NC, USA

|

Posted: 3/13/2024 11:11:41 AM EDT

[Last Edit: DV8EDD]

I'm feeling lost with no defined strategy other than throw money at things and have seen some good advice in here recently. Figured I'd ask b/c I'm having a tough time figuring out what to do about pre versus post tax contributions.

Roth or just contribute to post tax 401k? Change all 401k contributions from pre-tax to Roth? Both? Consolidate any of this stuff? Totally overthinking it? |

|

|

OK, USA

|

[Last Edit: GlockPride]

[#1]

Max the Roth for you and the wife, first. Main reason is that it GROWS and WITHDRAWS tax-free.

After that, then I’d add to a non-retirement/non-tax advantaged account. I’d probably also drop down the % of large cap stocks owned with some smaller small & mid caps with aggressive growth. If you feel like being a little defensive you could add some T-bill ETF’s or bonds (but I don’t generally like them). The wife and I are moderate to somewhat aggressive with our 401k’s, but heavily aggressive in our Roth’s. We are both mid-40’s and look at the Roth as our fun money for retirement. |

|

|

NC, USA

|

[#2]

Originally Posted By GlockPride: Max the Roth for you and the wife, first. Main reason is that it GROWS and WITHDRAWS tax-free. After that, then I’d add to a non-retirement/non-tax advantaged account. I’d probably also drop down the % of large cap stocks owned with some smaller small & mid caps with aggressive growth. If you feel like being a little defensive you could add some T-bill ETF’s or bonds (but I don’t generally like them). The wife and I are moderate to somewhat aggressive with our 401k’s, but heavily aggressive in our Roth’s. We are both mid-40’s and look at the Roth as our fun money for retirement. Definitely doing that for now but wondering if I should be doing something different to grow the post tax contributions while minimizing future tax impact. |

|

|

USA

|

[#3]

Originally Posted By DV8EDD: Definitely doing that for now but wondering if I should be doing something different to grow the post tax contributions while minimizing future tax impact. Post tax contributions should only be used if your plan allows for mega backdoor Roth conversions. Otherwise it doesn’t make sense from a tax standpoint. From your descriptions you should be maxing you and your wife’s Roth IRA, making 401k Roth contributions up to the employer match, max HSA if available, then go back and max the 401k. Any money left after that can go into mega backdoor Roth conversions if your plan allows some would advise brokerage, but that really only matters if you want to be able to withdraw money in the short term. Otherwise mega backdoor is way more tax efficient and allows for legacy planning. |

|

|

NC, USA

|

[Last Edit: DV8EDD]

[#4]

Originally Posted By Joe_Blacke: Post tax contributions should only be used if your plan allows for mega backdoor Roth conversions. Otherwise it doesn’t make sense from a tax standpoint. From your descriptions you should be maxing you and your wife’s Roth IRA, making 401k Roth contributions up to the employer match, max HSA if available, then go back and max the 401k. Any money left after that can go into mega backdoor Roth conversions if your plan allows some would advise brokerage, but that really only matters if you want to be able to withdraw money in the short term. Otherwise mega backdoor is way more tax efficient and allows for legacy planning. so Roth contributions to the 401k should take precedent over pre-tax? ETA: my after tax contributions are automatically converted to Roth within my 401k plan. So I'm maxing pre-tax at the annual limit then I'm also contributing after tax which is auto converted. |

|

|

USA

|

[Last Edit: Joe_Blacke]

[#5]

Originally Posted By DV8EDD: so Roth contributions to the 401k should take precedent over pre-tax? ETA: my after tax contributions are automatically converted to Roth within my 401k plan. So I'm maxing pre-tax at the annual limit then I'm also contributing after tax which is auto converted. Unless your state income taxes are higher than 5%, Roth makes the most sense. Roth contributions are always after tax. 401kplans can have 3 types of contributions. Pre-tax, Roth and after tax. Pre tax and Roth are affected by the max contribution limit. After tax is best used after pre-tax and Roth are maxed. 401k plan have much higher limits when you use after tax in this manner and can allow you to move those $$ out of the plan to a Roth IRA. If the money stays in your plan it isn’t Roth. Any gains will be taxable for after tax contributions you dont move to a Roth |

|

|

|

[Last Edit: FALARAK]

[#6]

1. Max out your 401k elective deferral contribution. You want to capitalize fully on the match, and the tax advantaged status. Whether you choose Roth 401k or Pre-Tax depends on a LOT of factors. People argue for days over this. Since you have access to a Mega Backdoor Roth to get a LOT of money into Roth status, I personally choose pre-tax for the 401k contribution. You don't have a huge nest egg here in what we are seeing at age 49, and you don't have a LOT of time for tax-free growth. But you DO want a chunk of Roth at retirement to control your taxable income.

2. You didn't mention HSA. If you have a HDHCP then you should max out an HSA, do not spend it, and invest it into market equities. 3. Since you are Mega Backdoor Roth eligible, there is no reason to mess with a direct contribution to a Roth IRA, until you are maxing out the mega backdoor Roth. For instance, the 401k defined contribution limit from all sources is $69,000. If you max your elective deferral of $23,000, then get a company match of $7000, you have $39,000 left to contribute. You can contribute up to $39,000 into the 401k from payroll to AFTER-TAX, which is set to auto-convert to a Roth status sub-account inside the 401k. If you are not filling this bucket, there is no real need to mess with a direct contribution to a Roth IRA (or a Backdoor Roth IRA since you are getting VERY close to the MAGI threshold for direct Roth contributions which currently starts at $230,000 for MFJ.) The mega Backdoor Roth has no income limitations, so take advantage of this while it is available. Congress tries to close this down but has not been successful yet. Once you are filling the Mega-Backdoor ROTH fully, THEN you can consider contributing to a ROTH IRA either directly or backdoor. The exception to this might be your wife's Roth IRA, because funding this doesn't have to come from payroll (assuming you have savings that can contribute to this, and you just want to get more individual retirement funds in her name) 4. In the YEAR you turn 50, you qualify for catchup contributions. So, if you will turn 50 sometime in 2024, you can contribute an additional $7,500 to your 401k, either Pre-Tax or Roth (for now). I choose pre-tax for this. 5. Do the ESPP regardless of anything above, just sell the stock immediately and capture your discount. Free money. And you only tie up 3 months of contributions at a time, which are returned when you sell each quarter. These are my generic Investing order of operations: 1. Pay off all toxic debt (credit cards, high interest rates). 2. NEVER carry a balance on a credit card month to month. This is called "paying the stupid tax". 3. Build an emergency fund of 6-12 months of *expenses* and keep it liquid, such as in a High Yield Savings Account (HYSA) or Money Market Fund (MMF) 4. Contribute to your 401k up to the company match maximum. 5. Contribute to an HSA if offered up to the maximum allowed. 6. If your 401k plan allows, contribute to a Mega Backdoor Roth. https://thecollegeinvestor.com/17561/understanding-the-mega-backdoor-roth-ira 7. If you do not have access to a Mega Backdoor Roth through your 401k, contribute to a ROTH IRA (unless income ineligible, then use Backdoor Roth IRA method. https://thecollegeinvestor.com/38006/how-to-do-a-backdoor-roth-ira 8. Go back and finish contributing to the 401k plan, up to the maximum limit ($23,000 in 2024). 9. If offered a Company Stock plan (ESPP/ESOP) that gives you shares at a discount, AND you can sell immediately upon stock purchase, contribute the maximum amount to this program and sell each time. You should participate in this regardless of any choices or order of operations above. This runs in parallel to everything else. 10. Open a taxable brokerage account and begin investing here, and/or real estate, and/or side business. 11. Consider funding children's college in 529 plans or taxable brokerage account, or other state advantaged options. 12. Limit the amount of vehicle debt you carry, as vehicles can be one of the biggest barriers to building wealth as people believe they derive "happiness" from getting new vehicles often. Invest all of these in a low fee Total US Equities Market index fund (if offered) or an S&P500 index fund, to start. DONT TOUCH it. Just be steady and don't change, be careful who you listen to, and don't make emotion based moves into cash because what you just "know", likely is not so. Recommended reading: https://www.amazon.com/Simple-Path-Wealth-financial-independence/dp/1533667926 https://www.amazon.com/dp/1119847672?tag=arfcom00-20 https://www.amazon.com/Richest-Man-Babylon-Original-Classics/dp/B0C1J5ML66 https://www.amazon.com/The-Millionaire-Next-Door-audiobook/dp/B0000547HR |

|

|

|

|

[#7]

Originally Posted By Joe_Blacke: Roth contributions are always after tax. 401kplans can have 3 types of contributions. Pre-tax, Roth and after tax. Pre tax and Roth are affected by the max contribution limit. After tax is best used after pre-tax and Roth are maxed. 401k plan have much higher limits when you use after tax in this manner and can allow you to move those $$ out of the plan to a Roth IRA. If the money stays in your plan it isn’t Roth. Any gains will be taxable for after tax contributions you dont move to a Roth This is absolutely not correct. For the Mega Backdoor Roth - After-Tax contributions must be converted to Roth via an In-Plan conversion. At that point, they are Roth status. There is ZERO requirement to move them out of the plan and into a Roth IRA. That is just an optional step you can elect to take, to have broader investment options and easier access for early withdrawals of contributions. Should you elect to leave the in-plan converted funds in your 401k, they are held in a Roth sub-account and they grow tax-free. It is true only if you do NOT do an in-plan conversion. As stated earlier, it is pointless to contribute AFTER-TAX without in-plan conversion. If the funds stay in the AFTER TAX sub account, the earnings will be taxable. This is why Fidelity enabled an option for auto-conversion immediately upon contribution.

|

|

|

|

|

[#8]

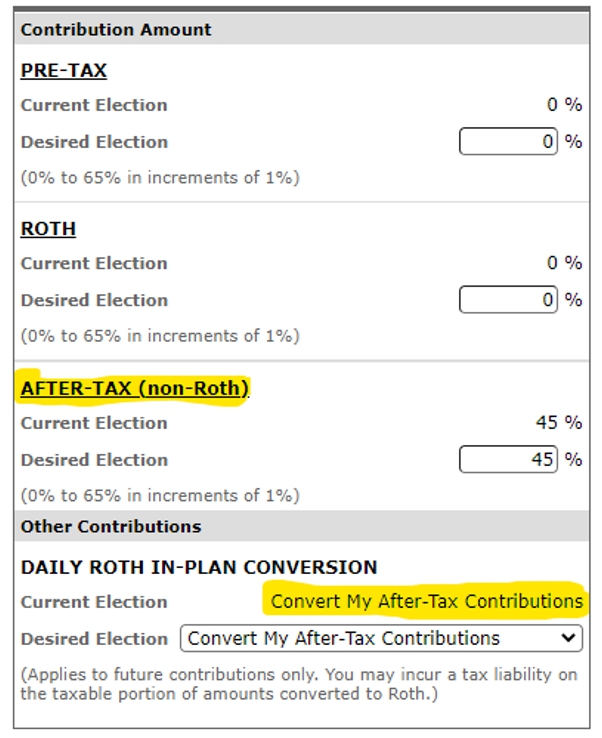

Originally Posted By DV8EDD: ETA: my after tax contributions are automatically converted to Roth within my 401k plan. So I'm maxing pre-tax at the annual limit then I'm also contributing after tax which is auto converted.  |

|

|

|

|

[#9]

It’s nice to have both pretax and post tax “buckets” available when you retire (or at least that’s what I’m hoping).

My 401(k) is decent. Need to make the Roth bigger now. |

|

|

|

USA

|

[Last Edit: Joe_Blacke]

[#10]

Originally Posted By FALARAK: This is absolutely not correct. For the Mega Backdoor Roth - After-Tax contributions must be converted to Roth via an In-Plan conversion. At that point, they are Roth status. There is ZERO requirement to move them out of the plan and into a Roth IRA. That is just an optional step you can elect to take, to have broader investment options and easier access for early withdrawals of contributions. Should you elect to leave the in-plan converted funds in your 401k, they are held in a Roth sub-account and they grow tax-free. It is true only if you do NOT do an in-plan conversion. As stated earlier, it is pointless to contribute AFTER-TAX without in-plan conversion. If the funds stay in the AFTER TAX sub account, the earnings will be taxable. This is why Fidelity enabled an option for auto-conversion immediately upon contribution. https://i.postimg.cc/Tw5q82np/screenshot-763.jpg Mega Backdoor Roth ideally means moving it to a Roth IRA. Otherwise it is really nothing more than just an in plan conversion. You do not need to convert to Roth inside your plan for mega backdoor Roth. You can convert after tax directly to a Roth IRA. With Fidelity you have to call them to get it done, but this allows you to get access to investments outside of your 401k. I would recommend you do a standard Roth before you do Mega Backdoor. When doing conversions there will be times when your intended conversion looses value before the conversion happens. That isn’t true with a direct contribution. Last two years I ended up loosing over $1,000 combined that wouldn’t get converted. I’d get paid on a Friday but Fidelity can’t process the conversion until after close the following Monday. Markets were down both days, so my $1500 that was supposed to go into Roth only had a value of around $1300 to $1350 by the time the conversion happened. For income taxes I was taxed on the whole $1500 even though my Roth only saw $1300(ish) come in for that pay period. For an “in kind” pre tax to Roth conversion that would be a good thing. For an after tax to Roth IRA megabackdoor conversion it isn’t great. Of course most years, this year included, I’m getting market gains for those two days to move more than the $1500 per pay period. The downside is that I’m taxed on my $1500 plus all the gains that get moved over. |

|

|

|

[Last Edit: FALARAK]

[#11]

Originally Posted By Joe_Blacke: Mega Backdoor Roth ideally means moving it to a Roth IRA. Otherwise it is really nothing more than just an in plan conversion. Originally Posted By Joe_Blacke: Mega Backdoor Roth ideally means moving it to a Roth IRA. Otherwise it is really nothing more than just an in plan conversion. No, it does not. Mega Backdoor Roth means the ability to contribute after-tax dollars and convert them to Roth status while inside the 401k. That's it. The movement to a personal Roth IRA account is 100% optional, and has nothing to do at all with the Mega Backdoor Roth process. You do not need to convert to Roth inside your plan for mega backdoor Roth Yes you do. It is a requirement for it to be an in-plan conversion. You can convert after tax directly to a Roth IRA. No, you cannot. It is two steps. Your custodian may have made it "seem" like it wasn't, but it absolutely is, because the latter is optional. The 401k plan MUST support an in-plan conversion. With Fidelity you have to call them to get it done, but this allows you to get access to investments outside of your 401k. Yes, I do it every year. But it is called a sweep, or a transfer. It is NOT part of the Mega Backdoor process. The plan simply allows for this to be allowed, once they have been converted to Roth status in the sub account, via in-plan conversion. I would recommend you do a standard Roth before you do Mega Backdoor. When doing conversions there will be times when your intended conversion looses value before the conversion happens. Fidelity supports auto-conversion, which are done immediately upon contribution. There is no gain nor loss. I don't know why yours does not auto-convert. Mine is instant, upon the after-tax contribution from payroll. There is never a gain nor loss. |

|

|

|

USA

|

[Last Edit: Joe_Blacke]

[#12]

Originally Posted By FALARAK: No, it does not. Mega Backdoor Roth means the ability to contribute after-tax dollars and convert them to Roth status while inside the 401k. That's it. The movement to a personal Roth IRA account is 100% optional, and has nothing to do at all with the Mega Backdoor Roth process. Yes you do. It is a requirement for it to be an in-plan conversion. No, you cannot. It is two steps. Your custodian may have made it "seem" like it wasn't, but it absolutely is, because the latter is optional. The 401k plan MUST support an in-plan conversion. Yes, I do it every year. But it is called a sweep, or a transfer. It is NOT part of the Mega Backdoor process. The plan simply allows for this to be allowed, once they have been converted to Roth status in the sub account, via in-plan conversion. Fidelity supports auto-conversion, which are done immediately upon contribution. There is no gain nor loss. I don't know why yours does not auto-convert. Mine is instant, upon the after-tax contribution from payroll. There is never a gain nor loss. Nope you are wrong. In plan conversions are still better than leaving money in pre tax or straight after tax. However megabackdoor is really about getting around Roth IRA income and contribution limits. Otherwise you could just consider someone maxing out a Roth 401k contribution to be doing “mega Backdoor Roth”instead of just straight Roth contributions. https://www.usatoday.com/money/blueprint/retirement/mega-backdoor-roth/ From the article: A mega backdoor Roth involves converting after-tax 401(k) contributions to a Roth IRA. Also: To use a mega backdoor Roth, your employer-sponsored plan must allow after-tax contributions and in-service withdrawals. Graphic from Bogleheads There is zero requirement to move it to Roth inside your 401k. Your plan doesn’t need to allow in-plan conversions. It needs to allow in service withdrawals. I’ve been doing it with Fidelity for years. I’d much rather have the money inside a Roth IRA instead of a 401k for better investment options and lower fees. The only reason I’d just do in plan conversions is for the rule of 55. However in my case I need to spend down a massive pre-tax balance in my 401k so I’ll use that, rather than convert it all to Roth, after I retire to help minimize RMD, plus have my pension. I still won’t collect SS until 70. |

|

|

|

[#13]

The biggest question is when do you plan to quit working? What about the wife?

Having the appropriate amounts of pre and post tax money makes a huge difference once you retire. You can opt to withdraw money from pre-tax or post-tax accounts to make your taxable income whatever is best for your situation. In general, roth is more flexible since you can withdraw anytime tax-free and it has no RMDs. Investing is pretty easy, but planning is more valuable the closer you get to retirement. Planning to avoid taxes can easily save you a 6 figure amount of money over your retirement years. |

|

|

|

NC, USA

|

[#14]

Originally Posted By FALARAK: 1. Max out your 401k elective deferral contribution. You want to capitalize fully on the match, and the tax advantaged status. Whether you choose Roth 401k or Pre-Tax depends on a LOT of factors. People argue for days over this. Since you have access to a Mega Backdoor Roth to get a LOT of money into Roth status, I personally choose pre-tax for the 401k contribution. You don't have a huge nest egg here in what we are seeing at age 49, and you don't have a LOT of time for tax-free growth. But you DO want a chunk of Roth at retirement to control your taxable income. 2. You didn't mention HSA. If you have a HDHCP then you should max out an HSA, do not spend it, and invest it into market equities. 3. Since you are Mega Backdoor Roth eligible, there is no reason to mess with a direct contribution to a Roth IRA, until you are maxing out the mega backdoor Roth. For instance, the 401k defined contribution limit from all sources is $69,000. If you max your elective deferral of $23,000, then get a company match of $7000, you have $39,000 left to contribute. You can contribute up to $39,000 into the 401k from payroll to AFTER-TAX, which is set to auto-convert to a Roth status sub-account inside the 401k. If you are not filling this bucket, there is no real need to mess with a direct contribution to a Roth IRA (or a Backdoor Roth IRA since you are getting VERY close to the MAGI threshold for direct Roth contributions which currently starts at $230,000 for MFJ.) The mega Backdoor Roth has no income limitations, so take advantage of this while it is available. Congress tries to close this down but has not been successful yet. Once you are filling the Mega-Backdoor ROTH fully, THEN you can consider contributing to a ROTH IRA either directly or backdoor. The exception to this might be your wife's Roth IRA, because funding this doesn't have to come from payroll (assuming you have savings that can contribute to this, and you just want to get more individual retirement funds in her name) 4. In the YEAR you turn 50, you qualify for catchup contributions. So, if you will turn 50 sometime in 2024, you can contribute an additional $7,500 to your 401k, either Pre-Tax or Roth (for now). I choose pre-tax for this. 5. Do the ESPP regardless of anything above, just sell the stock immediately and capture your discount. Free money. And you only tie up 3 months of contributions at a time, which are returned when you sell each quarter. These are my generic Investing order of operations: 1. Pay off all toxic debt (credit cards, high interest rates). 2. NEVER carry a balance on a credit card month to month. This is called "paying the stupid tax". 3. Build an emergency fund of 6-12 months of *expenses* and keep it liquid, such as in a High Yield Savings Account (HYSA) or Money Market Fund (MMF) 4. Contribute to your 401k up to the company match maximum. 5. Contribute to an HSA if offered up to the maximum allowed. 6. If your 401k plan allows, contribute to a Mega Backdoor Roth. https://thecollegeinvestor.com/17561/understanding-the-mega-backdoor-roth-ira 7. If you do not have access to a Mega Backdoor Roth through your 401k, contribute to a ROTH IRA (unless income ineligible, then use Backdoor Roth IRA method. https://thecollegeinvestor.com/38006/how-to-do-a-backdoor-roth-ira 8. Go back and finish contributing to the 401k plan, up to the maximum limit ($23,000 in 2024). 9. If offered a Company Stock plan (ESPP/ESOP) that gives you shares at a discount, AND you can sell immediately upon stock purchase, contribute the maximum amount to this program and sell each time. You should participate in this regardless of any choices or order of operations above. This runs in parallel to everything else. 10. Open a taxable brokerage account and begin investing here, and/or real estate, and/or side business. 11. Consider funding children's college in 529 plans or taxable brokerage account, or other state advantaged options. 12. Limit the amount of vehicle debt you carry, as vehicles can be one of the biggest barriers to building wealth as people believe they derive "happiness" from getting new vehicles often. Invest all of these in a low fee Total US Equities Market index fund (if offered) or an S&P500 index fund, to start. DONT TOUCH it. Just be steady and don't change, be careful who you listen to, and don't make emotion based moves into cash because what you just "know", likely is not so. Recommended reading: https://www.amazon.com/Simple-Path-Wealth-financial-independence/dp/1533667926 https://www.amazon.com/dp/1119847672?tag=arfcom00-20 https://www.amazon.com/Richest-Man-Babylon-Original-Classics/dp/B0C1J5ML66 https://www.amazon.com/The-Millionaire-Next-Door-audiobook/dp/B0000547HR I really appreciate all the detail here and I think this confirms what I suspected concerning the 401k plan. The after-tax with auto conversion to Roth is new (year old) to my company's plan and I had never been exposed to this before. It's pretty recent that my career situation has allowed me more money to invest with pay going up and now living in a less expensive area. I'll adjust and add more to the after tax and stop contributing to the individual ROTH IRA since the plan limit is far higher than the individual account limit. I'll read through what you shared, thank you.

|

|

|

|

[#15]

Unable to answer:

You never state your income. Pre-tax works well for those in the highest tax brackets (state taxes too). If we are talking about you maxing out a $69,000 contribution, chances are you are in that bracket. If you are swinging a 30%+ highest marginal rate you would be better served to max your pre-tax/traditional contributions and get the 30+% "bonus" to contributions. You could then do the mega-roth conversions and backdoor roth after your $23,000 of tax deferred contributions are met. |

|

|

|

PA, USA

|

[#16]

Originally Posted By FALARAK: 1. Max out your 401k elective deferral contribution. You want to capitalize fully on the match, and the tax advantaged status. Whether you choose Roth 401k or Pre-Tax depends on a LOT of factors. People argue for days over this. Since you have access to a Mega Backdoor Roth to get a LOT of money into Roth status, I personally choose pre-tax for the 401k contribution. You don't have a huge nest egg here in what we are seeing at age 49, and you don't have a LOT of time for tax-free growth. But you DO want a chunk of Roth at retirement to control your taxable income. 2. You didn't mention HSA. If you have a HDHCP then you should max out an HSA, do not spend it, and invest it into market equities. 3. Since you are Mega Backdoor Roth eligible, there is no reason to mess with a direct contribution to a Roth IRA, until you are maxing out the mega backdoor Roth. For instance, the 401k defined contribution limit from all sources is $69,000. If you max your elective deferral of $23,000, then get a company match of $7000, you have $39,000 left to contribute. You can contribute up to $39,000 into the 401k from payroll to AFTER-TAX, which is set to auto-convert to a Roth status sub-account inside the 401k. If you are not filling this bucket, there is no real need to mess with a direct contribution to a Roth IRA (or a Backdoor Roth IRA since you are getting VERY close to the MAGI threshold for direct Roth contributions which currently starts at $230,000 for MFJ.) The mega Backdoor Roth has no income limitations, so take advantage of this while it is available. Congress tries to close this down but has not been successful yet. Once you are filling the Mega-Backdoor ROTH fully, THEN you can consider contributing to a ROTH IRA either directly or backdoor. The exception to this might be your wife's Roth IRA, because funding this doesn't have to come from payroll (assuming you have savings that can contribute to this, and you just want to get more individual retirement funds in her name) 4. In the YEAR you turn 50, you qualify for catchup contributions. So, if you will turn 50 sometime in 2024, you can contribute an additional $7,500 to your 401k, either Pre-Tax or Roth (for now). I choose pre-tax for this. 5. Do the ESPP regardless of anything above, just sell the stock immediately and capture your discount. Free money. And you only tie up 3 months of contributions at a time, which are returned when you sell each quarter. These are my generic Investing order of operations: 1. Pay off all toxic debt (credit cards, high interest rates). 2. NEVER carry a balance on a credit card month to month. This is called "paying the stupid tax". 3. Build an emergency fund of 6-12 months of *expenses* and keep it liquid, such as in a High Yield Savings Account (HYSA) or Money Market Fund (MMF) 4. Contribute to your 401k up to the company match maximum. 5. Contribute to an HSA if offered up to the maximum allowed. 6. If your 401k plan allows, contribute to a Mega Backdoor Roth. https://thecollegeinvestor.com/17561/understanding-the-mega-backdoor-roth-ira 7. If you do not have access to a Mega Backdoor Roth through your 401k, contribute to a ROTH IRA (unless income ineligible, then use Backdoor Roth IRA method. https://thecollegeinvestor.com/38006/how-to-do-a-backdoor-roth-ira 8. Go back and finish contributing to the 401k plan, up to the maximum limit ($23,000 in 2024). 9. If offered a Company Stock plan (ESPP/ESOP) that gives you shares at a discount, AND you can sell immediately upon stock purchase, contribute the maximum amount to this program and sell each time. You should participate in this regardless of any choices or order of operations above. This runs in parallel to everything else. 10. Open a taxable brokerage account and begin investing here, and/or real estate, and/or side business. 11. Consider funding children's college in 529 plans or taxable brokerage account, or other state advantaged options. 12. Limit the amount of vehicle debt you carry, as vehicles can be one of the biggest barriers to building wealth as people believe they derive "happiness" from getting new vehicles often. Invest all of these in a low fee Total US Equities Market index fund (if offered) or an S&P500 index fund, to start. DONT TOUCH it. Just be steady and don't change, be careful who you listen to, and don't make emotion based moves into cash because what you just "know", likely is not so. Recommended reading: https://www.amazon.com/Simple-Path-Wealth-financial-independence/dp/1533667926 https://www.amazon.com/dp/1119847672?tag=arfcom00-20 https://www.amazon.com/Richest-Man-Babylon-Original-Classics/dp/B0C1J5ML66 https://www.amazon.com/The-Millionaire-Next-Door-audiobook/dp/B0000547HR @falarak Once you have max out 401k in step 8, at what point do you stop putting savings into low risk hysa/mmf at 5.25% and starting putting it into sp500 index funds? For example if looking to buy a $400k to $500k house in near future with $300k in hysa/mmf (would like to keep $50k of $300k as emergency fund), is that enough low risk savings and future savings should be put in more inflation pacing higher risk funds such as sp500 index? |

|

|

|

[#17]

Originally Posted By msprain10: @falarak Once you have max out 401k in step 8, at what point do you stop putting savings into low risk hysa/mmf at 5.25% and starting putting it into sp500 index funds? For example if looking to buy a $400k to $500k house in near future with $300k in hysa/mmf (would like to keep $50k of $300k as emergency fund), is that enough low risk savings and future savings should be put in more inflation pacing higher risk funds such as sp500 index? Originally Posted By msprain10: Originally Posted By FALARAK: 1. Max out your 401k elective deferral contribution. You want to capitalize fully on the match, and the tax advantaged status. Whether you choose Roth 401k or Pre-Tax depends on a LOT of factors. People argue for days over this. Since you have access to a Mega Backdoor Roth to get a LOT of money into Roth status, I personally choose pre-tax for the 401k contribution. You don't have a huge nest egg here in what we are seeing at age 49, and you don't have a LOT of time for tax-free growth. But you DO want a chunk of Roth at retirement to control your taxable income. 2. You didn't mention HSA. If you have a HDHCP then you should max out an HSA, do not spend it, and invest it into market equities. 3. Since you are Mega Backdoor Roth eligible, there is no reason to mess with a direct contribution to a Roth IRA, until you are maxing out the mega backdoor Roth. For instance, the 401k defined contribution limit from all sources is $69,000. If you max your elective deferral of $23,000, then get a company match of $7000, you have $39,000 left to contribute. You can contribute up to $39,000 into the 401k from payroll to AFTER-TAX, which is set to auto-convert to a Roth status sub-account inside the 401k. If you are not filling this bucket, there is no real need to mess with a direct contribution to a Roth IRA (or a Backdoor Roth IRA since you are getting VERY close to the MAGI threshold for direct Roth contributions which currently starts at $230,000 for MFJ.) The mega Backdoor Roth has no income limitations, so take advantage of this while it is available. Congress tries to close this down but has not been successful yet. Once you are filling the Mega-Backdoor ROTH fully, THEN you can consider contributing to a ROTH IRA either directly or backdoor. The exception to this might be your wife's Roth IRA, because funding this doesn't have to come from payroll (assuming you have savings that can contribute to this, and you just want to get more individual retirement funds in her name) 4. In the YEAR you turn 50, you qualify for catchup contributions. So, if you will turn 50 sometime in 2024, you can contribute an additional $7,500 to your 401k, either Pre-Tax or Roth (for now). I choose pre-tax for this. 5. Do the ESPP regardless of anything above, just sell the stock immediately and capture your discount. Free money. And you only tie up 3 months of contributions at a time, which are returned when you sell each quarter. These are my generic Investing order of operations: 1. Pay off all toxic debt (credit cards, high interest rates). 2. NEVER carry a balance on a credit card month to month. This is called "paying the stupid tax". 3. Build an emergency fund of 6-12 months of *expenses* and keep it liquid, such as in a High Yield Savings Account (HYSA) or Money Market Fund (MMF) 4. Contribute to your 401k up to the company match maximum. 5. Contribute to an HSA if offered up to the maximum allowed. 6. If your 401k plan allows, contribute to a Mega Backdoor Roth. https://thecollegeinvestor.com/17561/understanding-the-mega-backdoor-roth-ira 7. If you do not have access to a Mega Backdoor Roth through your 401k, contribute to a ROTH IRA (unless income ineligible, then use Backdoor Roth IRA method. https://thecollegeinvestor.com/38006/how-to-do-a-backdoor-roth-ira 8. Go back and finish contributing to the 401k plan, up to the maximum limit ($23,000 in 2024). 9. If offered a Company Stock plan (ESPP/ESOP) that gives you shares at a discount, AND you can sell immediately upon stock purchase, contribute the maximum amount to this program and sell each time. You should participate in this regardless of any choices or order of operations above. This runs in parallel to everything else. 10. Open a taxable brokerage account and begin investing here, and/or real estate, and/or side business. 11. Consider funding children's college in 529 plans or taxable brokerage account, or other state advantaged options. 12. Limit the amount of vehicle debt you carry, as vehicles can be one of the biggest barriers to building wealth as people believe they derive "happiness" from getting new vehicles often. Invest all of these in a low fee Total US Equities Market index fund (if offered) or an S&P500 index fund, to start. DONT TOUCH it. Just be steady and don't change, be careful who you listen to, and don't make emotion based moves into cash because what you just "know", likely is not so. Recommended reading: https://www.amazon.com/Simple-Path-Wealth-financial-independence/dp/1533667926 https://www.amazon.com/dp/1119847672?tag=arfcom00-20 https://www.amazon.com/Richest-Man-Babylon-Original-Classics/dp/B0C1J5ML66 https://www.amazon.com/The-Millionaire-Next-Door-audiobook/dp/B0000547HR @falarak Once you have max out 401k in step 8, at what point do you stop putting savings into low risk hysa/mmf at 5.25% and starting putting it into sp500 index funds? For example if looking to buy a $400k to $500k house in near future with $300k in hysa/mmf (would like to keep $50k of $300k as emergency fund), is that enough low risk savings and future savings should be put in more inflation pacing higher risk funds such as sp500 index? If you are saving money for a specific purpose and short term time frame, I would leave it in a money market fund than risk it in a market equity fund. A market downturn could last 2-5 years, so if you plan to purchase a home in less than 5 years, I’d rather keep it in cash earning 5% (at least for now) |

|

|

|

|

[#18]

Originally Posted By msprain10: @falarak Once you have max out 401k in step 8, at what point do you stop putting savings into low risk hysa/mmf at 5.25% and starting putting it into sp500 index funds? For example if looking to buy a $400k to $500k house in near future with $300k in hysa/mmf (would like to keep $50k of $300k as emergency fund), is that enough low risk savings and future savings should be put in more inflation pacing higher risk funds such as sp500 index? I'm assuming you are investing in your 401K and not putting retirement funds in a bond/MMF. Anything "short term" should be held in cash, which is any account easily converted to cash such as HYSA or MMF. Do not put your short term cash into the market. While invested you may see some gains over the current MMF rates, but you protect yourself from downsides as well. |

|

|

|

|

[#19]

Originally Posted By FALARAK: This is absolutely not correct. For the Mega Backdoor Roth - After-Tax contributions must be converted to Roth via an In-Plan conversion. At that point, they are Roth status. There is ZERO requirement to move them out of the plan and into a Roth IRA. @falarak You mentioned you can do this in your fidelity 401k - I’ve searched the fidelity app and website and cannot find this. My only options on fidelitys website for contributions are pretax and roth. My 401k is at fidelity - can different 401k plans at fidelity have such different rules? Do I need to look somewhere else for the secret key to this? |

|

|

|

|

[#20]

Originally Posted By Morgan321: @falarak You mentioned you can do this in your fidelity 401k - I’ve searched the fidelity app and website and cannot find this. My only options on fidelitys website for contributions are pretax and roth. My 401k is at fidelity - can different 401k plans at fidelity have such different rules? Do I need to look somewhere else for the secret key to this? Originally Posted By Morgan321: Originally Posted By FALARAK: This is absolutely not correct. For the Mega Backdoor Roth - After-Tax contributions must be converted to Roth via an In-Plan conversion. At that point, they are Roth status. There is ZERO requirement to move them out of the plan and into a Roth IRA. @falarak You mentioned you can do this in your fidelity 401k - I’ve searched the fidelity app and website and cannot find this. My only options on fidelitys website for contributions are pretax and roth. My 401k is at fidelity - can different 401k plans at fidelity have such different rules? Do I need to look somewhere else for the secret key to this? This means your employer plan does not support it. It is by employer plan, not provider. So many plans held at fidelity do not support after tax contributions, because the employer plan does not support them. You can ask your employer to add this capability. |

|

|

|

|

[#21]

Originally Posted By FALARAK: This means your employer plan does not support it. It is by employer plan, not provider. So many plans held at fidelity do not support after tax contributions, because the employer plan does not support them. You can ask your employer to add this capability. Thanks for the info about fidelity! I verified this with HR we can't do it. Apparently adding this capability is in the works because many people have been asking about it. I work for a small company and most employees are well paid so I'm optimistic it will happen in a relatively short time. |

|

|

|

|

[#22]

Originally Posted By Morgan321: Thanks for the info about fidelity! I verified this with HR we can't do it. Apparently adding this capability is in the works because many people have been asking about it. I work for a small company and most employees are well paid so I'm optimistic it will happen in a relatively short time. Originally Posted By Morgan321: Originally Posted By FALARAK: This means your employer plan does not support it. It is by employer plan, not provider. So many plans held at fidelity do not support after tax contributions, because the employer plan does not support them. You can ask your employer to add this capability. Thanks for the info about fidelity! I verified this with HR we can't do it. Apparently adding this capability is in the works because many people have been asking about it. I work for a small company and most employees are well paid so I'm optimistic it will happen in a relatively short time. When it is supported, you will see two things: 1. AFTER-TAX contribution category. 2. Auto-conversion option to automatically execute the in-plan conversion of the After-Tax contribution to Roth status, immediately upon contribution.

|

|

|

|

|

[#23]

Originally Posted By Morgan321: Thanks for the info about fidelity! I verified this with HR we can't do it. Apparently adding this capability is in the works because many people have been asking about it. I work for a small company and most employees are well paid so I'm optimistic it will happen in a relatively short time. I believe it is a requirement after Secure 2.0 was passed but they have an extended amount of time to change their plan policies. |

|

|

|

|

[#24]

Originally Posted By Silverbulletz06: I believe it is a requirement after Secure 2.0 was passed but they have an extended amount of time to change their plan policies. Originally Posted By Silverbulletz06: Originally Posted By Morgan321: Thanks for the info about fidelity! I verified this with HR we can't do it. Apparently adding this capability is in the works because many people have been asking about it. I work for a small company and most employees are well paid so I'm optimistic it will happen in a relatively short time. I believe it is a requirement after Secure 2.0 was passed but they have an extended amount of time to change their plan policies. Roth *contribution* capability is a requirement of Secure 2.0 because the age 50+ catchup contribution must be Roth and not pre-tax. However, After-Tax with Roth in-plan conversion is not a requirement of Secure Act 2.0. In fact, congress has been attempting to eliminate the Mega Backdoor Roth option, or at least limit it by income the same as a direct Roth IRA contribution is limited. |

|

|

|

Win a FREE Membership!

Win a FREE Membership!

Sign up for the ARFCOM weekly newsletter and be entered to win a free ARFCOM membership. One new winner* is announced every week!

You will receive an email every Friday morning featuring the latest chatter from the hottest topics, breaking news surrounding legislation, as well as exclusive deals only available to ARFCOM email subscribers.

AR15.COM is the world's largest firearm community and is a gathering place for firearm enthusiasts of all types.

From hunters and military members, to competition shooters and general firearm enthusiasts, we welcome anyone who values and respects the way of the firearm.

Subscribe to our monthly Newsletter to receive firearm news, product discounts from your favorite Industry Partners, and more.

Copyright © 1996-2024 AR15.COM LLC. All Rights Reserved.

Any use of this content without express written consent is prohibited.

AR15.Com reserves the right to overwrite or replace any affiliate, commercial, or monetizable links, posted by users, with our own.