little BTC. I'm not losing $ |

|

|

|

|

[#48]

Originally Posted By BillofRights: Let’s say they netted $350k. That money is earning them $1458 a month just sitting at Fidelity at 5%. If they put the money into a simple pipeline LP, such as ET, they would be getting $28,000/year or $2333 per month. -And, their total investment would have also Doubled in that time. If they invested some in any S&P 500 ETF, they would have gained 20%, or $70,000 -just saying; things are not as simple as you think, when managing large amounts of capital. I agree. I have two couples that sold their paid for homes (one was $500k and one was $540k) to downsize that rent from me. I can build a duplex for $300,000 plus land They pay $2000/month each Taxes, insurance, mowing and plowing is about $14,000 a year So my $350,000 investment nets me $34,000/year plus any appreciation They make their entire rent payment just in interest plus they save on taxes, insurance and upkeep Win/win |

|

|

|

|

[#49]

Originally Posted By The_Master_Shake: I like the 5 D's phrase I'm going to use that Originally Posted By The_Master_Shake: Originally Posted By wookie1562: That's one interpretation.... A more succinct one is that sales are down 4% since last year, which was already dead. Median sale price for Q1 23 vs Q1 24 is down ~3%. Inventory continues to climb despite being in peak season. Time on the market continues to climb. No rate relief is coming. The 5 D's never sleep (death, divorce, downsizing, diapers, diamonds) Unemployment continues to accelerate. California and several other states appear to already be in recession. There's this too: https://pbs.twimg.com/media/GJNOWU2XAAEx53m?format=png&name=small I like the 5 D's phrase I'm going to use that Sitting in a Cali beach town. Sure doesn't look like recession around here by the number of wide bodies flying and people I see around... |

|

|

|

PRK

|

[#50]

Originally Posted By anothermisanthrope: Man the doomers just can't catch a break - this morning's CSI report: https://finance.yahoo.com/news/us-home-price-growth-picks-130000757.html Or maybe the dollar has lost that much more value and doomers were right all along, in a way The way they’re printing it seems more likely |

|

|

Win a FREE Membership!

Win a FREE Membership!

Sign up for the ARFCOM weekly newsletter and be entered to win a free ARFCOM membership. One new winner* is announced every week!

You will receive an email every Friday morning featuring the latest chatter from the hottest topics, breaking news surrounding legislation, as well as exclusive deals only available to ARFCOM email subscribers.

AR15.COM is the world's largest firearm community and is a gathering place for firearm enthusiasts of all types.

From hunters and military members, to competition shooters and general firearm enthusiasts, we welcome anyone who values and respects the way of the firearm.

Subscribe to our monthly Newsletter to receive firearm news, product discounts from your favorite Industry Partners, and more.

Copyright © 1996-2024 AR15.COM LLC. All Rights Reserved.

Any use of this content without express written consent is prohibited.

AR15.Com reserves the right to overwrite or replace any affiliate, commercial, or monetizable links, posted by users, with our own.