|

[#1]

Rats, pesky new pages.

|

|

|

|

[#2]

Target Acquired.

Send it. BOOM! http://www.ar15.com/forums/t_1_5/1242625_.html&page=1 |

|

|

|

[#3]

Quoted:

Target Acquired. Send it. BOOM! http://www.ar15.com/forums/t_1_5/1242625_.html&page=1 Thanks for that. I pretty much thought the same thing, but you helped put some names to the movement. |

|

|

|

[#4]

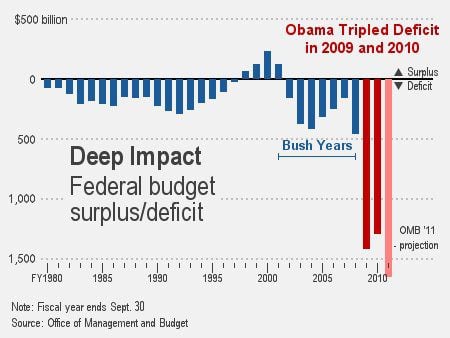

Remember the Bush bashing about his Deficit Spending? The MSM has become irrelevant, but has anyone questioned the House Leadership as to why they are allowing this spending to continue? Ticking time-bomb |

|

|

|

[#5]

Quoted:

http://www.thegatewaypundit.com/wp-content/uploads/2011/02/obama-deficit-2011.jpg Remember the Bush bashing about his Deficit Spending? The MSM has become irrelevant, but has anyone questioned the House Leadership as to why they are allowing this spending to continue? Ticking time-bomb Speaker John Boehner pushed his debt-ceiling bill through the House Friday night with the support of 218 Republicans. Here are the 22 no votes: Justin Amash (Mich.) Michele Bachmann (Minn.) Chip Cravaack (Minn.) Jason Chaffetz (Utah) Scott Desjarlais (Tenn.) Tom Graves (Ga.) Tim Huelskamp (Kans.) Steve King (Iowa) Tim Johnson (Ill.) Tom McClintock (Calif.) Mick Mulvaney (S.C.) Ron Paul (Texas) Connie Mack (Fla.) Jim Jordan (Ohio) Tim Scott (S.C.) Paul Broun (Ga.) Tom Latham (Iowa) Jeff Duncan (S.C.) Trey Gowdy (S.C.) Steve Southerland (Fla.) Joe Walsh (Ill.) Joe Wilson (S.C.) |

|

|

|

[#6]

Quoted:

http://www.thegatewaypundit.com/wp-content/uploads/2011/02/obama-deficit-2011.jpg Remember the Bush bashing about his Deficit Spending? The MSM has become irrelevant, but has anyone questioned the House Leadership as to why they are allowing this spending to continue? Ticking time-bomb As bad as that chart looks it is actually much worse. If the fed.gov had to use legally required accounting methods like EVERYONE else then they have not had a balanced budget in many generations. |

|

|

|

[#7]

Speak of the devil ... I had just posted this over in the debate thread ...

Quoted:

Quoted:

<snip> Newt for the win last night particularly on National Defence. Cain did fine in defence of his 9-9-9 plan too. While the 9-9-9 Plan sounds great in sound bites .... They ain't gonna stop the selfish spending, not one iota, so the 9-9-9 comes off sounding like a kid's plan to arrange his underwear drawer to get his ma off his back. But hey, I may have it wrong.

|

|

|

|

[#8]

Math vs. Myth

There is no austerity, only more uncontrolled spending. Michael Tanner It is a medical truism that if you get the diagnosis wrong, the treatment will be wrong. The same holds true with Washington budgeting. Unfortunately, as we prepare for yet more debates over budgeting, spending, and stimulus, we can expect to once again enter a fact-free debate. Among the most common myths: 1. Republicans have slashed government spending. While there are political reasons for both Democrats and Republicans to pretend that we’ve entered a new age of austerity, it’s not even close to true. According to figures released last week by the Treasury Department, federal spending this year is up by roughly 5 percent over the same period last year. That’s a $120 billion increase in just the first nine months of this year. That’s right: Despite a near shutdown of the government and “holding the debt ceiling hostage,” government spending is still increasing. And not surprisingly, we are borrowing more money in order to fund it. The deficit is already $23.5 billion higher this year — with three months still to go. As a result, our national debt continues to grow. This month it will close in on $15 trillion. Throw in the unfunded liabilities of Social Security and Medicare, and our real indebtedness tops $120 trillion and rising. If Keynesian-style stimulus worked, we should be swimming in jobs. 2. States are firing teachers and firefighters because they are broke. Washington has to help. That’s the logic behind the president’s plan for $35 billion in additional federal aid to the states, a bill that the Senate is expected to vote on this week. In reality, however, state government spending has also been rising, up more than 10 percent in the past two years. And while some of that represents a pass-through of federal aid from earlier stimulus bills, state general-fund spending rose 5.2 percent this year. If state governments are laying off teachers and firefighters, it’s because they are failing to manage their priorities, not because they don’t have any money. 3. We have a revenue problem. Yes, tax revenues are low today by historic standards, in part because of the recession and in part because of the Bush tax cuts. But this is a temporary phenomenon. According to the Congressional Budget Office, even if the entirety of the Bush tax cuts were made permanent and the Alternative Minimum Tax (AMT) repealed, tax revenue would rise to more than 20 percent of GDP by 2020. That’s roughly two percentage points of GDP above the historic average. If taxes will bring in more revenue than usual, how is it that we are still projecting huge future deficits? Simple, spending is expected to rise even faster. In 2020, federal spending is estimated to be roughly 25 percent of GDP, roughly four percentage points higher than historic averages, and seven points higher than it was under President Clinton. So, which side of the ledger has a problem? 4. We can solve our problems by taxing the rich and closing corporate loopholes. Set aside the question of whether higher taxes on the rich would stifle economic growth and job creation. There is simply no way to raise enough money to cover our deficits by taxing the rich. As the president would say, “It’s math.” This year, we will run a deficit of roughly $1.3 trillion. Eliminating the tax break for corporate jets, a prime Democratic talking point, would raise roughly $300 million this year. Yes, that’s million with an “m.” Ending tax breaks for oil and gas companies, another frequent Democratic target, would bring in somewhat more, nearly $4 billion per year. And, the big enchilada, the Democrats’ proposed 5.6 percent surtax on “millionaires and billionaires,” would raise an average of $45.3 billion in additional revenue per year. Therefore, if the Democrats were able to get every penny that they want, they would raise all of $49.6 billion per year, leaving us with a budget deficit this year of only $1.25 trillion. 5. We can balance the budget by cutting “fraud, waste, and abuse.” This is the Republican flip side of the Democrats’ reliance on higher taxes, a way to avoid making tough choices about cutting defense and reforming entitlements. Total domestic discretionary spending — everything from the Department of Education to the Department of Commerce, from the FBI to the FDA — amounted to roughly $650 billion this year. If we simply abolished all of those programs, the muscle and bone as well as the fat, we would still have a $650 billion budget deficit. That is not to say that we shouldn’t cut everywhere we can, but to spend too much time searching for “fraud, waste, and abuse” is to pluck out a splinter while the patient is bleeding to death. With any addiction, the first step to recovery is to admit that you have a problem. Washington remains addicted to spending. It is time for Congress to get honest about that and stop hiding behind these budget myths. Maybe then, we can begin the path to economic recovery. — Michael Tanner is a senior fellow at the Cato Institute and author of Leviathan on the Right: How Big-Government Conservatism Brought Down the Republican Revolution. |

|

|

|

[#9]

different person, obviously. must have coffee before posting. carry on...

|

|

|

|

[#10]

Quoted: Quoted: http://www.thegatewaypundit.com/wp-content/uploads/2011/02/obama-deficit-2011.jpg Remember the Bush bashing about his Deficit Spending? The MSM has become irrelevant, but has anyone questioned the House Leadership as to why they are allowing this spending to continue? Ticking time-bomb As bad as that chart looks it is actually much worse. If the fed.gov had to use legally required accounting methods like EVERYONE else then they have not had a balanced budget in many generations.  |

|

|

|

[#11]

STRATFOR is doing a special this weekend on what to do wrt Greece. Here's their flowchart promo:

Anyone a subscriber who can fill us in on the details? |

|

|

|

[#12]

Watching GB from last night, he talked about a national "Bank Transfer Day" on Nov 5th. Apparently it is a day to take your money out of the bank and put it into a credit union.

The interesting thing is he showed a screen shot of their Facebook page. It has been scrubbed from Facebook - I just went to find it and it's not there. Has anyone else heard about this protest? |

|

|

|

[#13]

Quoted:

Quoted:Collapse is relative. If they weren't handing out ObamaBucks to every person with a sob story there would be soup lines and riots in the streets. Would you consider that a collapse?

According to Sherrick, as long as the rioters are willing to trade cans of soup for molitov coctails then commerce is still happening, so....... no.

Ain't that the truth.

Decrease in standard of living: not "huge" yet, but certainly the biggest drop since records were started... in 1960. Clearly abnormal, but only time will tell what will happen over the next 36 months. The 4 years of bad news, busted markets, and floundering economies at the expense of tens of trillions of dollars in "stimulus spending" CLEARLY suggests a Recovery. Bottom line: The average individual now has $1,315 less in disposable income than he or she did three years ago at the onset of the Great Recession – even though the recession ended, technically speaking, in mid-2009. That means less money to spend at the spa or the movies, less for vacations, new carpeting for the house, or dinner at a restaurant. -snip- What has led to the most dramatic drop in the US standard of living since at least 1960? One factor is stagnant incomes: Real median income is down 9.8 percent since the start of the recession through this June, according to Sentier Research in Annapolis, Md., citing census bureau data. Another is falling net worth – think about the value of your home and, if you have one, your retirement portfolio. A third is rising consumer prices, with inflation eroding people's buying power by 3.25 percent since mid-2008. http://www.csmonitor.com/Business/2011/1019/A-long-steep-drop-for-Americans-standard-of-living |

|

|

|

[#14]

Beginnings of STRATFOR's coverage:

The European Banking Crisis, Part 1: Assessing the Damage October 21, 2011 Europe faces a banking crisis it has not wanted to admit even exists. The formal authority on financial stability, International Monetary Fund (IMF) chief Christine Lagarde, made her institution’s opinion on European banking known back in August when she prompted the European Union to engage in an immediate 200 billion-euro bank recapitalization effort. The response was broad-based derision from Europeans at the local, national and EU bureaucratic levels. The vehemence directed at Lagarde was particularly notable as Lagarde is certainly in a position to know what she was talking about: Until July 5, her title was not IMF chief, but French finance minister. She has seen the books, and the books are bad. Due to European inaction, the IMF on Oct. 18 raised its estimate for recapitalization needs from 200 billion euros to 300 billion euros ($274 billion to $410 billion). Link Full disclosure - I have not read any of this yet.

|

|

|

|

[#15]

No comment needed.

The GAO Audit of the Fed Doesn't Call It 'Corruption'.... The Government Accountability Office (GAO) finished its second audit of the Federal Reserve System and came out with a 127-page report that outlines, among other issues, the huge and complex conflicts of interests that arose when the Fed decided who got what during the multi-trillion dollar bailout mania between 2007 and 2009 (for a 1-page timeline of bailout mania, click here; for Senator Bernie Sanders' 4-page Report on the GAO Audit, click here). Speaking of conflicts of interest: the GAO audit was authorized by the Dodd-Frank financial reform act—whose co-sponsor Barney Frank (D) is scheduled to attend a Wall Street fundraiser in New York tonight, according to Politico. Last June, Frank attended a Wall Street fundraiser organized by the Securities Industry and Financial Markets Association, which lobbies against financial reforms. Money is important, after all. Even for President Obama. He raised more money from Wall Street than did all GOP presidential candidates combined, according to a Washington Post analysis. So where were we? Ah yes, conflicts of interest, favoritism, and lots of money for some—but not all: The GAO identified 18 former and current members of the Federal Reserve's board affiliated with banks and companies that received emergency loans from the Federal Reserve during the financial crisis.... For the heck of it, let's dive into a specific example. In January 2008 when the financial crisis was already in full swing, Goldman Sachs board member and shareholder Stephen Friedman joined the Federal Reserve Bank of New York as a Class C director. At the time, Goldman Sachs was an investment bank, and thus not regulated by the Federal Reserve. But then Lehman Brothers began to totter. Its CEO, Richard Fuld, a Class B director at the New York Fed, met with Timothy Geithner, president of the New York Fed, and with Friedman, who was then chairman of the New York Fed (and still sat on the board of Goldman Sachs). Fuld needed help. However, due to potential "reputational risks," Geithner and Friedman turned down his request. Further, Federal Reserve Board practice sees to it that directors resign when their financial institutions get in trouble. So, instead of getting bailed out, Fuld had to resign. And on September 15, Lehman filed for bankruptcy. September 20, Goldman Sachs, now tottering too, submitted an application to become a bank holding company. With Friedman being chairman of the New York Fed, the application was approved overnight. That did a number of things, among them: It gave the firm access to the Fed's unlimited resources; and Friedman became ineligible to remain a Class C director and should have resigned, but didn't. Then on September 23, there was a public demonstration of just how intertwined the financial elite around the Fed is. Friedman's long-time friend and client Warren Buffet announced Berkshire Hathaway's investment in Goldman Sachs. During an interview with CNBC, Buffet said that he wouldn't have made the move, had he not been certain that Goldman Sachs would get bailed out. And he got a special deal: $5 billion in preferred stock with a 10% annual dividend plus warrants to buy $5 billion in common stock at a strike price of $115. When the announcement was made after hours, GS jumped to $134.75. The warrants were already in the money (today, GS closed at $100.86). In October that year, the New York Fed asked for a waiver that would allow Friedman to remain a Class C director while being a board member and stockholder of Goldman Sachs, the very firm he was now regulating and bailing out. On January 21, 2009, the waiver was approved though not publicly disclosed. But throughout that time, Friedman, as chairman of the New York Fed, purchased more Goldman Sachs stock, knowing what bailout instruments were being planned and implemented, and which firm got how much and under what conditions. Among the 18 people identified in the GAO report was Jeffrey Immelt, the CEO of General Electric, and a director on the board of the New York Fed. He was involved in establishing the Commercial Paper Funding Facility that later handed GE $16 billion in bailout funds (he is now Chairman of the Council on Jobs and Competitiveness in the Obama administration). Another was Jamie Dimon, the CEO of JP Morgan Chase, and a director at the New York Fed. And we can assume that there were many more that the audit didn't identify. These audits are good. And they're necessary. So we're grateful that Senator Bernie Sanders sponsored the amendment to Frank-Dodd that authorized them. But they're only a feeble first step. Courageous congressional action to clean up the financial cesspool that is bogging down the economy should be next. But Congress is hooked on Wall Street fund raisers. And it is hooked on the Fed's printing press to monetize the gigantic budget deficits. So there isn't much hope for serious reform. |

|

|

|

[#16]

NC Jobless rate continues to rise.

N.C. jobless rate continues to rise By: RICHARD CRAVER | Winston-Salem Journal Published: October 21, 2011 Updated: October 21, 2011 - 4:01 PM Another round of government job losses during September sent the state's jobless rate to its highest level in 17 months, the N.C. Employment Security Commission reported Friday. The rate increased 0.1 percentage point to 10.5 percent. The state experienced a loss of 22,200 jobs during September compared with August, of which 13,700 were government jobs. Over the past 12 months, there has been a reduction of 18,700 government jobs. The one bright spot in the private sector was a net gain of 2,800 construction jobs. More here. |

|

|

|

[#17]

Quoted:

No comment needed. The GAO Audit of the Fed Doesn't Call It 'Corruption'.... The Government Accountability Office (GAO) finished its second audit of the Federal Reserve System and came out with a 127-page report that outlines, among other issues, the huge and complex conflicts of interests that arose when the Fed decided who got what during the multi-trillion dollar bailout mania between 2007 and 2009 (for a 1-page timeline of bailout mania, click here; for Senator Bernie Sanders' 4-page Report on the GAO Audit, click here). Speaking of conflicts of interest: the GAO audit was authorized by the Dodd-Frank financial reform act—whose co-sponsor Barney Frank (D) is scheduled to attend a Wall Street fundraiser in New York tonight, according to Politico. Last June, Frank attended a Wall Street fundraiser organized by the Securities Industry and Financial Markets Association, which lobbies against financial reforms. Money is important, after all. Even for President Obama. He raised more money from Wall Street than did all GOP presidential candidates combined, according to a Washington Post analysis. So where were we? Ah yes, conflicts of interest, favoritism, and lots of money for some—but not all: The GAO identified 18 former and current members of the Federal Reserve's board affiliated with banks and companies that received emergency loans from the Federal Reserve during the financial crisis.... For the heck of it, let's dive into a specific example. In January 2008 when the financial crisis was already in full swing, Goldman Sachs board member and shareholder Stephen Friedman joined the Federal Reserve Bank of New York as a Class C director. At the time, Goldman Sachs was an investment bank, and thus not regulated by the Federal Reserve. But then Lehman Brothers began to totter. Its CEO, Richard Fuld, a Class B director at the New York Fed, met with Timothy Geithner, president of the New York Fed, and with Friedman, who was then chairman of the New York Fed (and still sat on the board of Goldman Sachs). Fuld needed help. However, due to potential "reputational risks," Geithner and Friedman turned down his request. Further, Federal Reserve Board practice sees to it that directors resign when their financial institutions get in trouble. So, instead of getting bailed out, Fuld had to resign. And on September 15, Lehman filed for bankruptcy. September 20, Goldman Sachs, now tottering too, submitted an application to become a bank holding company. With Friedman being chairman of the New York Fed, the application was approved overnight. That did a number of things, among them: It gave the firm access to the Fed's unlimited resources; and Friedman became ineligible to remain a Class C director and should have resigned, but didn't. Then on September 23, there was a public demonstration of just how intertwined the financial elite around the Fed is. Friedman's long-time friend and client Warren Buffet announced Berkshire Hathaway's investment in Goldman Sachs. During an interview with CNBC, Buffet said that he wouldn't have made the move, had he not been certain that Goldman Sachs would get bailed out. And he got a special deal: $5 billion in preferred stock with a 10% annual dividend plus warrants to buy $5 billion in common stock at a strike price of $115. When the announcement was made after hours, GS jumped to $134.75. The warrants were already in the money (today, GS closed at $100.86). In October that year, the New York Fed asked for a waiver that would allow Friedman to remain a Class C director while being a board member and stockholder of Goldman Sachs, the very firm he was now regulating and bailing out. On January 21, 2009, the waiver was approved though not publicly disclosed. But throughout that time, Friedman, as chairman of the New York Fed, purchased more Goldman Sachs stock, knowing what bailout instruments were being planned and implemented, and which firm got how much and under what conditions. Among the 18 people identified in the GAO report was Jeffrey Immelt, the CEO of General Electric, and a director on the board of the New York Fed. He was involved in establishing the Commercial Paper Funding Facility that later handed GE $16 billion in bailout funds (he is now Chairman of the Council on Jobs and Competitiveness in the Obama administration). Another was Jamie Dimon, the CEO of JP Morgan Chase, and a director at the New York Fed. And we can assume that there were many more that the audit didn't identify. These audits are good. And they're necessary. So we're grateful that Senator Bernie Sanders sponsored the amendment to Frank-Dodd that authorized them. But they're only a feeble first step. Courageous congressional action to clean up the financial cesspool that is bogging down the economy should be next. But Congress is hooked on Wall Street fund raisers. And it is hooked on the Fed's printing press to monetize the gigantic budget deficits. So there isn't much hope for serious reform. I hope your link isn't linked to Bernie Sander's website. That negates any facts in the report. |

|

|

|

[#18]

Link

According to Freddie Mac, the national average commitment rate for a 30-year, conventional, fixed-rate mortgage fell to a record low 4.11 percent in September, down from 4.27 percent in August; the rate was 4.35 percent in September 2010. Contract failures were reported by 18 percent of NAR members in September, unchanged from August; they were 9 percent in September 2010. Contract failures are cancellations caused by declined mortgage applications, failures in loan underwriting from appraised values coming in below the negotiated price, or other problems including home inspections and employment losses. That's a good sign, right? |

|

|

|

[#19]

Quoted:

STRATFOR is doing a special this weekend on what to do wrt Greece. Here's their flowchart promo: http://i52.tinypic.com/117en8o.jpg Anyone a subscriber who can fill us in on the details? alpha, while I am not a subscriber to STRATFOR's offerings, I'm confident that I can complete that flowchart with a reasonable degree of accuracy with regards to what is actually at stake. Folks, the stakes are high- higher than they've ever been, and that includes the very worst of 2008/2009. While sitting here typing this post, part of me simply refuses to believe that, despite the untold trillions being hurled at it's credit/debt lattice to avert abject systemic implosion, the US-dominated world financial order is still lurching ever so inexorably closer to a worst-case eventuality I envisioned over four years ago. The kill-shot play now on the table is thus: (1)A disorderly European sovereign default triggers (2)a series of Credit Events, (3)detonating derivatives positions held by primary dealers and/or systemically significant banks and financial firms, which (4)cannot be successfully backstopped with central bank liquidity (virtual counterfeit) due to fiscal/political factors. The consequent (5)avalanche of bank defaults and hedge fund implosions rapidly accelerate to the point where (6)no action taken by any government or banking authority can possibly respond quickly enough, with enough System Liquidity (SL) to brake what has, by now, mushroomed into a... ... (7) self-sustaining and geometrically cascading financial, fiscal and ultimately, economic equivalent of a multi-megaton fission/fusion thermonuclear bomb, whose blast, via Euro CDS held by American financial firms & the Primary Dealer System, (8)backdrafts into the American financial system... This current iteration of the Global Financial Order, having achieved a critical mass of debt, simply seizes up, implodes, and self-incinerates into the nothingness from whence it emanated. If you have not taken adequate countermeasures, it could also incinerate your livelihood along with much of what you've already worked for.

-It's getting way late in the midst of an exceedingly complex subject, so here's the short version. Should such a scenario result from the ongoing financial crisis: Neighbor, I guarantee you that the we would then stand in grave danger of finding ourselves, in four to eight months, at economic depths that took four years for America to sink to after the credit(-DEBT)/equities crash of 1929. |

|

|

|

[#20]

What is your definition of "adequate countermeasures?"

|

|

|

|

[#21]

We can also look at the numbers directly from here. (2nd qtr)

If I believe what the too-big-to-exist banks told the gubmint (which I don't), their "net credit exposure" is supposedly only $364 billion. This, of course, is complete fantasy. Why? Let's look further: - Interest rate derivatives total 82% of the derivatives reported. This is why the Fed CANNOT raise interest rates here in the US. Some of these interest rate derivative products might also be based on foreign rates, probably European, in which case if the EMU goes sideways, the euro-based interest rates skyrocket and these guys take it in the shorts. If only 25% of these are euro based, a sudden interest rate jump would fry all of them. They are already likely seeing losses in the tens of billions on these since euro interest rates have been rising. - Credit derivatives supposedly "only" comprise $15.2 TRILLION. Probably quite a few of these have some euro exposure. If there is a cascade euro default (Greece goes which takes down France then Italy, Spain, and finally Germany), then the majority of these go <poof>. - Since the total net notional is $249 TRILLION and we can assume that these turds are leveraged at roughly 75:1 in that regard, their real "net exposure" is likely to be about 3.3 TRILLION. The Fed can't print that kind of scratch into existence overnight. So, if they are triggered, they are done/toast/kaput. Bottom line is that it really only takes a fraction of these derivatives to be triggered to cause a cascade failure here. Note that the "other side of the trade" for the majority of these bogus paper scams is other derivative holders. Ergo, the top 5 banks currently are engaged in a mutual suicide pact and we the taxpayers are being held hostage as a result. Keep in mind, too, that these 10lb. ticks on the 5lb. dog use deposited money as their leverage to do all this lovely "investing". As the economy gets worse and/or a European collapse begins to occur, people with lots of money in these banks will want their cash RFN. This will be the equivalent of a bank run, only in hours, not months. (This is supposedly what started to happen in 2008 when the gubmint stepped in.) Since the depositors cash is leveraged, the first to get theirs out may have a chance to get their cash. Everybody else will have to wait or see their stash vaporize. Remember, BlightOnAmerica transferred all their derivatives to the FDIC "insured" depositor institution to keep their "counterparty" happy. So, in case of <poof> these derivatives would vaporize all the deposits and the FDIC would be on the hook for coming up with every cent of the money you have in the bank. P.S. The FDIC doesn't have close to enough money to cover the depositors on even ONE of the TBTF banks. What happens when the top 5 all fail simultaneously? This is why the goobermint has been terrorized by these pond scum. P.P.S. "Adequate countermeasures" would include taking your money out of the TBTF banks NOW before you are unable to do so. In addition, Kyle Bass has also suggested "guns and gold". (See here) |

|

|

|

[#22]

Inflationary price increases are becoming slightly noticeable. Still no collapse. Gonna be some people pissed off at Obummer come 2012 though if it keeps up.

|

|

|

|

[#23]

Quoted: Inflationary price increases are becoming slightly noticeable. Still no collapse. Gonna be some people pissed off at Obummer come 2012 though if it keeps up. If? Are you still just exploring the random possibilities?  You're just one of our college overly-educated shills, aren't you? We've grown sick of you and your ilk. One defensive post at a time. "if" it keeps up.... fuck off. Check the score. The inflation began before you drank the Rolaids.

|

|

|

|

[#24]

Quoted:

Quoted:

Inflationary price increases are becoming slightly noticeable. Still no collapse. Gonna be some people pissed off at Obummer come 2012 though if it keeps up. If? Are you still just exploring the random possibilities? You're just one of our college overly-educated shills, aren't you? We've grown sick of you and your ilk. One defensive post at a time. "if" it keeps up.... fuck off. Check the score. The inflation began before you drank the Rolaids. Dial it back man... You can't convince everyone, nor should you try. It's not going to help anything if you get riled up and end up getting your account locked. Be glad you know what's up, and have prepared as much as you have. Compared to most, you're ahead if the game. |

|

|

|

[#25]

Quoted: "If" meaning people noticing it. It is very mild which is why most people are not outraged over the cost of products yet. It will have to affect the middle class more than just eating out a couple times less a month or aimlessly driving around less before something is done about it. And something will be done about it. No collapse. Just reaction. Just like Carter. Quoted: Inflationary price increases are becoming slightly noticeable. Still no collapse. Gonna be some people pissed off at Obummer come 2012 though if it keeps up. If? Are you still just exploring the random possibilities? You're just one of our college overly-educated shills, aren't you? We've grown sick of you and your ilk. One defensive post at a time. "if" it keeps up.... fuck off. Check the score. The inflation began before you drank the Rolaids. You are pretty far off on your assumptions about me but you seem to be the one getting defensive and aggressive. Maybe this friday you will be vindicated and the big collapse will happen. That will teach me a lesson for sure. |

|

|

|

[#26]

Quoted:

We can also look at the numbers directly from here. (2nd qtr) If I believe what the too-big-to-exist banks told the gubmint (which I don't), their "net credit exposure" is supposedly only $364 billion. This, of course, is complete fantasy. Why? Let's look further: - Interest rate derivatives total 82% of the derivatives reported. This is why the Fed CANNOT raise interest rates here in the US. Some of these interest rate derivative products might also be based on foreign rates, probably European, in which case if the EMU goes sideways, the euro-based interest rates skyrocket and these guys take it in the shorts. If only 25% of these are euro based, a sudden interest rate jump would fry all of them. They are already likely seeing losses in the tens of billions on these since euro interest rates have been rising. - Credit derivatives supposedly "only" comprise $15.2 TRILLION. Probably quite a few of these have some euro exposure. If there is a cascade euro default (Greece goes which takes down France then Italy, Spain, and finally Germany), then the majority of these go <poof>. - Since the total net notional is $249 TRILLION and we can assume that these turds are leveraged at roughly 75:1 in that regard, their real "net exposure" is likely to be about 3.3 TRILLION. The Fed can't print that kind of scratch into existence overnight. So, if they are triggered, they are done/toast/kaput. Bottom line is that it really only takes a fraction of these derivatives to be triggered to cause a cascade failure here. Note that the "other side of the trade" for the majority of these bogus paper scams is other derivative holders. Ergo, the top 5 banks currently are engaged in a mutual suicide pact and we the taxpayers are being held hostage as a result. Keep in mind, too, that these 10lb. ticks on the 5lb. dog use deposited money as their leverage to do all this lovely "investing". As the economy gets worse and/or a European collapse begins to occur, people with lots of money in these banks will want their cash RFN. This will be the equivalent of a bank run, only in hours, not months. (This is supposedly what started to happen in 2008 when the gubmint stepped in.) Since the depositors cash is leveraged, the first to get theirs out may have a chance to get their cash. Everybody else will have to wait or see their stash vaporize. Remember, BlightOnAmerica transferred all their derivatives to the FDIC "insured" depositor institution to keep their "counterparty" happy. So, in case of <poof> these derivatives would vaporize all the deposits and the FDIC would be on the hook for coming up with every cent of the money you have in the bank. P.S. The FDIC doesn't have close to enough money to cover the depositors on even ONE of the TBTF banks. What happens when the top 5 all fail simultaneously? This is why the goobermint has been terrorized by these pond scum. P.P.S. "Adequate countermeasures" would include taking your money out of the TBTF banks NOW before you are unable to do so. In addition, Kyle Bass has also suggested "guns and gold". (See here) Part in red. I don't know about that. In September 2008, the fed deposited 8 trillion over night in accounts around the world to keep the money market zero balance accounts from seizing up. So I think they can do that with 3.3 trillion, but not 75 trillion. I have also read the exposure in bad paper is 249 trillion though, so I agree it's too big to be fixed. |

|

|

|

[#27]

The name of the game since 2007 is preventing the derivatives domino chain from starting. It continues in Europe. Every adjective used to define nonpayment of obligations - ie: default - is being used. Haircut, voluntary writedown, managed drawdown, soft restructuring, hard restructuring, etc. - there's hundreds of them used to define what is in fact a default.

The Dealbreaker: Barclays Sees A 50-60% Haircut As A CDS Trigger In our view, there is little doubt that a large notional haircut of c. 50-60% would be considered a credit event, consequently triggering CDS contracts. In our view, that resistance has been motivated by concerns on the potential impact of CDS-triggers across the European financial institutions (FIs) and, more broadly, on concerns on financial stability, in particular on the potential trigger of a bank run in Greek institutions and the scope for contagion to other EMU countries. Wow! Somebody actually has the balls to call nonpayment of up to 60% as a credit event?????? The nerve of these guys. Which leads to the question of the validity of CDS as a whole. You know for a fact that numerous entities are taking credit for having CDS as hedges on their books, making it look as if the "risky" investment instruments are properly hedged and of little risk to them. If a credit event can never happen or be financially engineered out of the system when needed, are the books of numerous entities as sound as they may look? As it stands now, the CDS issuing companies gladly take in the risk premium (with no requirement to have cash available to pay if an event occurs), the purchasing company gladly book the CDS as balancing risk and the STATE (taxpayer) pays both when the bet goes bad. |

|

|

|

[#28]

Quoted:

The name of the game since 2007 is preventing the derivatives domino chain from starting. It continues in Europe. Every adjective used to define nonpayment of obligations - ie: default - is being used. Haircut, voluntary writedown, managed drawdown, soft restructuring, hard restructuring, etc. - there's hundreds of them used to define what is in fact a default. The Dealbreaker: Barclays Sees A 50-60% Haircut As A CDS Trigger In our view, there is little doubt that a large notional haircut of c. 50-60% would be considered a credit event, consequently triggering CDS contracts. In our view, that resistance has been motivated by concerns on the potential impact of CDS-triggers across the European financial institutions (FIs) and, more broadly, on concerns on financial stability, in particular on the potential trigger of a bank run in Greek institutions and the scope for contagion to other EMU countries. Wow! Somebody actually has the balls to call nonpayment of up to 60% as a credit event?????? The nerve of these guys. Which leads to the question of the validity of CDS as a whole. You know for a fact that numerous entities are taking credit for having CDS as hedges on their books, making it look as if the "risky" investment instruments are properly hedged and of little risk to them. If a credit event can never happen or be financially engineered out of the system when needed, are the books of numerous entities as sound as they may look? As it stands now, the CDS issuing companies gladly take in the risk premium (with no requirement to have cash available to pay if an event occurs), the purchasing company gladly book the CDS as balancing risk and the STATE (taxpayer) pays both when the bet goes bad. CDS, either by design or as a by product have created the financial equivalent of Mutually Assured Destruction No one dares trigger a default because everyone is destroyed. We are now watching as nations do everything possible to prevent the first default at any cost since the alternative is MAD.

|

|

|

|

[#29]

It should comfort you to know that CDS are a minority in the estimated $250 Trillion in derivatives contracts held by five of the largest banks in the US.

Only God knows how this mess could blow up.

From here |

|

|

|

[#30]

Quoted:

Beginnings of STRATFOR's coverage: The European Banking Crisis, Part 1: Assessing the Damage October 21, 2011 Europe faces a banking crisis it has not wanted to admit even exists. The formal authority on financial stability, International Monetary Fund (IMF) chief Christine Lagarde, made her institution’s opinion on European banking known back in August when she prompted the European Union to engage in an immediate 200 billion-euro bank recapitalization effort. The response was broad-based derision from Europeans at the local, national and EU bureaucratic levels. The vehemence directed at Lagarde was particularly notable as Lagarde is certainly in a position to know what she was talking about: Until July 5, her title was not IMF chief, but French finance minister. She has seen the books, and the books are bad. Due to European inaction, the IMF on Oct. 18 raised its estimate for recapitalization needs from 200 billion euros to 300 billion euros ($274 billion to $410 billion). Link Full disclosure - I have not read any of this yet. Dang it, alpha!!

Anyway, thanks for the info; parsing it now. |

|

|

|

[#31]

Quoted:

Quoted:

Beginnings of STRATFOR's coverage: The European Banking Crisis, Part 1: Assessing the Damage October 21, 2011 Europe faces a banking crisis it has not wanted to admit even exists. The formal authority on financial stability, International Monetary Fund (IMF) chief Christine Lagarde, made her institution’s opinion on European banking known back in August when she prompted the European Union to engage in an immediate 200 billion-euro bank recapitalization effort. The response was broad-based derision from Europeans at the local, national and EU bureaucratic levels. The vehemence directed at Lagarde was particularly notable as Lagarde is certainly in a position to know what she was talking about: Until July 5, her title was not IMF chief, but French finance minister. She has seen the books, and the books are bad. Due to European inaction, the IMF on Oct. 18 raised its estimate for recapitalization needs from 200 billion euros to 300 billion euros ($274 billion to $410 billion). Link Full disclosure - I have not read any of this yet. Dang it, alpha!!

Anyway, thanks for the info; parsing it now. The bitch is to get part 2 you have to join. |

|

|

|

[#32]

To aid in answering my previous question:

What Happens If Europe Crushes the Swap Market? The Financial Times is reporting that bankers fear the CDS market could be “killed stone dead” if a large haircut does not count as a "credit event" triggering CDS payouts. This makes sense. After all, what's the point of buying protection on bonds that doesn't payoff in the event that the bonds are suddenly only worth—at best—half of their face value? .... But the European leaders misunderstand the CDS market and its relationship to the bond market. The CDS market serves two important purposes: It's both a hedge for investors and an indicator of how risky the market thinks certain bonds are. Many investors are able to buy more of a country's bonds because they can reduce their risk by purchasing swaps that pay off in a default. And the price of the swaps is an indicator—albeit not always a reliable one—of the riskiness of the underlying bonds. In short, the CDS market provides liquidity and transparency to the bond market. .... In short, European leaders may get what they wish for—and that might wind up working out very badly for them. I'll try some layman's terms here: I might be interested in buying a countries debt if I can hedge it with an instrument that provides protection from loss but still allows a profit from interest on the debt I bought. If I can't trust the hedging/insurance instrument, I would be less likely to buy the contries debt. With many countries straining to sell debt, including the USA at times, noss of confidence in the CDS market may make some less likely to buy soverign debt................or any debt for that matter. That's why the article mentions the spillover into corporate debt. Adding: The naked CDS works something like this. I know for a fact that, let's say RRA223, is a horrible driver. He's totaled three cars in the last year. Knowing this, I take out an insurance policy on his new car he just got after his last accident. I pay a modest premium for this "insurance". He also has an insurance policy on that car. I tell my friends of my new found sure-thing investment. They also buy insurance on RRA's car. Sure as shit, RRA wipes out another $20k car. He gets paid for his loss through his insurance policy. I ALSO GET A $20K SETTLEMENT OUT OF THAT SAME CAR. ALL OF MY FRIENDS GET $20K OUT OF THE INCIDENT. A one time $20k material loss ends up costing the insuring entity $20k X the number of "naked insurance policies" out there. Ever wonder why AIG needed $180Billion and counting? |

|

|

|

[#33]

So... umm.. I think Greece just defaulted.

http://www.zerohedge.com/news/we-have-deal I'm still trying to sort out who is taking haircuts (read default of obligation to pay back a loan) and who is being spared. So far I'm reading that the Greeks pension bonds as well as individual investors took a 50% haircut, but that several other bond holders are shielded. http://www.zerohedge.com/news/here-how-50-greek-haircut-actually-just-28 The announcement came at 03:00 their time, so I guess they've been up all night figuring this shit out. Zerohedge is bustling with folks trying to figure this out. Barclays says 50% is a default: http://www.zerohedge.com/news/barclays-explains-why-50-greek-haircut-would-be-considered-credit-event-consequently-triggering On the surface it appears that the banks are in charge of determining what a "credit event" is that will trigger Credit Default Swaps, so at least for now, they appear to have deemed 50% as a non CDS triggering event.... But even if they've somehow managed to cut their debt load in half without triggering the CDS bomb and tanking the world, they now have to tell the Greek people that their pension funds have just been cut in half.... |

|

|

|

[#34]

And yet the DOW is at an insane level of 11900 and futures show an open +125.

It's all on the up and up. Yeah, right. I would not be surprise to see us back in the mid 10's by Friday. |

|

|

|

[#35]

Quoted: So... umm.. I think Greece just defaulted. http://www.zerohedge.com/news/we-have-deal I'm still trying to sort out who is taking haircuts (read default of obligation to pay back a loan) and who is being spared. So far I'm reading that the Greeks pension bonds as well as individual investors took a 50% haircut, but that several other bond holders are shielded. http://www.zerohedge.com/news/here-how-50-greek-haircut-actually-just-28 The announcement came at 03:00 their time, so I guess they've been up all night figuring this shit out. Zerohedge is bustling with folks trying to figure this out. Barclays says 50% is a default: http://www.zerohedge.com/news/barclays-explains-why-50-greek-haircut-would-be-considered-credit-event-consequently-triggering On the surface it appears that the banks are in charge of determining what a "credit event" is that will trigger Credit Default Swaps, so at least for now, they appear to have deemed 50% as a non CDS triggering event.... But even if they've somehow managed to cut their debt load in half without triggering the CDS bomb and tanking the world, they now have to tell the Greek people that their pension funds have just been cut in half.... http://finance.yahoo.com/news/Europe-reaches-key-deal-to-apf-3214664161.html?x=0&sec=topStories&pos=6&asset=&ccode= |

|

|

|

[#36]

So bondholders lose 50%, Greece's debt load is reduced to a still unsustainable 120% of GDP, Greeks see their pension fund reduced by 50% over night, and Credit Default Swaps don't trigger because banks on the ISDA changed what "default" means, negating that whole section of "assets".

So, if you bought CDS on Greek debt you just watched Greece basically default and yet were denied pay off on your insurance. Basically it took two years for the EU to find a way to circumvent the rules in order to get their cake AND eat it. Bank of America strategists offered their thoughts on the subject: "A substantial debt haircut in Greece that is designed in a way that does not trigger CDS contracts could question the whole sovereign CDS insurance market" A sovereign market with no access to CDS is likely to have profound negative effects on the world economy. Firstly, banks all over the world will dump all of the bond exposure that they have to the Euro area which will make the situation in Greece look like child's play. A mass exodus from European debt would, without any doubt, bring down the whole of the Eurozone in one fell swoop. Secondly, a lack of CDS protection would drive up the cost of borrowing globally and not just in Europe. Making the deleveraging process not just faster but also a lot deeper than the current credit conditions provide. So this deal IS NOT final (what's new) and it's down to lawyers, bankers, and bureaucrats to decide! JOY! On a related note, Firefox's spell checker doesn't have DEleverage in the bank, only leverage. |

|

|

|

[#37]

Unintended consequences can be a bitch.

|

|

|

|

[#38]

It's all over.

Greek bond holders are going to "voluntarily" take a 50% haircut to "solve" the Greek crisis. This will end the shenanigans after the initial 21% haircut in June failed to stem the hemorrhaging. Thankfully, because this is "voluntary," no CDS covering will be triggered, this will be considered a non-credit event and the perpetual bull market goes on.

All we need now are some voluntary write-offs in Italy, Spain, Portugal, Great Britain and maybe the US?

http://www.zerohedge.com/news/farce-complete-isda-finds-50-haircut-not-credit-event |

|

|

|

[#39]

So, is the Stock Market going to have a huge rally today, as Greek Default fears abate? |

|

|

|

[#40]

Quoted: So, is the Stock Market going to have a huge rally today, as Greek Default fears abate? Rallying around the world as we speak. |

|

|

|

[#41]

Quoted:

Quoted:

So, is the Stock Market going to have a huge rally today, as Greek Default fears abate? Rallying around the world as we speak. +1 Hundreds of billions of dollars in "assests" held by dozens of international banks will now have to be devalued by 50% to avoid catastrophe - after THREE YEARS of bickering, compromising and other austerity measures implimented without any success in keeping the Eurozone's smallest economy afloat so far - all of this is now bullish. BTFD. |

|

|

|

[#42]

ZH puts it this way:

You buy fire insurance on your neighbor's house, then you light your neighbor's house on fire, only to find out the insurance policy was canceled. |

|

|

|

[#43]

Quoted:

ZH puts it this way: You buy fire insurance on your neighbor's house, then you light your neighbor's house on fire, only to find out the insurance policy was canceled. Except that your neighbor set his own house on fire. |

|

|

|

[#44]

I've said many times that the Euro thing won't be over until they decide who loses money. Somebody was going to have to get fucked.

Looks like the bondholders losing money are going to be part of the solution. http://www.bloomberg.com/news/2011-10-27/merkel-cements-eu-leadership-role-as-she-seeks-to-win-back-german-voters.html Addressing lawmakers before she left Berlin, Merkel said that the summit’s main goal would be to cut Greece’s debt to 120 percent of gross domestic product by 2020, a level that international creditors said last week could be achieved if bondholders accepted voluntary 50 percent losses. Banks bowed to pressure today to accept a 50 percent haircut on Greek debt after Merkel made clear it was European leaders’ "last word.” This won't be the end of the fucking however. There is more debt losses to be doled out. |

|

|

|

[#45]

Quoted:

ZH puts it this way: You buy fire insurance on your neighbor's house, then you light your neighbor's house on fire, only to find out the insurance policy was canceled. Except that that only applies to "naked CDS" bets. Many banks bought CDSes on the "houses" that they themselves "owned". The "voluntary write-down" nonsense means that the banks insured their own houses, the Greek government lit the houses on fire, and now the EU is telling the banks that they have to "voluntarily" give up any claim to payment from their own insurance policies. |

|

|

|

[#46]

Quoted: Quoted: Quoted: So, is the Stock Market going to have a huge rally today, as Greek Default fears abate? Rallying around the world as we speak. +1 Hundreds of billions of dollars in "assests" held by dozens of international banks will now have to be devalued by 50% to avoid catastrophe - after THREE YEARS of bickering, compromising and other austerity measures implimented without any success in keeping the Eurozone's smallest economy afloat so far - all of this is now bullish. BTFD. Maybe, this will be sort of a good thing, if it decreases the credibility and popularity of Credit Default Swaps. Anyway, it was good to me so far. I'm up the equivalent of a couple 6920's w / Larue mounts and optics. |

|

|

|

[#47]

Greece Default Swaps Failure to Trigger Casts Doubt on Contracts as Hedge

“It will raise some very serious question marks over the value of CDS contracts,” said Harpreet Parhar, a strategist at Credit Agricole SA in London. “For euro sovereigns in particular, the CDS market is likely to remain wary.” .... This approach threatens to affect banks that use credit- default swaps to hedge their holdings of government bonds, forcing them to look at other ways of laying off risk. “It punishes the banks that were well-hedged and managed, and I think it’s just starting to sink in as to what this might mean,” said Peter Tchir, the founder of hedge fund TF Market Advisors in New York. “Bank hedging desks are definitely now trying to re-evaluate” their use of default swaps, he said. .... “If they find a way to avoid a trigger event in the CDS, then people will doubt the value of credit-default swaps in general, leading to more dislocations in the market,” said Pilar Gomez-Bravo, the senior adviser at Negentropy Capital in London, which oversees about 200 million euros. .... “It is symptomatic of the regulatory and legal goalposts being constantly shifted either randomly or to suit political interests,” said Marc Ostwald, a fixed-income strategist at Monument Securities Ltd. in London. “For genuine long-term investors, either financial or non-financial, it’s a major liability.” More here |

|

|

|

[#48]

T$PTB: Credit Events

"Meh! We'll just make up the rules as we go along- no one'll notice."

|

|

|

|

[#49]

Quoted:

So... umm.. I think Greece just defaulted. C'mon TDT, what in heck would give ya such a crazy notion?!

|

|

|

|

[#50]

Quoted:

Quoted:

So... umm.. I think Greece just defaulted. C'mon TDT, what in heck would give ya such a crazy notion?!

A default by any other name ISN'T a default |

|

|

AR15.COM is the world's largest firearm community and is a gathering place for firearm enthusiasts of all types.

From hunters and military members, to competition shooters and general firearm enthusiasts, we welcome anyone who values and respects the way of the firearm.

Subscribe to our monthly Newsletter to receive firearm news, product discounts from your favorite Industry Partners, and more.

Copyright © 1996-2024 AR15.COM LLC. All Rights Reserved.

Any use of this content without express written consent is prohibited.

AR15.Com reserves the right to overwrite or replace any affiliate, commercial, or monetizable links, posted by users, with our own.