[ARCHIVED THREAD] - A Honest question (Page 1 of 2)

Posted: 12/16/2013 2:23:56 PM EDT

| I prep a little here and there. Nothing like the doomsday preppers. But what is the likely that something will actually happen. I keep reading civil unrest, government complete takeover, nuclear war, and what ever else anyone can think of. Oh zombies. But the economy is tanking and it has for years and no SHTF. I would like someone to try to explain it to me. Please. I am just not that informed I guess. |

|

Quoted:

I prep a little here and there. Nothing like the doomsday preppers. But what is the likely that something will actually happen. I keep reading civil unrest, government complete takeover, nuclear war, and what ever else anyone can think of. Oh zombies. But the economy is tanking and it has for years and no SHTF. I would like someone to try to explain it to me. Please. I am just not that informed I guess. As for the economy, in short, because it's happened elsewhere multiple times throughout history....AND....our country's economy is sort of following suit with those places. But if you look at what takes place it leads to some unpleasant results. Prepare now, hopefully survive later. Don't prepare and you take your chances just like everyone else. -Emt1581 |

| Zombies are used as a metaphor of sorts. If youre prepped for zombies, youre prepped for any SHTF scenario. I agree with the above posters that its better to have it and not need it, than need it and not have it. And no one can perfectly predict these coming scenarios. Even a little bit helps. So just keep doing what youre doing. |

|

Well, if you aren't scared about our economy (and that of the world, for that matter), then you haven't been paying close enough attention Look at the Weimar Republic. Look what happens and has always happened when a country does what we are doing. NEVER has ended well. Civil unrest: It would take a surprisingly small even to cause a LOT of chaos. Doesn't have to be a national event to be a SHTF for you, locally. Gov't takeover: Really? You don't see this as possible the way the gov't is acting? Our civilization and relatively calm time in the world is hanging by a thread, and historically speaking, we are probably due for something bad. I pray every day I never have to use my preps. BUT, if the day comes I will be DAMN GLAD that I have what I do.

|

|

Something will happen someday, for sure.....in your area of operation and in your lifetime? Who knows.

My view is that I can afford to have some things to provide comfort to my family during hard times that we are likely to encounter.........bad weather, job loss, other natural disaster......We prep what we use....so in the end, if nothing ever happens. Nothing or little is wasted and my heirs will clean out my house and proclaim that I really was senile based on the stash. I am embarrassed for folks in our community that have cashed out retirement.....gone into debt.....and gone overboard to prep for zombies or whatever. Prepping is not going into debt to stock up on PMAGs and Black Friday uppers (nice excuse though)..... NOW, they may be right and it will all go down tomorrow, but we have a pretty good record of being lucky in recent history. Being prepped also means that you will be in good shape even if it doesn't hit the fan. |

|

Prepping is just like an insurance policy. You hope you don't need it, but if you do, it sure is nice. A great hobby too! Like the insurance policy, how much you put into it, usually reflects as to how good a policy you have. It gets really good when you work on not wasting anything by rotating food stocks and other items into your everyday stuff and not having to throw the older stuff away (a waste in the end like insurance premiums)

It can be fun, and fulfilling to know you have things pretty much covered. I agree, we are in for tough times somewhere not too far down the road. Why not be ready? |

|

First, you should separate the what you think from what you know. Well, we know that the economy is not what the MSM blowhard cheerleaders make it out to be. There are 48 million people on food stamps, nearly double the number when OcommiePinko took office. We know that the current unemployment rate does not consider people who have been out of work so long that they've fallen off the gravy train - we know there are several million of these folks based on the employment participation rate being as low now as it was in the early 80s (after Jimmy Carter nearly destroyed the economy). We know that the top banks have more bogus, fake, so-called derivatives now than when the financial crisis started in 2008. We know that the amount of "excess reserves", ie money that banks have on deposit with the Federal Reserve ostensibly because they need to show they can cover losses elsewhere, skyrocketed from 108 billion to 1.08 TRILLION, a factor of 10. Oh, and much of that money was "given" to the banks by the bailout. We know there are currently about 1/6th the number of workers employed in the housing industry as there were in 2006-2007. (So, if you were in that industry, chances are good you're not anymore and won't be for the foreseeable future.) We know that there are already millions of folks whose insurance is being cancelled and will have a huge increase in their costs, and the same will occur again in spades come January. We know that the Administration is hell-bent on gun control, spying on its own citizens, and plans to implement tens of thousands of pages of new regulations within the next year (along with the tens of thousands of pages every year for the last 5). We know that our money is being de-based by roughly 6% per year by the 85 large the Federal Reserve is printing into existence. That's on top of the inflation in food, energy, and other necessities, which are excluded from the .gov's "official" inflation tally. We know that the number of guns and the amount of ammo being purchased this year alone will be double what it was a mere 10 years ago. We know that trust in the .gov, and vice versa, is at its lowest point in American history. We know there were large crowds of people, angry at the petty, stupid things Odumbo demanded as part of the shutdown, who were willing and able to defy government proclamations and visit the people's memorials.

By what definition can we legitimately say that the S hasn't already HTF? For a great, great many people, it already has. Further, in terms of the country's financial condition, it hit the fan 5 years ago and has not improved one iota. In fact, our national debt is so high now that a simple reversion to mean historical interest rates would bankrupt the US government because interest on the debt by itself would exceed all revenues from all sources. If, on the other hand you're definition of SHTF is wholesale gunfights between angry citizens and .gov JBTs, then, no, SHTF has yet to begin. As for an "advertised" financial meltdown, we haven't been allowed to see the meltdown that has already occurred because of the incessant pandering of the left-leaning media to its Ocommie master. When, not if, there is another financial crisis like what happened in 2008 happens again, it will be a systemic collapse because there is no headroom left in the economy to absorb the catastrophic losses that would occur. Bank runs and subsequent "holidays" along with capital controls to prevent people from getting their money out of insolvent institutions would occur. How likely is the "worst case" scenario? At this point, 50/50 between now and the end of Odumbo's term. How likely is a real shooting war vs. massive protests and civil unrest? Not very likely, I think. First, the mostly silent majority of people will finally have enough and show up in sufficient numbers to nationwide protests to get the pols attention. Further, the .gov knows it is completely outgunned by sheer numbers, and the .mil will support the Constitution, not the Administration, when push comes to shove. So, this is a long-winded post to basically say there is a "high" likelihood of economic turmoil ala greater than the Great Depression. If you plan to become self-sufficient, financially first, then actually, then regardless of the debilitating financial condition of the rest of the country, you and your family will be safe, fed, clothed, sheltered, and perhaps even prosperous, just as those who lived before us were back then. My $0.031 (after Fed induced inflation is considered). |

|

Quoted:

First, you should separate the what you think from what you know. Well, we know that the economy is not what the MSM blowhard cheerleaders make it out to be. There are 48 million people on food stamps, nearly double the number when OcommiePinko took office. We know that the current unemployment rate does not consider people who have been out of work so long that they've fallen off the gravy train - we know there are several million of these folks based on the employment participation rate being as low now as it was in the early 80s (after Jimmy Carter nearly destroyed the economy). We know that the top banks have more bogus, fake, so-called derivatives now than when the financial crisis started in 2008. We know that the amount of "excess reserves", ie money that banks have on deposit with the Federal Reserve ostensibly because they need to show they can cover losses elsewhere, skyrocketed from 108 billion to 1.08 TRILLION, a factor of 10. Oh, and much of that money was "given" to the banks by the bailout. We know there are currently about 1/6th the number of workers employed in the housing industry as there were in 2006-2007. (So, if you were in that industry, chances are good you're not anymore and won't be for the foreseeable future.) We know that there are already millions of folks whose insurance is being cancelled and will have a huge increase in their costs, and the same will occur again in spades come January. We know that the Administration is hell-bent on gun control, spying on its own citizens, and plans to implement tens of thousands of pages of new regulations within the next year (along with the tens of thousands of pages every year for the last 5). We know that our money is being de-based by roughly 6% per year by the 85 large the Federal Reserve is printing into existence. That's on top of the inflation in food, energy, and other necessities, which are excluded from the .gov's "official" inflation tally. We know that the number of guns and the amount of ammo being purchased this year alone will be double what it was a mere 10 years ago. We know that trust in the .gov, and vice versa, is at its lowest point in American history. We know there were large crowds of people, angry at the petty, stupid things Odumbo demanded as part of the shutdown, who were willing and able to defy government proclamations and visit the people's memorials. By what definition can we legitimately say that the S hasn't already HTF? For a great, great many people, it already has. Further, in terms of the country's financial condition, it hit the fan 5 years ago and has not improved one iota. In fact, our national debt is so high now that a simple reversion to mean historical interest rates would bankrupt the US government because interest on the debt by itself would exceed all revenues from all sources. If, on the other hand you're definition of SHTF is wholesale gunfights between angry citizens and .gov JBTs, then, no, SHTF has yet to begin. As for an "advertised" financial meltdown, we haven't been allowed to see the meltdown that has already occurred because of the incessant pandering of the left-leaning media to its Ocommie master. When, not if, there is another financial crisis like what happened in 2008 happens again, it will be a systemic collapse because there is no headroom left in the economy to absorb the catastrophic losses that would occur. Bank runs and subsequent "holidays" along with capital controls to prevent people from getting their money out of insolvent institutions would occur. How likely is the "worst case" scenario? At this point, 50/50 between now and the end of Odumbo's term. How likely is a real shooting war vs. massive protests and civil unrest? Not very likely, I think. First, the mostly silent majority of people will finally have enough and show up in sufficient numbers to nationwide protests to get the pols attention. Further, the .gov knows it is completely outgunned by sheer numbers, and the .mil will support the Constitution, not the Administration, when push comes to shove. So, this is a long-winded post to basically say there is a "high" likelihood of economic turmoil ala greater than the Great Depression. If you plan to become self-sufficient, financially first, then actually, then regardless of the debilitating financial condition of the rest of the country, you and your family will be safe, fed, clothed, sheltered, and perhaps even prosperous, just as those who lived before us were back then. My $0.031 (after Fed induced inflation is considered).

|

|

I am prepping for a hurricane. But that is not all, it is simply the most likely event. Is it likely? No, but then neither is me getting mugged or my home being broken into, and I am prepared for that. It is not likely that my house will catch on fire, but I have fire extinguishers. It is not likely that I will get seriously ill, but I have health insurance (for as long as that lasts these days). It is not likely my home will get flooded, but I have flood insurance. It is all the same thing in my mind. |

|

Quoted:

You don't need an epic event for it to be a SHTF scenario. Worry about things that happen on a regular basis and prepare for them before you worry about EMP or aliens attacking. Tornado Hurricane Ice Storm Blizzard Loss of spouse - death or divorce Loss of Job Loss of ability to make a living I am amazed at how many people claim to be prepping but do not have basic insurance coverage. That would be where you should start. health insurance life insurance disability insurance car insurance HO or renters insurance It is impossible for you as an individual to adequately prep for the kind of SHTF events these insurance policies cover but you can readily buy a policy, yet many people refuse to do so. |

|

End Of The World As We Know It, EOTWAKI, is a matter of threshold, because everyday really is an end and a new beginning. Its a lot more fun to talk and think of shooting wars. After all, this a gun forum. Will it happen? I have little doubt because socialism is a failed experiment that historically ends in civil unrest or war. The question is when? Its taking a lot to drag down the best economy and standard of living the world has ever seen. We're heading there though as this is the third generation now that has no expectation of living better than their parents. To us older folks, it wasn't that long ago "Leave it to Beaver" was on TV and mom stayed home. We're not that far either from that house with the picket fence being a slum condo in the tower like in the movie "Dredd".

Until then, the difference between someone who dabbles at this lifestyle and those who live it is in the preparation of everything up until that point. We have a lot to go through before the UN Invades or revolution reigns. Since I left my parents over 40 years ago, I've experienced two over one week events that included a total loss of services. I've seen one riot first hand and avoided about three others. My house has been broken in on, my vehicle stolen, and at least six attempts on my life, not including childhood fights, by someone I didn't even know pointing guns at me. Rather than face unemployment, I've lived in seven states. Making a decision, which I have, of I'm staying here is a big decision. I've been stranded in snow storms, stranded in the wilderness, prayed on jets to let me survive this one, and so sick on the Ocean, I was too sick to be scared out of my wits. I've had friends raped and killed. Stood guard and helped people pickup the pieces of their lives. All of this was after going to war with the Military. In retrospect, Army life was more intense in a short time period but nothing compared to a lifetime. Its pretty simple, we prepare because shit is not maybe but going to happen. We prepare because others depend on us and when shit happens that deer in the headlight look is not acceptable. Its about taking responsibility. Tj |

|

Quoted:

Quoted:

Quoted:

First, you should separate the what you think from what you know. Well, we know that the economy is not what the MSM blowhard cheerleaders make it out to be. There are 48 million people on food stamps, nearly double the number when OcommiePinko took office. We know that the current unemployment rate does not consider people who have been out of work so long that they've fallen off the gravy train - we know there are several million of these folks based on the employment participation rate being as low now as it was in the early 80s (after Jimmy Carter nearly destroyed the economy). We know that the top banks have more bogus, fake, so-called derivatives now than when the financial crisis started in 2008. We know that the amount of "excess reserves", ie money that banks have on deposit with the Federal Reserve ostensibly because they need to show they can cover losses elsewhere, skyrocketed from 108 billion to 1.08 TRILLION, a factor of 10. Oh, and much of that money was "given" to the banks by the bailout. We know there are currently about 1/6th the number of workers employed in the housing industry as there were in 2006-2007. (So, if you were in that industry, chances are good you're not anymore and won't be for the foreseeable future.) We know that there are already millions of folks whose insurance is being cancelled and will have a huge increase in their costs, and the same will occur again in spades come January. We know that the Administration is hell-bent on gun control, spying on its own citizens, and plans to implement tens of thousands of pages of new regulations within the next year (along with the tens of thousands of pages every year for the last 5). We know that our money is being de-based by roughly 6% per year by the 85 large the Federal Reserve is printing into existence. That's on top of the inflation in food, energy, and other necessities, which are excluded from the .gov's "official" inflation tally. We know that the number of guns and the amount of ammo being purchased this year alone will be double what it was a mere 10 years ago. We know that trust in the .gov, and vice versa, is at its lowest point in American history. We know there were large crowds of people, angry at the petty, stupid things Odumbo demanded as part of the shutdown, who were willing and able to defy government proclamations and visit the people's memorials. By what definition can we legitimately say that the S hasn't already HTF? For a great, great many people, it already has. Further, in terms of the country's financial condition, it hit the fan 5 years ago and has not improved one iota. In fact, our national debt is so high now that a simple reversion to mean historical interest rates would bankrupt the US government because interest on the debt by itself would exceed all revenues from all sources. If, on the other hand you're definition of SHTF is wholesale gunfights between angry citizens and .gov JBTs, then, no, SHTF has yet to begin. As for an "advertised" financial meltdown, we haven't been allowed to see the meltdown that has already occurred because of the incessant pandering of the left-leaning media to its Ocommie master. When, not if, there is another financial crisis like what happened in 2008 happens again, it will be a systemic collapse because there is no headroom left in the economy to absorb the catastrophic losses that would occur. Bank runs and subsequent "holidays" along with capital controls to prevent people from getting their money out of insolvent institutions would occur. How likely is the "worst case" scenario? At this point, 50/50 between now and the end of Odumbo's term. How likely is a real shooting war vs. massive protests and civil unrest? Not very likely, I think. First, the mostly silent majority of people will finally have enough and show up in sufficient numbers to nationwide protests to get the pols attention. Further, the .gov knows it is completely outgunned by sheer numbers, and the .mil will support the Constitution, not the Administration, when push comes to shove. So, this is a long-winded post to basically say there is a "high" likelihood of economic turmoil ala greater than the Great Depression. If you plan to become self-sufficient, financially first, then actually, then regardless of the debilitating financial condition of the rest of the country, you and your family will be safe, fed, clothed, sheltered, and perhaps even prosperous, just as those who lived before us were back then. My $0.031 (after Fed induced inflation is considered). Planemaker, way to lay out facts and make the holidays brighter. Unfortunately, while I agree with your post, I cannot toast to it. |

|

Quoted:

Snip Jedi, have you got any investing advice you'd be willing to share here? Not on specific investments, of course, but on basic strategy. (Read: You're beating our retirement accounts' return right now and I'm jealous.) For those who aren't investing, consider this: with a high degree of certainty, everyone here is going to face financial trouble at some time. Ultimately, many of us will have to stop working or slow down significantly in our older years. Start saving for retirement when you are young. Start as early as possible. Allow the power of compounding interest to work for you. Delaying the start of your retirement savings by even a few years can have a big effect on how much interest you earn. Here is a quick look at the sort of difference delaying your retirement savings can make. This assumes an 8% return every year, $5,000 saved every year, and all deposits made as a lump sum at the end of the year. Ignore the principal difference (that is, the amount that is deposited) and pay attention to the difference in the interest accrued:

|

|

I didn't realize 3/4 of the people on Doomsday preppers were actually preparing.... More like hoarding with a kinda sorta maybe purpose....

Definitely most are not preparing in the real sense of the term. Missing the bigger points while obsessing about the smaller points IMO. FWIW, I'm only up to Season 2 on DVD but so far the only decent examples have been SouthernPrepper1, Scott Hunt and a handful of others. |

|

Quoted:

Jedi, have you got any investing advice you'd be willing to share here? Not on specific investments, of course, but on basic strategy. (Read: You're beating our retirement accounts' return right now and I'm jealous.) For those who aren't investing, consider this: with a high degree of certainty, everyone here is going to face financial trouble at some time. Ultimately, many of us will have to stop working or slow down significantly in our older years. Start saving for retirement when you are young. Start as early as possible. Allow the power of compounding interest to work for you. Delaying the start of your retirement savings by even a few years can have a big effect on how much interest you earn. I can't speak for ar-jedi, but my super secret strategy is to put money into my 401K at work each payday, which is invested in the stock market. ROR last 12 months: 24.4%

but, this is just between us, OK? shhhhhhhh ETA: OTOH, I don't wanna look at what is was December 2008. |

|

Quoted: I can't speak for ar-jedi, but my super secret strategy is to put money into my 401K at work each payday, which is invested in the stock market. ROR last 12 months: 24.4% http://imageshack.us/a/img29/5383/9qxr.jpg but, this is just between us, OK? shhhhhhhh ETA: OTOH, I don't wanna look at what is was December 2008. Quoted: Quoted: Jedi, have you got any investing advice you'd be willing to share here? Not on specific investments, of course, but on basic strategy. (Read: You're beating our retirement accounts' return right now and I'm jealous.) For those who aren't investing, consider this: with a high degree of certainty, everyone here is going to face financial trouble at some time. Ultimately, many of us will have to stop working or slow down significantly in our older years. Start saving for retirement when you are young. Start as early as possible. Allow the power of compounding interest to work for you. Delaying the start of your retirement savings by even a few years can have a big effect on how much interest you earn. I can't speak for ar-jedi, but my super secret strategy is to put money into my 401K at work each payday, which is invested in the stock market. ROR last 12 months: 24.4% http://imageshack.us/a/img29/5383/9qxr.jpg but, this is just between us, OK? shhhhhhhh ETA: OTOH, I don't wanna look at what is was December 2008. ETA: Is there any other more "safe" investments, even if the return is lower? Pushing 30, I need to start thinking about this.

|

|

Quoted:

First, you should separate the what you think from what you know. Well, we know that the economy is not what the MSM blowhard cheerleaders make it out to be. There are 48 million people on food stamps, nearly double the number when OcommiePinko took office. We know that the current unemployment rate does not consider people who have been out of work so long that they've fallen off the gravy train - we know there are several million of these folks based on the employment participation rate being as low now as it was in the early 80s (after Jimmy Carter nearly destroyed the economy). We know that the top banks have more bogus, fake, so-called derivatives now than when the financial crisis started in 2008. We know that the amount of "excess reserves", ie money that banks have on deposit with the Federal Reserve ostensibly because they need to show they can cover losses elsewhere, skyrocketed from 108 billion to 1.08 TRILLION, a factor of 10. Oh, and much of that money was "given" to the banks by the bailout. We know there are currently about 1/6th the number of workers employed in the housing industry as there were in 2006-2007. (So, if you were in that industry, chances are good you're not anymore and won't be for the foreseeable future.) We know that there are already millions of folks whose insurance is being cancelled and will have a huge increase in their costs, and the same will occur again in spades come January. We know that the Administration is hell-bent on gun control, spying on its own citizens, and plans to implement tens of thousands of pages of new regulations within the next year (along with the tens of thousands of pages every year for the last 5). We know that our money is being de-based by roughly 6% per year by the 85 large the Federal Reserve is printing into existence. That's on top of the inflation in food, energy, and other necessities, which are excluded from the .gov's "official" inflation tally. We know that the number of guns and the amount of ammo being purchased this year alone will be double what it was a mere 10 years ago. We know that trust in the .gov, and vice versa, is at its lowest point in American history. We know there were large crowds of people, angry at the petty, stupid things Odumbo demanded as part of the shutdown, who were willing and able to defy government proclamations and visit the people's memorials. By what definition can we legitimately say that the S hasn't already HTF? For a great, great many people, it already has. Further, in terms of the country's financial condition, it hit the fan 5 years ago and has not improved one iota. In fact, our national debt is so high now that a simple reversion to mean historical interest rates would bankrupt the US government because interest on the debt by itself would exceed all revenues from all sources. If, on the other hand you're definition of SHTF is wholesale gunfights between angry citizens and .gov JBTs, then, no, SHTF has yet to begin. As for an "advertised" financial meltdown, we haven't been allowed to see the meltdown that has already occurred because of the incessant pandering of the left-leaning media to its Ocommie master. When, not if, there is another financial crisis like what happened in 2008 happens again, it will be a systemic collapse because there is no headroom left in the economy to absorb the catastrophic losses that would occur. Bank runs and subsequent "holidays" along with capital controls to prevent people from getting their money out of insolvent institutions would occur. How likely is the "worst case" scenario? At this point, 50/50 between now and the end of Odumbo's term. How likely is a real shooting war vs. massive protests and civil unrest? Not very likely, I think. First, the mostly silent majority of people will finally have enough and show up in sufficient numbers to nationwide protests to get the pols attention. Further, the .gov knows it is completely outgunned by sheer numbers, and the .mil will support the Constitution, not the Administration, when push comes to shove. So, this is a long-winded post to basically say there is a "high" likelihood of economic turmoil ala greater than the Great Depression. If you plan to become self-sufficient, financially first, then actually, then regardless of the debilitating financial condition of the rest of the country, you and your family will be safe, fed, clothed, sheltered, and perhaps even prosperous, just as those who lived before us were back then. My $0.031 (after Fed induced inflation is considered). Very well said, and on point as far as I think as well. |

| Forget the record welfare recipients. Forget Obamacare. In one line...the FED is keeping interest low and stock market high. THAT alone cannot last forever. Add in Obamacare this country cannot sustain plus welfare. WE are living on borrowed time my friend. It WILL happen. Knowing when is the secret! |

|

Quoted:

<snip> My take on that is I don't want to ride the burst/bubble train. My father was about to retire in 2008/2009. Can't do that now. He has made a lot back, but the burst can screw you over pretty good if the timing isn't on your side. ETA: Is there any other more "safe" investments, even if the return is lower? Pushing 30, I need to start thinking about this. I am not an investment guru, you might want to seek out the Business and Investment forum. I contribute to the 401K since my job offers it. The money comes out pre-tax so it lowers my taxable income. My job also makes some contributions to it. Not a lot, but some. My first piece of advice is that if you are within a couple of years of retirement, you should not be in the stock market. My work 401K offers several investment options including a fixed income option, when I get close to retirement, I will switch to a safer investment. I have money put into other things as well - including the much disparaged gold/silver. Just another leg of our retirement. If the economy collapses, I lose my 401K money, If the dollar collapses or we have hyper-inflation, I lose my 401K money. So yes, there is a risk - because I don't know how this all ends. OTOH, if things don't collapse, If I retire without saving anything and have to rely on Social Security - I pretty much know exactly how that ends up looking. I will have failed myself and my wife. As to the OP's question, I don't know what will happen in the future, but looking at the debt, the uncontrolled spending, increasing entitlements and freedom of the press at the Federal Reserve, something has to give eventually. No one knows when - anyone that tells you when, is trying to sell you something. This is a scary website: U.S. Debt Clock |

|

Quoted:

ETA: Is there any other more "safe" investments, even if the return is lower? Pushing 30, I need to start thinking about this. First of all, does your job offer any sort of retirement savings plan? Do they match 401k or similar contributions? If they do, find out how much they match and make sure you are getting the full match every year. If you don't, you are essentially turning down free money that should be going into an account earning interest over many years. Once you start your retirement account you can start looking at the various investments available to you. My wife and I are relatively young, so we have more money in moderate risk investments than in low risk investments. We don't invest in individual stocks. |

|

Quoted: First of all, does your job offer any sort of retirement savings plan? Do they match 401k or similar contributions? If they do, find out how much they match and make sure you are getting the full match every year. If you don't, you are essentially turning down free money that should be going into an account earning interest over many years. Once you start your retirement account you can start looking at the various investments available to you. My wife and I are relatively young, so we have more money in moderate risk investments than in low risk investments. We don't invest in individual stocks. Quoted: Quoted: ETA: Is there any other more "safe" investments, even if the return is lower? Pushing 30, I need to start thinking about this. First of all, does your job offer any sort of retirement savings plan? Do they match 401k or similar contributions? If they do, find out how much they match and make sure you are getting the full match every year. If you don't, you are essentially turning down free money that should be going into an account earning interest over many years. Once you start your retirement account you can start looking at the various investments available to you. My wife and I are relatively young, so we have more money in moderate risk investments than in low risk investments. We don't invest in individual stocks. |

|

Quoted:

But what is the likely that something will actually happen. I keep reading civil unrest, government complete takeover, nuclear war, and what ever else anyone can think of. Oh zombies. But the economy is tanking and it has for years and no SHTF. I would like someone to try to explain it to me. Please. I am just not that informed I guess. Bad stuff happens all the time. Open the newspaper any day of the week Floods. Windstorms Unemployment Cold snaps chemical spills. Doesn't have to be a sci fi-type event. Whats a little peace of mind worth to you? Do you have dependents? What sort of rainy day preps for hard times do you think you owe your kids, if you have any? |

|

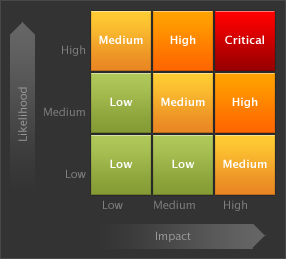

If we look at life using typical Risk Management logic, we'd fall back to Risk = Likelihood x Impact. "Effective Risk" incorporates Mitigation Strategies and Contingency Plans, which tells you what your real risk is. The chances of you getting in a car accident TODAY are low, but the impact for someone completely unprotected (typically death) drives us to incorporate cost-effective Mitigation Strategies (seatbelts). In general, we tend to implement Mitigation Strategies or Contingency Plans for things that could kill us - no matter how unlikely they are.

While there are some places you can impact likelihood (ex: performance on the job reducing your likelihood of being laid off) - many instances you can't. Stuff happens - whether it be on a personal, local, or worldwide level. The combination of Likelihood and Impact allows us to identify threats that we care about enough to do something about them (i.e. mitigate, or create contingency plans). A low likelihood situation that would have a low impact (if it did happen) isn't really anything we'd spend our time on. An extremely expensive mitigation for a medium risk isn't the right answer either. Wearing a seatbelt is essentially free, and we do it because of the impact of an unprotected accident. Anyway, whether we think about it in these terms, all of our preparations (from health insurance to a GHB) are driven by these considerations (or should be). Here's a random risk matrix I grabbed off the internet:

So what's in your top right quadrant? I would suggest job loss, a lack of a comfortable retirement or medical emergency would be for most people. TSHTF perhaps isn't very likely, but the impact is high enough that smart people have some reserves of food, water, shelter, etc. As many here have stated - most preps are universal, so it's not appropriate to think that everyone who has cases of bottled water is preparing for zombies. Reduce your likelihood of problems. Stay in good health, don't drive after midnight, stay out of bad neighborhoods, etc. Then implement mitigations or contingency plans for things that are a serious threat to your way of life. Whether that's zombies, economy or nuclear war is kind of a personal exercise (based highly on your opinions of what you believe the threats are). Your point is probably that "we" (self reliant people) don't always do a good job of that. There are a few threads about losing weight and investments right here on page #1, which I think is a good sign. I haven't seen a "what kind of gun should I buy?" thread in a while. To me, that's the sign of a relatively mature group, but that's just my two cents..... |

|

I think that all sides have truth. I would guess the # 1 SHTF event in America today is an unexpected illness/accident which racks up many thousands of dollars in bills combined with the inability to work. This could lead most families to the brink of bankrupcy in a month or two. I would guess that the #2 would be loss of your job. Everyone should be preparing financially for one of these two to happen to them. Having enough cash in the bank to survive for 2-3 months should be the first "prep" everyone should have in my mind. Divorce is probably very high on the list as well, in terms of a financial SHTF. After these come natural disasters, in my mind, which are USUALLY short lived (Katrinas are rare). Having 2 weeks worth of food, a source of water and a way to heat your house with the power out (assuming you live in a climate where this is necessary) seem like pretty common sense ideas. This doesn't require $1000s of dollars in "preps", but just having two extra weeks worth of food, and a way to store water (I think the "water bob" looks pretty simple and effective), as well as perhaps a generator and a wood stove. Is there a financial melt down coming? I am sure there is, but I don't think anyone can predict when it will be. I would have thought the Euro would have had a crisis/crash a few years ago, but they seem able to keep things going much longer than I expected. We clearly cannot maintain the path we are taking as a nation, but can we stumble along for another 1 year or 20 years? I don't know. The stock market was a good investment in 2013 because much of the money the fed invents has inflated it. I don't think that most investors look at the fundamentals of companies (profit and loss) any more, they just follow the emotional rollercoaster that is "the market". Eventually this bubble to will crash, but again I don't know if it will be next month or 5 years from now. I think that having 10-20% of your investments in precious metals is a good idea. They aren't going to make you a lot of money on paper, but when the dollar begins its inevitable collapse, they will become the bulk of your savings. When this happens, having your "BOL" with 40 acres to plow and your "fire team" of neighbors might become relevant. I would guess that having a few guns and an acre or so to garden on would be pretty helpful, so planting a garden and developing some experience in growing things would be a good way to plan for this. That's my $0.02 |

|

I think fema recomends 3 days of food and water. Depending on your location local stuff is something to consider. Hurricane or tornado or tourists or flamingos or whatever. A housefire is a game changer for many people. I have had a 4 day power outage and the next year I was all set for it again and did not get the ice storm. What sucked is the parents got the icestorm and I went and fixed all their problems and a sister headed that way and made it to the driveway only to get stuck on the plow trucks ice/snow berm so I had to help that vehicle out as well. Right now, your ability to pay your bills and feed you and yours and keep a warm roof over your head might be all you need to worry about. |

| I don't prep for any event. My goal is to maintain continuity even when bumps in the road appear. That could be something normal and mundane like getting laid off, something out of the ordinary and potentially catastrophic like the flooding my state (and my city... and some of my neighbors) experienced last September or something completely epic like grid failure or economic collapse. I try to live a lifestyle that primarily lets me keep my family (and me) healthy, sheltered and fed and secondarily keeps me solvent, marketable and networked with my local community for news, shared defense and basic social skills. |

|

no. i attempted for two years to bring something resembling sanity into the B&I forum. in my experience there is little to be found there. every thread ended with a pile of people demanding that the OP buy precious metals and bullets, and completely ignore rational asset allocation approaches. i gave up. even Sisyphus gets tired. if you want good, useful financial guidance from folks who have something more to offer: http://www.fatwallet.com/forums/finance/ FWF is like ARFCOM GD, only very finance-oriented. some of the stuff that folks suggest AND do in FWF is incredibly brilliant. some of it would cause members of the SF to run screaming from the room. note: you are going to need a thick skin if you want to toy with folks there. if you start a thread asking whether you should buy or lease a new car, you are going to get pummeled with replies about tacked threads. on the other hand i have seen some of the absolutely oddest scenarios played out and the advice given is top notch. there is a brazen honesty in both the OP's and the replies on FWF, which is simultaneously refreshing and also pushes aside some of the social tiptoeing that occurs in other forums. by the way, the "FWF vehicle of choice" is the Crown Vic PI edition... http://socialize.morningstar.com/NewSocialize/asp/AllConv.asp?forumId=F100000026 morningstar's forums have a unique attribute: it costs $5 for a lifetime subscription, which enables you to post. that's it, you pay $5 once and you are good forever. the reason for this is that it completely removes the spammers, as well as the folks who just create an account to stir trouble. for this reason M* forums are the opposite of ARFCOM GD. that said, the Fidelity-specific forum on M* may seem like an odd place to point you to, but i assure you that a many of the folks in the T/A (technical analysis) and market/economy relevant threads in the Fido forum know EXACTLY what they are doing. if you do nothing but read the threads in M*'s Fido forum once a week for two months, i guarantee you will be way ahead of the curve on market economics. you can make a decent amount of money in the bond market (by buying or selling bond funds about every 6 months) doing nothing else other than monitoring threads in the M* Fidelity forum. http://seekingalpha.com/ seeking alpha is quant-heaven. it is also one of the best places to get raw financial news, from folks that deal in finance, rather than folks that deal in "the news". for this reason you get unbridled analysis of trends and so on. e.g. http://seekingalpha.com/article/1903641-zero-hedge-is-wrong-about-gold most of what is presented on SA is going to be slightly esoteric for the typical individual investor. nevertheless some of the information will provide a lot of insight into *why* certain companies or markets will succeed or will be doomed. i have to credit a story on SA for the single best investment that i ever made; in the 10 years that i owned it, it returned a stratospheric amount of money and i'm looking for a reentry point on it, although it's much less of a secret now. http://www.bogleheads.org/forum/index.php bogleheads is simultaneously the most user-friendly financial investing site but also the most religious. the "john bogle" way dictates investment behaviors which don't provide a lot of latitude. for example, a so-called boglehead would opine that the *only* way to invest in the equities market is via a total market index fund. why? because it has the lowest intrinsic cost, the most breadth and therefore the least risk, and statistically outperforms the majority of "managed money" in traditional mutual funds. i encourage you to get an account on bogleheads and inform them that they are all wrong, and that there is a better way. i'm exaggerating a bit here, of course. i will say that if you have a financial situation which you would like some advice on -- example, i'm 34, i have two young kids, i want them to go to college, what's the best way to invest so i can pay for it? -- you will get a variety of excellent ideas and positive advice from the folks on the bogleheads forum. bogleheads is another site where if you would just read once a week for a couple of months you will learn an incredible amount of useful, practical information. http://www.early-retirement.org/forums/ the religion at this forum is known as "FIRE" -- "financial independence, retire early" -- and it is the mantra of this website. the idea of FIRE is to "get off the merry-go-round" as soon as possible; that means different things to different people, but in the end it's the same: escape. read this forum and learning how people are planning to FIRE, how they are actually doing FIRE, and finally how they did FIRE. one thing you will notice is that these folks DO NOT SPEND MONEY ON NON-ESSENTIAL things. if you ever need to be told, "it's not what you make, it's what you save", well this is the place. related to the above site is this tool: http://www.firecalc.com/ (there is an entire forum at the above site discussing how to use/not misuse this tool, incidentally) the point of this tool is straightforward in terms of answering questions: given you want to retire, how much will you need, how quickly will it be used up, and what return will you need? the tool uses Monte Carlo simulation to statistically work out the bounds of various market scenarios, and how they will affect your retirement monies. ps to finish up, the single text that i would advise folks pick up is Ferri's "All About Asset Allocation". after you read this the light will go on, and it will help you take "big picture" stock of your investments in totality. the $20 or whatever this book costs at Amazon will be repaid many times over. ar-jedi |

|

Quoted:

Jedi, have you got any investing advice you'd be willing to share here? Not on specific investments, of course, but on basic strategy. Quoted:

Quoted:

Snip Jedi, have you got any investing advice you'd be willing to share here? Not on specific investments, of course, but on basic strategy. read the websites above.

seriously, though, the reason i posted that snippet of my account summary is simple: your own "economy" is FAR more important than the country's. it is also very much disconnected -- it is certainly possible to personally make a lot of money when the economy is "bad" (hella money made in the bond market when the Fed was ratcheting down interest rates), and personally lose a lot of money when the economy is "good" (hella money lost by folks over-leveraging themselves into real estate -- an asset allocation boo-boo on a large scale). for this reason, one should work on the things that are in your immediate control -- your job, your mortgage, your expenses, your long term investments, and so on. you can't control the economy, that's for sure. but you can ask for a raise; you can refinance your mortgage; you can reign in your expenses; you can pay attention to your long term investments, and so on. http://en.wikipedia.org/wiki/Locus_of_control In personality psychology, locus of control refers to the extent to which individuals believe that they can control events that affect them. Understanding of the concept was developed by Julian B. Rotter in 1954, and has since become an aspect of personality studies. A person's "locus" (Latin for "place" or "location") is conceptualised as either internal (the person believes they can control their life) or external (meaning they believe that their decisions and life are controlled by environmental factors which they cannot influence). Individuals with a high internal locus of control believe that events in their life derive primarily from their own actions; for example, when receiving test results, people with an internal locus of control would praise or blame themselves and their abilities, whereas people with a extra high external locus of control would praise or blame the teacher or the test. ar-jedi |

|

Quoted:

ETA: OTOH, My take on that is I don't want to ride the burst/bubble train. My father was about to retire in 2008/2009. Can't do that now. He has made a lot back, but the burst can screw you over pretty good if the timing isn't on your side. ETA: Is there any other more "safe" investments, even if the return is lower? Pushing 30, I need to start thinking about this. what you describe above is mitigated through an investing technique called "asset allocation". once you understand why this so important, you can begin to make investment decisions that will minimize risk and maximize return. the short version of asset allocation is "don't put all your eggs in one basket". read Ferri's book on this topic. ar-jedi |

|

Quoted:

no. i attempted for two years to bring something resembling sanity into the B&I forum. in my experience there is little to be found there. every thread ended with a pile of people demanding that the OP buy precious metals and bullets, and completely ignore rational asset allocation approaches. i gave up. even Sisyphus gets tired. ar-jedi Quoted:

no. i attempted for two years to bring something resembling sanity into the B&I forum. in my experience there is little to be found there. every thread ended with a pile of people demanding that the OP buy precious metals and bullets, and completely ignore rational asset allocation approaches. i gave up. even Sisyphus gets tired. ar-jedi I will defer to you on this one. I don't spend much time there and as stated I am not a financial guy. Thanks for the many links. Knowledge is good. and I agree about "personal" economy. I stayed steadily employed through the 2008 meltdown and have not felt much effects, other than my 401K hit, which I have now recovered and since I kept adding to it during the downturn, I now have more than I would have had. |

|

and if you guys didn't believe me that FWF is just like ARFCOM GD, only finance-related, i bring you: http://www.ar15.com/forums/t_1_5/1569786_guy_has__45_000_cash_and_there_is_apparently_no_way_to_deposit_it_in_a_bank.html ar-jedi |

|

Quoted:

Zombies are used as a metaphor of sorts. If youre prepped for zombies, youre prepped for any SHTF scenario. I agree with the above posters that its better to have it and not need it, than need it and not have it. And no one can perfectly predict these coming scenarios. Even a little bit helps. So just keep doing what youre doing. THIS |

|

Quoted:

ETA: Is there any other more "safe" investments, even if the return is lower? Pushing 30, I need to start thinking about this. Risk reduction comes from diversification and asset allocation decisions, not so much any one thing you choose to invest in. Read Ferri's book, as ar-jedi suggested. At least the first few chapters. There's a kindle version you can start reading 4 minutes from now. Seriously ... a few bucks and the next hour of your time could fundamentally change how you understand investing and change your life for the better, long term. (And if you decide it's crap, you're only out a few bucks and a couple hours.) Posted Via AR15.Com Mobile |

|

Quoted:

Read Ferri's book, as ar-jedi suggested. At least the first few chapters. There's a kindle version you can start reading 4 minutes from now. Seriously ... a few bucks and the next hour of your time could fundamentally change how you understand investing and change your life for the better, long term. (And if you decide it's crap, you're only out a few bucks and a couple hours. ^^^ this. here is amazon link http://www.amazon.com/About-Asset-Allocation-Second-Edition/dp/0071700781 or this equivalent http://www.amazon.com/The-Intelligent-Asset-Allocator-Portfolio/dp/0071362363/ref=pd_cp_b_0 these are not finance math books. these are not stock picking books. these are not feel-good tomes about a millionaire next door. these are not doom/gloom sagas. these texts explain what asset allocation is, and why it is THE MOST IMPORTANT FACET of your investment/retirement portfolio. these texts go on to provide common examples, solutions to typical scenarios, and a list of do's/don'ts that keep you out of trouble. the best thing these texts do is point out what you already probably know -- you just don't know how to quantify it as risk-adjusted return. example: i tell you i have 5 houses worth $900K, along with $1M in mortgage debt, and no retirement savings. it should be obvious to you that i am overly committed to real estate, and a tiny little perturbation to the real estate market will send my financial life spiraling downward. this is an example of an asset allocation mistake. asset allocation issues in your overall portfolio are more subtle, of course, but can have a profound effect on risk vs return. hence the texts. one great way to get a head start is to use Morningstar's free "Instant Xray" tool. http://portfolio.morningstar.com/NewPort/Free/InstantXRayDEntry.aspx?tsection=toolsxray&dt=0.7055475 here is an example: http://www.ar15.com/forums/t_1_133/1122005__ARCHIVED_THREAD____IRA_not_making_dukey__AR_Jedi_help___Update__last_post.html and another: http://www.ar15.com/forums/t_1_133/583439__ARCHIVED_THREAD____401k_advice___Updated_to_include_ticker_symobols.html ar-jedi |

|

Well, we have a prediction...

And I heard a voice in the midst of the four beasts say, A measure of wheat for a penny, and three measures of barley for a penny; and see thou hurt not the oil and the wine.

When he opened the sixth seal, I looked, and behold, there was a great earthquake, and the sun became black as sackcloth, the full moon became like blood. The sky was rolled up like a scroll, and every mountain and island was removed from its place. And the kings of the earth, and the great men, and the rich men, and the chief captains, and the mighty men, and every bondman, and every free man, hid themselves in the dens and in the rocks of the mountains; |

|

Open your eyes and you'll see the shit hitting fans every where every day.

I don't need to have the dead rising from the ground to need a month's worth of cash in my bank account - how about a stolen debt card? I don't need to have a 7.0 earthquake to have a months worth of food in the house - how about breaking a leg so you can't go to work? I don't need an EMP blast to have a hundred ounces of silver (or gold!!!) in the safe - how about you lose your job? I don't need to have an urban riot burning homes in my neighborhood to want to own a semi-automatic M4gery - how about a home invasion robbery? |

|

Really, why don't you ask "why do you put your seatbelt on?"

Do you really expect a head-on collision or a blowout and subsequent roll-over? You are aware of the dangers, and prepare accordingly. Do your homework, understand your threat assessment and go from there... |

|

Preppers/Survivalists/Whatever are just simply people with situational awareness who realize there are a lot of bad things that can happen. These people then take steps to soften the blow if they find themselves in that bad situation. It's just that simple on the macro level. When you get down to specific "bad things" is where there is different strategies and different steps to take in anticipation of whatever event the individual feels is most threatening. If you cover your bases on the following points you will be able to endure a lot of adversity in life:

-debt reduction -> debt elimination -diversified assets - insurance -resources (food, water, shelter, transportation) - tools to maintain your resources (be it guns, a generator, or spark plug wrench) and the two most important: KNOWLEDGE and SITUATIONAL AWARENESS Embrace these ideas and those that others have mentioned and you'll at least have a fighting chance with whatever life throws at you |

|

Good thread with some good posts...

I don't prep for zombies... But I do try to prepare for some event that would have me without the"things" I might need... I figure 3 months is a good figure... 3 months not being able to go to work or a store would mean that there is a lot wrong with our country/ world. But keep in mind prepping is not just about "things" its as much a mindset and though process as it is "stuff." Prepare for the most likely first and least likely last... With all that said I myself need to stop buying so much "stuff" and start saving more cash as the money factor or job loss will hit us all long before we are "running & gunning." I am sure many of us will be going to work in a dangerous and degraded society before we are humping or bug out bags with tactical thy holsters and slung rifles... But you never know, and that's why we prepare. For me it is a lifestyle and hobby that I love, I don't just pile up my survival gear and stash it away, I enjoy bush-crafting, hunting, camping... I am fortunate enough to live on some acreage where I can "play." I would call myself a gear geek in some respects. I am an amateur radio operator, I don't just have ham radios for SHTF, I enjoy using them and am very active in the public service/ emergency preparedness aspect of ham. I have fun with it, but if I ever "need" it I am prepared with the gear and skills needed for just about any comm. Same goes with my wilderness gear, my vehicle, my equipment I use every day to heat my house with firewood... The list goes on. |