[ARCHIVED THREAD] - Retirement (Page 1 of 2)

Posted: 10/16/2016 2:32:37 AM EDT

|

I'm 28 years old(or 27, honestly can't recall at the moment, pretty sure it's 28 though). Just started an apprenticeship so I won't be able to invest balls deep for a couple of years yet. Around here if you work year round you get 74,000 in take home pay minus taxes. Total package is about 104,000/year.

Being that I won't be investing too heavily into retirement until I'm at least 30, how much should I be putting away a year? I'm behind the eight ball here starting any serious investing so late but I'm still shooting to retire between 55 and 60. Part of my benefits package inclused a 401k and roth IRA. I cannot pay additional into those though but there is also a third optional annuity that I can pay into. I'm looking at investing between 10-15k a year into retirement. Does that sound about right in my given situation if I'm shooting to retire, ideally, by 55? |

| Those various investment companies that manage the plans for your company, should send you information on the plans and also will have investment advisers who can talk with you and set up a plan for you to attain your goals in the time frame, they will also show you what has to be done to attain the goal. |

|

These days I think it's hard for anyone to tell you how much will be enough to retire by 55.

There are plenty of online calculators, for you to play with that deal with retirement. What do you mean by "Part of my benefits package inclused a 401k and roth IRA. I cannot pay additional into those though but there is also a third optional annuity that I can pay into". Are you saying you've maxed out your 401k contributions already ? At a minimum you should be putting enough away to get the company match. In any case, advice from an older guy. Live as far below your means as possible, don't get into debt for stupid shit, and save as much money as possible. |

| Correction.. the employer will not match anything we pay into the 401k or Roth. THEY pay in to them as part of our contract. We can pay into them on the side but, from my understanding, that is a waste as they will match the annuity up to a certain amount(don't have those numbers on hand at the moment). |

|

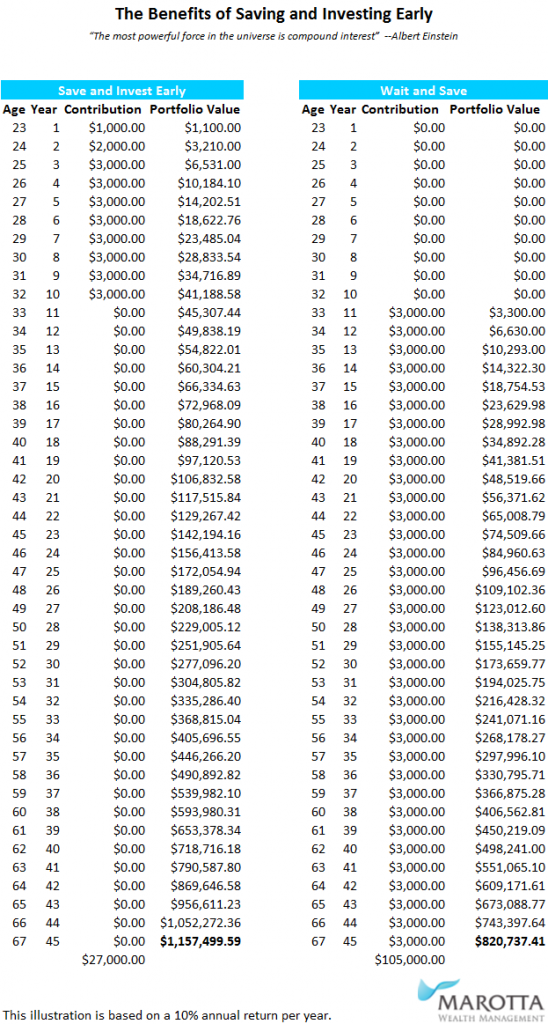

you're not going to retire at 55. For some quick math, we'll assume that you want to make in retirement approximately what you are making now. We'll also assume you can average a 6% return on your money for the next 28 years.

Under these assumptions, you would have to invest $27,000 per year at 6% to have $1,850,000 at 55. Under the 4% rule, you can pull $74,000 per year for the rest of your life. |

| You really can't save too much. Time in the market is more important than how much you dump in it. As such, I would recommend that you save the absolute most you are comfortable with, starting yesterday. As a random baseline, I make a bit more in salary than your total projected compensation and I save around $1500/mo and have been feeling guilty for it being so little. |

|

Quoted:

Fuck an annuity - pay into direct retirement accounts only. In the modern economy, annuities are nice investment vehicles for the bankers/sellers, and not much anyone else. But if the company is matching? He's giving away free money. Up to what is being matched, but not a dollar more, I'd say. |

|

Quoted: I'm 28 years old(or 27, honestly can't recall at the moment, pretty sure it's 28 though). Just started an apprenticeship so I won't be able to invest balls deep for a couple of years yet. Around here if you work year round you get 74,000 in take home pay minus taxes. Total package is about 104,000/year. Being that I won't be investing too heavily into retirement until I'm at least 30, how much should I be putting away a year? I'm behind the eight ball here starting any serious investing so late but I'm still shooting to retire between 55 and 60. Part of my benefits package inclused a 401k and roth IRA. I cannot pay additional into those though but there is also a third optional annuity that I can pay into. I'm looking at investing between 10-15k a year into retirement. Does that sound about right in my given situation if I'm shooting to retire, ideally, by 55? $10-15k per year sounds about right. If you don't have a company pension, fund your retirement in this order. 1. 401k 2. Traditional IRA 3. Roth IRA If you have a company pension, fund the Roth before the Traditional IRA. The Roth will be better because the pension will push you up into a higher tax bracket. Put it in a low-fee mutual fund like Vanguard. Don't let a "financial planner" talk you into some oddball fund that pays the "planner" high fees. Good luck! |

|

Here ya go! Twelve bucks for a year, best investment you'll ever make.

Worked for me. Retired early and comfortably by following their advice. |

| Put away as much as you can afford. Told my daughter this when she started working, and she followed our advice. Ever since then she has put as much as law allows into her retirement fund. She is now very pleased at the result, and plans on an early retirement. |

|

I was a fool living for today and didn't think saving for retirement was important. I didn't wake up and realize I needed to start saving for retirement until I was 40. Since then I have been contributing the max. allowed, but it's not ever going to be enough. Don't be like me, young people at your age should put away as much as is practical. The benefits of doing so are so much better.

Participate in 401k whenever possible to get the employer match. IRA's and Roth IRA's are good for those not employed where 401k is available. Stay away from annuities, they are for suckers. The bankers get rich off of your money there. A traditional savings account for a rainy day fund is also a good idea. Good luck to you and have a great future with proper planning. |

|

Quoted:

In any case, advice from an older guy. Live as far below your means as possible, don't get into debt for stupid shit, and save as much money as possible. This, the Government is going to tax this everloving shit out of your productivity. I hate it for my children. |

| The book mentioned earlier Rich Dad Poor Dad I believe does a good job explaining time value of money. I started at 27 which is right on the cusp of not having to put away crazy money each year, so you will be glad you started now. I plan to retire in 4-5 years at 57 and if projections hold I will have $1Mil in the 401K. |

|

Quoted:

Put away as much as you can afford. Told my daughter this when she started working, and she followed our advice. Ever since then she has put as much as law allows into her retirement fund. She is now very pleased at the result, and plans on an early retirement. My dad told me the same when I started working, I'm glad I listened. |

| Biggest financial mistake I made was at about 28 or so - sold out of all of my retirement stuff for a down payment on a house, which I later almost lost my shirt on selling in 2008. Would have been much batter off renting the whole time, in retrospect. But, timing can suck sometimes. |

|

Quoted:

Biggest financial mistake I made was at about 28 or so - sold out of all of my retirement stuff for a down payment on a house, which I later almost lost my shirt on selling in 2008. Would have been much batter off renting the whole time, in retrospect. But, timing can suck sometimes. It could be worse, I have a friend who did the same in his late 30s. |

|

Quoted:

save a quarter. even then, people try to DIY their financial planning. bad juju. paying someone 1% to dot all the "I"s and cross all the "t"s is cheap money for peace of mind. or ask arfcom GD. They are all professional finance people. +1 on the professionally managed portfolio. |

|

Quoted:

+1 on the professionally managed portfolio. Quoted:

Quoted:

save a quarter. even then, people try to DIY their financial planning. bad juju. paying someone 1% to dot all the "I"s and cross all the "t"s is cheap money for peace of mind. or ask arfcom GD. They are all professional finance people. +1 on the professionally managed portfolio. Yep. Full disclosure, I'm in the business. Find a CFP to help you. Ask people you know for referrals, make sure they have legitimate designations. Interview at least 2, then pick your favorite. By hiring someone, you are at least taking your emotions out of the equation. Also, while your own research is helpful, it would be insanely hard to understand finances like a true professional does. |

|

Quoted:By hiring someone, you are at least taking your emotions out of the equation. Also, while your own research is helpful, it would be insanely hard to understand finances like a true professional does. Not to belabor the point, but it probably helps individual investors to know that there are two major kinds of clients: institutional and retail. Retail is the individual investors, and they don't get access to institutional (meant for corporations) research, materials, strategies, or advice. Professional advisors with the correct licenses are allowed to get this info. The professional advisor can then translate into English for the individual investor. It's not that large corporations get secret squirrel stuff, it's that the information would be inappropriate for an individual investor; it's not called "professional" for nothing. Just a tidbit for people who try to manage their own stuff. It's possible, but missing a large part of the puzzle, and to be weighted against getting it wrong and retirement not working out the way they thought it would. |

|

Quoted:

Yep. Full disclosure, I'm in the business. Find a CFP to help you. Ask people you know for referrals, make sure they have legitimate designations. Interview at least 2, then pick your favorite. By hiring someone, you are at least taking your emotions out of the equation. Also, while your own research is helpful, it would be insanely hard to understand finances like a true professional does. Quoted:

Quoted:

Quoted:

save a quarter. even then, people try to DIY their financial planning. bad juju. paying someone 1% to dot all the "I"s and cross all the "t"s is cheap money for peace of mind. or ask arfcom GD. They are all professional finance people. +1 on the professionally managed portfolio. Yep. Full disclosure, I'm in the business. Find a CFP to help you. Ask people you know for referrals, make sure they have legitimate designations. Interview at least 2, then pick your favorite. By hiring someone, you are at least taking your emotions out of the equation. Also, while your own research is helpful, it would be insanely hard to understand finances like a true professional does. And they'll be aware of different strategies you can use in different situations. We had a big expensive house that lost a shit ton of value in the housing crash. We were going to just sell it and eat the loss. Our guy hooked us up with an accountant to essentially convert it into a business, show rental income in 3 different tax years before we sold it, then we were able to write off a bunch of depreciation and stuff and stuff that GREATLY lessened the sting. That's just an example of shit they may know that can help you. Running your own Vanguard IRA might save you a nickel, but that one little nugget of info saved us more than we'll ever end up paying out to him. |

|

Quoted:

And they'll be aware of different strategies you can use in different situations. We had a big expensive house that lost a shit ton of value in the housing crash. We were going to just sell it and eat the loss. Our guy hooked us up with an accountant to essentially convert it into a business, show rental income in 3 different tax years before we sold it, then we were able to write off a bunch of depreciation and stuff and stuff that GREATLY lessened the sting. That's just an example of shit they may know that can help you. Running your own Vanguard IRA might save you a nickel, but that one little nugget of info saved us more than we'll ever end up paying out to him. Quoted:

Quoted:

Quoted:

Quoted:

save a quarter. even then, people try to DIY their financial planning. bad juju. paying someone 1% to dot all the "I"s and cross all the "t"s is cheap money for peace of mind. or ask arfcom GD. They are all professional finance people. +1 on the professionally managed portfolio. Yep. Full disclosure, I'm in the business. Find a CFP to help you. Ask people you know for referrals, make sure they have legitimate designations. Interview at least 2, then pick your favorite. By hiring someone, you are at least taking your emotions out of the equation. Also, while your own research is helpful, it would be insanely hard to understand finances like a true professional does. And they'll be aware of different strategies you can use in different situations. We had a big expensive house that lost a shit ton of value in the housing crash. We were going to just sell it and eat the loss. Our guy hooked us up with an accountant to essentially convert it into a business, show rental income in 3 different tax years before we sold it, then we were able to write off a bunch of depreciation and stuff and stuff that GREATLY lessened the sting. That's just an example of shit they may know that can help you. Running your own Vanguard IRA might save you a nickel, but that one little nugget of info saved us more than we'll ever end up paying out to him. Nice. Was he a CFP, had a other designations, or no designations? Just curious. |

|

Quoted:

Nice. Was he a CFP, had a other designations, or no designations? Just curious. Quoted:

Quoted:

Quoted:

Quoted:

Quoted:

save a quarter. even then, people try to DIY their financial planning. bad juju. paying someone 1% to dot all the "I"s and cross all the "t"s is cheap money for peace of mind. or ask arfcom GD. They are all professional finance people. +1 on the professionally managed portfolio. Yep. Full disclosure, I'm in the business. Find a CFP to help you. Ask people you know for referrals, make sure they have legitimate designations. Interview at least 2, then pick your favorite. By hiring someone, you are at least taking your emotions out of the equation. Also, while your own research is helpful, it would be insanely hard to understand finances like a true professional does. And they'll be aware of different strategies you can use in different situations. We had a big expensive house that lost a shit ton of value in the housing crash. We were going to just sell it and eat the loss. Our guy hooked us up with an accountant to essentially convert it into a business, show rental income in 3 different tax years before we sold it, then we were able to write off a bunch of depreciation and stuff and stuff that GREATLY lessened the sting. That's just an example of shit they may know that can help you. Running your own Vanguard IRA might save you a nickel, but that one little nugget of info saved us more than we'll ever end up paying out to him. Nice. Was he a CFP, had a other designations, or no designations? Just curious. I'd have to look at one of his cards when I get home to know exactly what he's got. My wife is an actuary and handled all the initial vetting. |

|

Look into a self-directed IRA. At least you get more control of your stuff and lest you forget, MF-Global and PFG-Best (both absconded with clients' funds).

What's the difference between money and currency? If you don't know, get a financial education and watch Mike Maloney's Hidden Secrets of Money. It's a free education that takes only your time and attention. Good luck and prosper. We are on the brink of a global economic reset with the most massive wealth transfer in the history of mankind. Those who are liquid can become enormously wealthy. |

|

Quoted:

you're not going to retire at 55. For some quick math, we'll assume that you want to make in retirement approximately what you are making now. We'll also assume you can average a 6% return on your money for the next 28 years. Under these assumptions, you would have to invest $27,000 per year at 6% to have $1,850,000 at 55. Under the 4% rule, you can pull $74,000 per year for the rest of your life. Not in this current environment. Most trusts and other investors are in trouble because of low current returns. 2-3% for the next few years will probably be the norm. |

|

Quoted:

Not in this current environment. Most trusts and other investors are in trouble because of low current returns. 2-3% for the next few years will probably be the norm. Quoted:

Quoted:

you're not going to retire at 55. For some quick math, we'll assume that you want to make in retirement approximately what you are making now. We'll also assume you can average a 6% return on your money for the next 28 years. Under these assumptions, you would have to invest $27,000 per year at 6% to have $1,850,000 at 55. Under the 4% rule, you can pull $74,000 per year for the rest of your life. Not in this current environment. Most trusts and other investors are in trouble because of low current returns. 2-3% for the next few years will probably be the norm. Based on what? |

|

Your income is high (to me anyway) but, you really didn't say much. So, just go over these points.....

Max out 401k? Max out Roth Contribution? Health Savings Account? Did you buy insurance to take care of the family (if you have one) you leave behind or just to guarantee insurability? 6-12 month cash on hand? Home/rent/house? Pay it all off? Car Payments? Pay it all off? Reg. monthly bill and debt payments? College debts? Have you prepped for the ___________? Assuming that you won't be going wild in retirement, if it's possible, 10-12% into a retirement fund/account sounds conservative. If you put in more when you're young......you'll have more time to skate a bit later (if things go wrong). Aloha, Mark |

|

I have been managing my own stuff for years

Benn buying individual stocks and mutual funds and you don't need to pay anyone to do this For example I used to work at Exxon in the early 80s. Left with 4K worth or stock. Re-nvested every dividend and bought more along the way now have 2500 shares worth about 220k now and that's 1 stock - the dividends alone will pay my property taxes, homeowner ins and auto ins I have created my own annuity thru dividends |

|

I'm an outlier here. 401Ks are a scam imo. YOUR money is on lockdown and you have to pay a penalty if you have an emergency and need to withdraw early or borrow against it. When you look at all the estimates for retirement, they are always based off assumptions...it is not realistic to assume 6%, 8%, 10%, etc, returns per year for 30+ years. Nothing goes straight up. Are you aware of ALL the fees associated with the plans available?

60 Minutes on 401Ks We all know Social Security will fail. What do you think Congress will do? Don't worry, they'll have a plan for your 401K: Testimony Congress Should Nationalize 401Ks ETA: Don't forget to subtract out those maintenance fees from the annual returns. You may need a 13% return or more to get a net 10%. ETA2: She wants to nationalize 401Ks |

|

If you use TurboTax, get your last year's version and run through the what-ifs based on 401K contributions. See how your final number is impacted. If you don't have it, blow $40 and get next years, or find someone who will give you last years disk. At 100K you are making enough that you should minimize that amount that goes to Federal tax. That would be by contributing 18K/year to a 401K. You lose 10% by pulling it out early, plus the tax on the money. The tax you would have had to pay in any case. |

|

Quoted:

Find a certified financial planner. Tell him your birthday and ask him how old you are. If he can tell you, he is smarter than you and can be trusted. Good advice here. If you're too stupid to figure out your age you may want to hire someone to do the heavy thinking for you. |

|

My wife started with HCA 35 years ago as a young RN. She always contributed 10% and was matched. We added up our assets last week. Not counting equity in our home, firearms, etc, we have seven figures. When she hits 59.5, she begins to pull from her 401k. I turn 62 in less than 13 months. I will most likely retire then. We are semi-retired right now.

Point being, do not delay savings. No matter whatever else is going on, save. Do not use new furniture, a vacation, etc as reasons to start later. As is, we can pretty well do whatever we want as long as our health holds out. That is the scary part. Giv en what is happening with health care, we may end up spending a quarter of a mil on insurance once she retires over ten years. |

|

Quoted:

I couldn't imagine working until 65. I couldn't imagine working until 65.Quoted:

Quoted:

I personally think early retirement is overrated (depending on what you do for a living of course). I would do as much as you can and extend your window to age 65. The difference will be astronomical. I couldn't imagine working until 65.I'll tell you my expetience.....people who work after retiring are the happiest. Now, there are some commonalities with the ones I am talking about... They don't need to work to live. They work part time. They do something they love doing. I plan to retire earlier than 65, but will work for years after that. |