|

[#1]

Quoted:

That's great if the stocks do, ok to well, if they tank then that person would undoubted be cynical to the market for a long time. Just playing devil's advocate. Maybe a sim account for individual stocks first. Quoted:

Quoted:

Everyone learns differently but ONE way that might work for you is to learn by doing. Open up an IRA with an online broker (ETrade, TD Ameritrade, Merrill Lynch, ect) and fund it with $500. Buy a couple stocks to start and pick some big names that you know. The Dow 30 list is a good place to start: http://money.cnn.com/data/dow30/ Sit back and then follow your monthly statements to see how it works. The questions will come up at a less than rapid fire pace so you'll have the ability to tackle one thing at a time. What's a P/E ratio? What's a dividend? Why do earnings matter? Ect... I specifically recommend buying individual stocks before getting into mutual funds. Mutual funds are likely where you want to end up but they are ultimately comprised of individual investments like stocks and bonds, so I think it is important to understand the fundamental units of what you will be investing in before you start dumping money into mutual funds. It's like learning how to cut a board or hammer a nail before you start building a house. Now before anyone chimes in with "OMG, Woodsie, it's so inefficient to buy stocks in lots of $100 to $200 at a time", please remember that the purpose of this exercise is to get familiar investing. So what if she sucks up $10 to $40 in commissions to get her $500 invested? It's worth it to figure out what you are doing with small dollars before you invest big dollars and $10 to $40 is a small price to pay for an education. That's great if the stocks do, ok to well, if they tank then that person would undoubted be cynical to the market for a long time. Just playing devil's advocate. Maybe a sim account for individual stocks first. That's a great point. It's no fun getting burned, even if you expect that it may happen. |

|

|

|

[#2]

Quoted:

You need 100 shares of stock to really get in. That being said Buy- Waste management incorporated - garbage is big business, it's good no matter the economy. I should have bought it when it was cheaper. You won't buy it anyways... Quoted:

Quoted:

What single stock would it be invested in? You need 100 shares of stock to really get in. That being said Buy- Waste management incorporated - garbage is big business, it's good no matter the economy. I should have bought it when it was cheaper. You won't buy it anyways... Holy PE batman. |

|

|

|

[#3]

Quoted:

That's a great point. It's no fun getting burned, even if you expect that it may happen. Quoted:

Quoted:

Quoted:

Everyone learns differently but ONE way that might work for you is to learn by doing. Open up an IRA with an online broker (ETrade, TD Ameritrade, Merrill Lynch, ect) and fund it with $500. Buy a couple stocks to start and pick some big names that you know. The Dow 30 list is a good place to start: http://money.cnn.com/data/dow30/ Sit back and then follow your monthly statements to see how it works. The questions will come up at a less than rapid fire pace so you'll have the ability to tackle one thing at a time. What's a P/E ratio? What's a dividend? Why do earnings matter? Ect... I specifically recommend buying individual stocks before getting into mutual funds. Mutual funds are likely where you want to end up but they are ultimately comprised of individual investments like stocks and bonds, so I think it is important to understand the fundamental units of what you will be investing in before you start dumping money into mutual funds. It's like learning how to cut a board or hammer a nail before you start building a house. Now before anyone chimes in with "OMG, Woodsie, it's so inefficient to buy stocks in lots of $100 to $200 at a time", please remember that the purpose of this exercise is to get familiar investing. So what if she sucks up $10 to $40 in commissions to get her $500 invested? It's worth it to figure out what you are doing with small dollars before you invest big dollars and $10 to $40 is a small price to pay for an education. That's great if the stocks do, ok to well, if they tank then that person would undoubted be cynical to the market for a long time. Just playing devil's advocate. Maybe a sim account for individual stocks first. That's a great point. It's no fun getting burned, even if you expect that it may happen. I just wanted to mention it, I have talked with several people who got burned by fly by night brokers making promises about investing and then convincing these folks to sell CD's to buy Equity or MFs. I am not going to mention the Broker dealer, but they were famous for their new guys to call everyone and convince them to buy single stocks. A lot people liquidated their 5-6% short-intermediate term CDs to buy World com, Cisco etc in hope of better returns and we all know how they did in the turn of the century. From then on, they have been extremely skeptical and cynical which has caused them to revert back to short term cd's and miss out on growing their money. |

|

|

|

[#4]

Quoted:

so what you are saying is that rates are going to be high enough to warrant a rotation out of equities back into fixed income? But then FI is going to get hit hard by the effect of duration, so then where are you going to go? We didn't even hit euphoria yet where the retail guys get in at the peak of the cycle of the equity bull market.  Quoted:

Quoted:

There are many parallels today with 1929. Anyone who is serious about investing in stocks should read John Kenneth Galbraith's The Great Crash 1929. I don't think the crash will be this year but the Chair of the St. Louis Federal Reserve did say that interest rates should go up in the first quarter of 2015. so what you are saying is that rates are going to be high enough to warrant a rotation out of equities back into fixed income? But then FI is going to get hit hard by the effect of duration, so then where are you going to go? We didn't even hit euphoria yet where the retail guys get in at the peak of the cycle of the equity bull market. Nope. Missed by a wide margin. When interest rates go up, the derivatives market, stock and bond market goes TU. |

|

|

|

[#5]

Quoted:

Nope. Missed by a wide margin. When interest rates go up, the derivatives market, stock and bond market goes TU. Quoted:

Quoted:

Quoted:

There are many parallels today with 1929. Anyone who is serious about investing in stocks should read John Kenneth Galbraith's The Great Crash 1929. I don't think the crash will be this year but the Chair of the St. Louis Federal Reserve did say that interest rates should go up in the first quarter of 2015. so what you are saying is that rates are going to be high enough to warrant a rotation out of equities back into fixed income? But then FI is going to get hit hard by the effect of duration, so then where are you going to go? We didn't even hit euphoria yet where the retail guys get in at the peak of the cycle of the equity bull market. Nope. Missed by a wide margin. When interest rates go up, the derivatives market, stock and bond market goes TU. I'm pretty bearish, but for other reasons. Don't underestimate the power of the Fed to hold rates lower longer than you would ever believe possible

|

|

|

|

[#6]

Quoted:

Thanks. I'll try to figure it out. I hope I can do this smoothly from my 401k into an IRA. Quoted:

Quoted:

Quoted:

Quoted:

Put it in a Roth IRA (may need to add more to reach your income bracket maximum), repeat yearly with your income bracket maximum, withdrawal after you turn 59.5 years of age. I just tried to do that with my old 401k today. The lady at my bank said the IRA she could put me in wouldn't even keep up with inflation and it wasn't worth it. Said she couldn't do anything for me. I'm in Skink's boat, I'm trying to figure out what to do with it and whatever else ends up in my savings account. Halp. What kind of shitty IRAs do you have? Look into Fidelity Thanks. I'll try to figure it out. I hope I can do this smoothly from my 401k into an IRA. For IRAs I suggest you seriously consider Vanguard. They have some decent choices and low fees. |

|

|

|

[#7]

Already doing that for the me and the missus

|

|

|

|

[#8]

Quoted:

Nope. Missed by a wide margin. When interest rates go up, the derivatives market, stock and bond market goes TU. Quoted:

Quoted:

Quoted:

There are many parallels today with 1929. Anyone who is serious about investing in stocks should read John Kenneth Galbraith's The Great Crash 1929. I don't think the crash will be this year but the Chair of the St. Louis Federal Reserve did say that interest rates should go up in the first quarter of 2015. so what you are saying is that rates are going to be high enough to warrant a rotation out of equities back into fixed income? But then FI is going to get hit hard by the effect of duration, so then where are you going to go? We didn't even hit euphoria yet where the retail guys get in at the peak of the cycle of the equity bull market. Nope. Missed by a wide margin. When interest rates go up, the derivatives market, stock and bond market goes TU. 50bp is hardly going to make a dent in the equities market. ar-jedi |

|

|

|

[#9]

Quoted:

Nope. Missed by a wide margin. When interest rates go up, the derivatives market, stock and bond market goes TU. Quoted:

Quoted:

Quoted:

There are many parallels today with 1929. Anyone who is serious about investing in stocks should read John Kenneth Galbraith's The Great Crash 1929. I don't think the crash will be this year but the Chair of the St. Louis Federal Reserve did say that interest rates should go up in the first quarter of 2015. so what you are saying is that rates are going to be high enough to warrant a rotation out of equities back into fixed income? But then FI is going to get hit hard by the effect of duration, so then where are you going to go? We didn't even hit euphoria yet where the retail guys get in at the peak of the cycle of the equity bull market. Nope. Missed by a wide margin. When interest rates go up, the derivatives market, stock and bond market goes TU. The stock and bond markets are not derivatives of the FOMC's interest rate policy technically speaking. While inflation is normally bad due to what the Fed does by purposely slowing the economy, it is not the inflation by it's self. The Fed has been extremely accommodating to the economy. Plus, you actually have to have some inflation to occur for the fed to freak out. You are right on one major point, Rates up bonds take a on trading value. Here's a chart

|

|

|

|

[#10]

Quoted:

50bp is hardly going to make a dent in the equities market. ar-jedi Quoted:

Quoted:

Quoted:

Quoted:

There are many parallels today with 1929. Anyone who is serious about investing in stocks should read John Kenneth Galbraith's The Great Crash 1929. I don't think the crash will be this year but the Chair of the St. Louis Federal Reserve did say that interest rates should go up in the first quarter of 2015. so what you are saying is that rates are going to be high enough to warrant a rotation out of equities back into fixed income? But then FI is going to get hit hard by the effect of duration, so then where are you going to go? We didn't even hit euphoria yet where the retail guys get in at the peak of the cycle of the equity bull market. Nope. Missed by a wide margin. When interest rates go up, the derivatives market, stock and bond market goes TU. 50bp is hardly going to make a dent in the equities market. ar-jedi especially when the fed's target is 0-.25, you want to make the economy start moving. get the fed to stop paying on bank reserve deposits. That guy that bought the 30 year though is going to be a little upset. |

|

|

|

[#11]

Quoted:

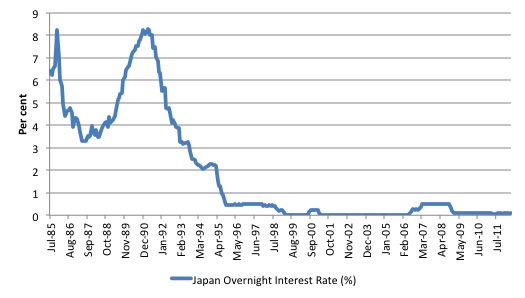

I'm pretty bearish, but for other reasons. Don't underestimate the power of the Fed to hold rates lower longer than you would ever believe possible http://bilbo.economicoutlook.net/blog/wp-content/uploads/2012/06/Japan_overnight_interest_rates_1985_2012.jpg Quoted:

Quoted:

Quoted:

Quoted:

There are many parallels today with 1929. Anyone who is serious about investing in stocks should read John Kenneth Galbraith's The Great Crash 1929. I don't think the crash will be this year but the Chair of the St. Louis Federal Reserve did say that interest rates should go up in the first quarter of 2015. so what you are saying is that rates are going to be high enough to warrant a rotation out of equities back into fixed income? But then FI is going to get hit hard by the effect of duration, so then where are you going to go? We didn't even hit euphoria yet where the retail guys get in at the peak of the cycle of the equity bull market. Nope. Missed by a wide margin. When interest rates go up, the derivatives market, stock and bond market goes TU. I'm pretty bearish, but for other reasons. Don't underestimate the power of the Fed to hold rates lower longer than you would ever believe possible http://bilbo.economicoutlook.net/blog/wp-content/uploads/2012/06/Japan_overnight_interest_rates_1985_2012.jpg Just read an email with these charts attached (hat tip John Mauldin) - they help partially explain why I don't think rates will be rising (meaningfully) any time soon. Keep in mind, rising rates mean lower revenues and substantially more interest than is depicted here - a much worse situation. While I wish this wasn't so, it is what it is at this point.

|

|

|

|

[#12]

Quoted:

That guy that bought the 30 year though is going to be a little upset. for every loser, a winner? ar-jedi --> has 3.25% fixed mortgage note |

|

|

|

[#13]

Quoted:

for every loser, a winner? ar-jedi --> has 3.25% fixed mortgage note Quoted:

Quoted:

That guy that bought the 30 year though is going to be a little upset. for every loser, a winner? ar-jedi --> has 3.25% fixed mortgage note That is true. |

|

|

|

[#14]

Quoted:

for every loser, a winner? ar-jedi --> has 3.25% fixed mortgage note Quoted:

Quoted:

That guy that bought the 30 year though is going to be a little upset. for every loser, a winner? ar-jedi --> has 3.25% fixed mortgage note not always

I can think of about three retirees off the top of my head who would consider loaning to ar-jedi at 3.25% for a mortgage to be a win-win. |

|

|

|

[#15]

GPS technology stocks

or Bourbon or 50 shares of cheap hookers and blow. You will feel more happy with this one than any. |

|

|

|

[#16]

Quoted:

I can think of about three retirees off the top of my head who would consider loaning to ar-jedi at 3.25% for a mortgage to be a win-win. i already have a 3.25% loan. my new target rate is 2.75% now. are there still multiple takers? if so, i am just going to continue a binary search for the lowest rate... ar-jedi |

|

|

|

[#17]

Quoted:

i already have a 3.25% loan. my new target rate is 2.75% now. are there still multiple takers? if so, i am just going to continue a binary search for the lowest rate... ar-jedi Quoted:

Quoted:

I can think of about three retirees off the top of my head who would consider loaning to ar-jedi at 3.25% for a mortgage to be a win-win. i already have a 3.25% loan. my new target rate is 2.75% now. are there still multiple takers? if so, i am just going to continue a binary search for the lowest rate... ar-jedi ha, not a bad idea. Still about 50bps over the current highest 5-year jumbo CD rate I've seen. If I was buying a house, I would seriously shop this just to avoid closing costs. |

|

|

|

[#18]

Quoted:

not always

I can think of about three retirees off the top of my head who would consider loaning to ar-jedi at 3.25% for a mortgage to be a win-win. Quoted:

Quoted:

Quoted:

That guy that bought the 30 year though is going to be a little upset. for every loser, a winner? ar-jedi --> has 3.25% fixed mortgage note not always

I can think of about three retirees off the top of my head who would consider loaning to ar-jedi at 3.25% for a mortgage to be a win-win. Its scary that people would actually invest money in something that returns that poor. |

|

|

|

[#19]

Quoted:

Its scary that people would actually invest money in something that returns that poor. Quoted:

Quoted:

Quoted:

Quoted:

That guy that bought the 30 year though is going to be a little upset. for every loser, a winner? ar-jedi --> has 3.25% fixed mortgage note not always

I can think of about three retirees off the top of my head who would consider loaning to ar-jedi at 3.25% for a mortgage to be a win-win. Its scary that people would actually invest money in something that returns that poor. I said three, but actually the two specific examples that I am thinking of are a couple of guys I used to help with their businesses. These are people that have done everything right - saved $1-2 million for retirement, changed their asset allocation from equities to fixed income as they got closer to retirement under the model that they were taught. They are now retired, and had all gone as planned would be making somewhere in the order of 4-5%. So, on $2 million that is $80-100k a year. Houses are paid for, a large portion of day-to-day living expenses are covered by pensions, and they have great long-term care insurance. They are fully in "protect the principal" mode and no argument in the world will change their minds. They have also lived through a few market meltdowns at this point and have friends who are struggling to make ends meet (who also saved well, but were invested in riskier assets at the wrong time). It sucks for them, but they will end up taking 2.5% in jumbo CDs from a variety of banks to keep them FDIC insured. I don't see any alternative. Even if I could talk them back into equities (and there is no way in hell I could), dividend yields on the higher rated stocks are still 2-3% and they aren't going to be interested in anything riskier at this point in their lives. |

|

|

|

[#20]

Quoted:

I said three, but actually the two specific examples that I am thinking of are a couple of guys I used to help with their businesses. These are people that have done everything right - saved $1-2 million for retirement, changed their asset allocation from equities to fixed income as they got closer to retirement under the model that they were taught. They are now retired, and had all gone as planned would be making somewhere in the order of 4-5%. So, on $2 million that is $80-100k a year. Houses are paid for, a large portion of day-to-day living expenses are covered by pensions, and they have great long-term care insurance. They are fully in "protect the principal" mode and no argument in the world will change their minds. They have also lived through a few market meltdowns at this point and have friends who are struggling to make ends meet (who also saved well, but were invested in riskier assets at the wrong time). It sucks for them, but they will end up taking 2.5% in jumbo CDs from a variety of banks to keep them FDIC insured. I don't see any alternative. Even if I could talk them back into equities (and there is no way in hell I could), dividend yields on the higher rated stocks are still 2-3% and they aren't going to be interested in anything riskier at this point in their lives. Quoted:

Quoted:

Quoted:

Quoted:

Quoted:

That guy that bought the 30 year though is going to be a little upset. for every loser, a winner? ar-jedi --> has 3.25% fixed mortgage note not always

I can think of about three retirees off the top of my head who would consider loaning to ar-jedi at 3.25% for a mortgage to be a win-win. Its scary that people would actually invest money in something that returns that poor. I said three, but actually the two specific examples that I am thinking of are a couple of guys I used to help with their businesses. These are people that have done everything right - saved $1-2 million for retirement, changed their asset allocation from equities to fixed income as they got closer to retirement under the model that they were taught. They are now retired, and had all gone as planned would be making somewhere in the order of 4-5%. So, on $2 million that is $80-100k a year. Houses are paid for, a large portion of day-to-day living expenses are covered by pensions, and they have great long-term care insurance. They are fully in "protect the principal" mode and no argument in the world will change their minds. They have also lived through a few market meltdowns at this point and have friends who are struggling to make ends meet (who also saved well, but were invested in riskier assets at the wrong time). It sucks for them, but they will end up taking 2.5% in jumbo CDs from a variety of banks to keep them FDIC insured. I don't see any alternative. Even if I could talk them back into equities (and there is no way in hell I could), dividend yields on the higher rated stocks are still 2-3% and they aren't going to be interested in anything riskier at this point in their lives. Your Broker dealer doesn't offer structured products? |

|

|

|

[#21]

Quoted:

Your Broker dealer doesn't offer structured products? They don't want the credit risk after Lehman |

|

|

|

[#22]

Quoted:

They don't want the credit risk after Lehman Quoted:

Quoted:

Your Broker dealer doesn't offer structured products? They don't want the credit risk after Lehman Your clients not your BD right? They don't ever want the FDIC insured stuff? Lehman bros bit the BD I stared out at in the ass big time. Even worse than world com bit them. The worst part about lehman is you had an opportunity to get out and about 70-80% of par before they went belly up. |

|

|

|

[#23]

Quoted:

I said three, but actually the two specific examples that I am thinking of are a couple of guys I used to help with their businesses. These are people that have done everything right - saved $1-2 million for retirement, changed their asset allocation from equities to fixed income as they got closer to retirement under the model that they were taught. They are now retired, and had all gone as planned would be making somewhere in the order of 4-5%. So, on $2 million that is $80-100k a year. Houses are paid for, a large portion of day-to-day living expenses are covered by pensions, and they have great long-term care insurance. They are fully in "protect the principal" mode and no argument in the world will change their minds. They have also lived through a few market meltdowns at this point and have friends who are struggling to make ends meet (who also saved well, but were invested in riskier assets at the wrong time). It sucks for them, but they will end up taking 2.5% in jumbo CDs from a variety of banks to keep them FDIC insured. I don't see any alternative. Even if I could talk them back into equities (and there is no way in hell I could), dividend yields on the higher rated stocks are still 2-3% and they aren't going to be interested in anything riskier at this point in their lives. part of the problem is that retirement duration has gotten longer. the rule-of-thumb of being able to spend about 4% of your assets forever fails when we sit for a long time at an effective 0% fed funds rate. these days, retire at 65 and you may actually have a 30 year investing horizon still in front of you. if you look at it this way, the equity portion of ones retirement portfolio *should* be higher than what most retired folks are probably at, versus fixed income. but, i'm not 65 and were i it would probably take a metallic ballset to be (120-65)=55% invested in equities at this point in the market cycle. it's easy to talk big until it's *your* nest egg at risk. but 30 years is a fairly long investment horizon, and it should even out. that said, there was hella money made on the downslope of loosening credit -- and similarly, hella money made as investable funds were pulled out of debt and poured into equities. so, you could argue that today's "slack tide" situation -- while not very pleasant for folks on fixed income (as your examples demonstrate) -- comes after returns were well above norm for both the bond and stock markets. i know just a (dangerously) trivial bit about bonds in general and i have several funds that did very well while the fed was enumerating thru QE(x+1). my point being that crops were good for several years prior, and although the "slack tide" now is uncomfortable for many (high equity pricing, low bond yields, fed poised to do something but not yet) there should be a full pantry to cover this. ar-jedi |

|

|

|

[#24]

Quoted:

part of the problem is that retirement duration has gotten longer. the rule-of-thumb of being able to spend about 4% of your assets forever fails when we sit for a long time at an effective 0% fed funds rate. these days, retire at 65 and you may actually have a 30 year investing horizon still in front of you. if you look at it this way, the equity portion of ones retirement portfolio *should* be higher than what most retired folks are probably at, versus fixed income. but, i'm not 65 and were i it would probably take a metallic ballset to be (120-65)=55% invested in equities at this point in the market cycle. it's easy to talk big until it's *your* nest egg at risk. but 30 years is a fairly long investment horizon, and it should even out. that said, there was hella money made on the downslope of loosening credit -- and similarly, hella money made as investable funds were pulled out of debt and poured into equities. so, you could argue that today's "slack tide" situation -- while not very pleasant for folks on fixed income (as your examples demonstrate) -- comes after returns were well above norm for both the bond and stock markets. i know just a (dangerously) trivial bit about bonds in general and i have several funds that did very well while the fed was enumerating thru QE(x+1). my point being that crops were good for several years prior, and although the "slack tide" now is uncomfortable for many (high equity pricing, low bond yields, fed poised to do something but not yet) there should be a full pantry to cover this. ar-jedi Quoted:

Quoted:

I said three, but actually the two specific examples that I am thinking of are a couple of guys I used to help with their businesses. These are people that have done everything right - saved $1-2 million for retirement, changed their asset allocation from equities to fixed income as they got closer to retirement under the model that they were taught. They are now retired, and had all gone as planned would be making somewhere in the order of 4-5%. So, on $2 million that is $80-100k a year. Houses are paid for, a large portion of day-to-day living expenses are covered by pensions, and they have great long-term care insurance. They are fully in "protect the principal" mode and no argument in the world will change their minds. They have also lived through a few market meltdowns at this point and have friends who are struggling to make ends meet (who also saved well, but were invested in riskier assets at the wrong time). It sucks for them, but they will end up taking 2.5% in jumbo CDs from a variety of banks to keep them FDIC insured. I don't see any alternative. Even if I could talk them back into equities (and there is no way in hell I could), dividend yields on the higher rated stocks are still 2-3% and they aren't going to be interested in anything riskier at this point in their lives. part of the problem is that retirement duration has gotten longer. the rule-of-thumb of being able to spend about 4% of your assets forever fails when we sit for a long time at an effective 0% fed funds rate. these days, retire at 65 and you may actually have a 30 year investing horizon still in front of you. if you look at it this way, the equity portion of ones retirement portfolio *should* be higher than what most retired folks are probably at, versus fixed income. but, i'm not 65 and were i it would probably take a metallic ballset to be (120-65)=55% invested in equities at this point in the market cycle. it's easy to talk big until it's *your* nest egg at risk. but 30 years is a fairly long investment horizon, and it should even out. that said, there was hella money made on the downslope of loosening credit -- and similarly, hella money made as investable funds were pulled out of debt and poured into equities. so, you could argue that today's "slack tide" situation -- while not very pleasant for folks on fixed income (as your examples demonstrate) -- comes after returns were well above norm for both the bond and stock markets. i know just a (dangerously) trivial bit about bonds in general and i have several funds that did very well while the fed was enumerating thru QE(x+1). my point being that crops were good for several years prior, and although the "slack tide" now is uncomfortable for many (high equity pricing, low bond yields, fed poised to do something but not yet) there should be a full pantry to cover this. ar-jedi It's a mind set that people sometimes can't get out of. Like you said having a 0 rate environment is royally messing with people preconceived notions of "safe" investments and their ability to just sit on a CD and take a check off those funds. When those gentlemen buy their brokered cd's and then god forbid the Fed raise rates faster than the street anticipated (not saying its probable) are going to shit when their market values fall. Unless they don't care about security value, then if that's the case why are they in cd's. Like I said it's an interesting mind set. There are always many ways to make money in any market. people fail to forget than when capital is flowing out of one asset class it's moving into another. |

|

|

|

[#25]

Quoted:

Your clients not your BD right? They don't ever want the FDIC insured stuff? Lehman bros bit the BD I stared out at in the ass big time. Even worse than world com bit them. The worst part about lehman is you had an opportunity to get out and about 70-80% of par before they went belly up. Quoted:

Quoted:

Quoted:

Your Broker dealer doesn't offer structured products? They don't want the credit risk after Lehman Your clients not your BD right? They don't ever want the FDIC insured stuff? Lehman bros bit the BD I stared out at in the ass big time. Even worse than world com bit them. The worst part about lehman is you had an opportunity to get out and about 70-80% of par before they went belly up. Yeah, not BD. I'm not an investment advisor nor work with retail investors. That way I only lose my own money

|

|

|

|

[#26]

Quoted:

Yeah, not BD. I'm not an investment advisor nor work with retail investors. That way I only lose my own money Quoted:

Quoted:

Quoted:

Quoted:

Your Broker dealer doesn't offer structured products? They don't want the credit risk after Lehman Your clients not your BD right? They don't ever want the FDIC insured stuff? Lehman bros bit the BD I stared out at in the ass big time. Even worse than world com bit them. The worst part about lehman is you had an opportunity to get out and about 70-80% of par before they went belly up. Yeah, not BD. I'm not an investment advisor nor work with retail investors. That way I only lose my own money

|

|

|

|

[#27]

$1000 gets you roughly 125 pmags with a great potential of returning 5k plus during another scare/shortage.

|

|

|

|

[#28]

Quoted:

$1000 gets you roughly 125 pmags with a great potential of returning 5k plus during another scare/shortage. besides the fact that this approach doesn't scale well, you also run the risk of ending up with nothing. one piece of knee-jerk legislation and you are screwed. ar-jedi |

|

|

|

[#29]

On Black in Vegas one time!

|

|

|

|

[#30]

I just invested a grand into Alibaba today.. I think they're going places

|

|

|

|

[#31]

Quoted:

besides the fact that this approach doesn't scale well, you also run the risk of ending up with nothing. one piece of knee-jerk legislation and you are screwed. ar-jedi Quoted:

Quoted:

$1000 gets you roughly 125 pmags with a great potential of returning 5k plus during another scare/shortage. besides the fact that this approach doesn't scale well, you also run the risk of ending up with nothing. one piece of knee-jerk legislation and you are screwed. ar-jedi But hey, you still have mags

|

|

|

|

[#32]

Quoted:

Silver. +1 I think it is at or near the bottom and will start back up shortly. Plus it has intrinsic value and is pretty to look at. http://www.monex.com/why/silver_market.html?mm_campaign=10bf58103fac144eba889d05654978b4&keyword=silver%20prices&utm_source=Google&utm_medium=CPC&utm_campaign=non-branded&gclid=CjwKEAjwqamhBRDeyKKuuYztxwQSJAA1luvGi_bLa5FAiyTs4Y0DoeyCo2AyDPlU2WVVVHtXW6BCQRoCm6jw_wcB |

|

|

|

[#33]

Quoted:

I just invested a grand into Alibaba today.. I think they're going places I don't think this was wise..... |

|

|

|

[#34]

I already have the Roths set up and was looking for something to play with. Appreciate all the dialog that is going on. Looked at WM and Johnson and Johnson. This was more the answer I was looking for.

will look into some companies that I deal with or use. |

|

|

|

[#35]

Quoted:

I already have the Roths set up and was looking for something to play with. Appreciate all the dialog that is going on. Looked at WM and Johnson and Johnson. This was more the answer I was looking for. will look into some companies that I deal with or use. Utilities ETFs I'm in VPU. |

|

|

|

[#36]

Quoted:

I already have the Roths set up and was looking for something to play with. Quoted:

I already have the Roths set up and was looking for something to play with. stop "playing" with investment money when you are young! this is completely the wrong mentality. "playing" is not a mindset for investing. this is a mindset which will most likely result in you losing money, becoming discouraged, and then abandoning investing altogether. you need to change your mindset: you are not going to a casino to wager your hard-earned money and in the end lose it to the house; you are investing your hard-earned money so that it grows into a bigger pile, so you can buy a house, a horse, a Mustang GT, a Porsche, a Picasso, or just so you are financially comfortable with your feet in the sand/drink in your hand when you are 75. this is also one of the reason that doctors as a class are among the worst investors --> "if i lose X, i can make 10X later". here is your reply, i have taken the liberty to pre-craft it for you: That is good advice. Thank you. But, I'm just looking to "dabble" a bit with this and learn how stockpicking works. If I lose it, I lose it. No big deal. I learn best by doing it. I can read all the info I can handle, but I won't feel comfortable until I do it for myself. so, my suggestion is that take the $1000 that you are about to lose, and sign up for a couple of investing and personal finance classes at your local college/university. you will get far more out of this route than pissing away a healthy fraction of $1000 on random stocks. you worked hard for that money -- don't just piss it away. you'll feel A LOT better making 10% on your first investment than losing 50%, believe me. and, positive returns from your investments at an early age gains you the benefit of compounded interest etc.; see my example above for what $1000 per year is worth in your twilight years. don't ever consider any money PLAY or TRASH MONEY. if you want to throw it away, send it to me or donate it to charity. again, do not "play" in the stock market. this is a mental mistake. equity markets are a brutal, zero-sum game in which you will be competing against others with YOUR money. don't treat your hard-earned savings by "playing" with it -- put it to work. ar-jedi |

|

|

|

[#37]

Quoted:

Get in on a cattle future. $2k investement made $40k Yeah, but he's not the Hildebeast. Take $12 of it and invest in this, then act accordingly. |

|

|

|

[#38]

Silver and ar15 mags

Gr |

|

|

|

[#39]

Natural Gas.

- Antero Natural Resources (currently the #1 energy company fracking the most wells in WV and Pa right now) they are hitting it big no signs of slowing down, blowing up big time, their stock is only going north. |

|

|

|

[#40]

GOOGLE

|

|

|

|

[#41]

gun stock like Olin or ATK

or do a drip - look at the ones that wells fargo will manage for you. all kinds of good to be had. I own about 105 shares of FNF (kind of like buffet - I like insurance companies). bought in when it was running 14 bucks a share in the bottom of the down turn - now in the high twentys so I have doubled my money - the dividends are paying me at a rate of 6 percent on my orginal money - so do something and keep doing something. Red

|

|

|

|

[#42]

You can't diversify with only $1,000. If you invested in a single stock -- any stock -- the risk would be unacceptably high.

You need at least $100 K for a decent diversified portfolio. Mutual funds are no answer because they kill you with fees. I have a nice basket of about 16 different stocks, and I've done quite well over the last couple of years. But I'm getting nervous. We may be coming to the end of a bull market. Honestly, I would stay out of stocks at the moment (if you are not already in the market). Keep your powder dry, and wait for better opportunities. |

|

|

|

[#43]

Quoted:

You can't diversify with only $1,000. If you invested in a single stock -- any stock -- the risk would be unacceptably high. You need at least $100 K for a decent diversified portfolio. Mutual funds are no answer because they kill you with fees. I have a nice basket of about 16 different stocks, and I've done quite well over the last couple of years. But I'm getting nervous. We may be coming to the end of a bull market. Honestly, I would stay out of stocks at the moment (if you are not already in the market). Keep your powder dry, and wait for better opportunities. Where are you pulling that number out of the air from, 100k? Studies have shown that 20-30 individual stocks will reduce systematic to were adding any more individual stocks to that portfolio you are marginally reducing that risk. Not to mention do you know what ETF's are? They are a modern portfolio theorist's dream security. |

|

|

|

[#44]

Quoted:

this is also one of the reason that doctors as a class are among the worst investors --> "if i lose X, i can make 10X later". ar-jedi That's why I regret not taking the MCAT and going to medical school, apparently they teach a course in med school that makes all doctors investing wizards. I really wish they would have that class available for me to take.

|

|

|

|

[#45]

Quoted:

That's why I regret not taking the MCAT and going to medical school, apparently they teach a course in med school that makes all doctors investing wizards. I really wish they would have that class available for me to take.

Quoted:

Quoted:

this is also one of the reason that doctors as a class are among the worst investors --> "if i lose X, i can make 10X later". That's why I regret not taking the MCAT and going to medical school, apparently they teach a course in med school that makes all doctors investing wizards. I really wish they would have that class available for me to take.

overconfidence in skill transference PLUS very high income make for a very dangerous couple. "i am an accomplished surgeon, among the best in my field. what i do is hella complicated and requires extraordinary aptitude, hence the very few of us who can do it. in contrast, investing is not that complicated -- millions of people do it. however, i'm a very smart guy so i can expect great performance from my investment selections. and, since i'm making US$400K per annum, even if i screw up a $50K position, i can earn that back in 6 weeks. but anyway, 4 of the doctors in my practice are going to pool our money and buy an apartment complex. now then i don't know jack about running an apartment complex but i aced medical school and running an apartment complex can't be that hard since people with high school diplomas do it regularly. one partner in my practice says we should net about 40% over expenses per year on this investment." boom. ar-jedi |

|

|

|

[#46]

Quoted:

overconfidence in skill transference PLUS very high income make for a very dangerous couple. "i am an accomplished surgeon, among the best in my field. what i do is hella complicated and requires extraordinary aptitude, hence the very few of us who can do it. in contrast, investing is not that complicated -- millions of people do it. however, i'm a very smart guy so i can expect great performance from my investment selections. and, since i'm making US$400K per annum, even if i screw up a $50K position, i can earn that back in 6 weeks. but anyway, 4 of the doctors in my practice are going to pool our money and buy an apartment complex. now then i don't know jack about running an apartment complex but i aced medical school and running an apartment complex can't be that hard since people with high school diplomas do it regularly. one partner in my practice says we should net about 40% over expenses per year on this investment." boom. ar-jedi Quoted:

Quoted:

Quoted:

this is also one of the reason that doctors as a class are among the worst investors --> "if i lose X, i can make 10X later". That's why I regret not taking the MCAT and going to medical school, apparently they teach a course in med school that makes all doctors investing wizards. I really wish they would have that class available for me to take.

overconfidence in skill transference PLUS very high income make for a very dangerous couple. "i am an accomplished surgeon, among the best in my field. what i do is hella complicated and requires extraordinary aptitude, hence the very few of us who can do it. in contrast, investing is not that complicated -- millions of people do it. however, i'm a very smart guy so i can expect great performance from my investment selections. and, since i'm making US$400K per annum, even if i screw up a $50K position, i can earn that back in 6 weeks. but anyway, 4 of the doctors in my practice are going to pool our money and buy an apartment complex. now then i don't know jack about running an apartment complex but i aced medical school and running an apartment complex can't be that hard since people with high school diplomas do it regularly. one partner in my practice says we should net about 40% over expenses per year on this investment." boom. ar-jedi

|

|

|

|

[#47]

Ammo or mags. Make guaranteed payout. If the value doesn't go up you still have a hard asset. If value does go up in a year or two sell and then wait to reinvest.

|

|

|

|

[#48]

Quoted:

overconfidence in skill transference PLUS very high income make for a very dangerous couple. "i am an accomplished surgeon, among the best in my field. what i do is hella complicated and requires extraordinary aptitude, hence the very few of us who can do it. in contrast, investing is not that complicated -- millions of people do it. however, i'm a very smart guy so i can expect great performance from my investment selections. and, since i'm making US$400K per annum, even if i screw up a $50K position, i can earn that back in 6 weeks. but anyway, 4 of the doctors in my practice are going to pool our money and buy an apartment complex. now then i don't know jack about running an apartment complex but i aced medical school and running an apartment complex can't be that hard since people with high school diplomas do it regularly. one partner in my practice says we should net about 40% over expenses per year on this investment." boom. ar-jedi Quoted:

Quoted:

Quoted:

this is also one of the reason that doctors as a class are among the worst investors --> "if i lose X, i can make 10X later". That's why I regret not taking the MCAT and going to medical school, apparently they teach a course in med school that makes all doctors investing wizards. I really wish they would have that class available for me to take.

overconfidence in skill transference PLUS very high income make for a very dangerous couple. "i am an accomplished surgeon, among the best in my field. what i do is hella complicated and requires extraordinary aptitude, hence the very few of us who can do it. in contrast, investing is not that complicated -- millions of people do it. however, i'm a very smart guy so i can expect great performance from my investment selections. and, since i'm making US$400K per annum, even if i screw up a $50K position, i can earn that back in 6 weeks. but anyway, 4 of the doctors in my practice are going to pool our money and buy an apartment complex. now then i don't know jack about running an apartment complex but i aced medical school and running an apartment complex can't be that hard since people with high school diplomas do it regularly. one partner in my practice says we should net about 40% over expenses per year on this investment." boom. ar-jedi haha, brilliant.. Unfortunately, this has triggered my ptsd and skeletons are flying out of the closet. Won't sleep for a week. I used to work at a hedge fund that had raised all of its money from local doctors. It was market neutral but the number of times I had to listen to some shrill surgeon yelling at me that "my partner's Ameritrade account was up 5% this week and why the hell did I gain less than 1% that week, and what the f*ck was wrong with you, why did I ever give you my money, why do I have to wait three months to pull it out and put it in my own Ameritrade account" has scarred me for life. I also never got a thank you on weeks the market tanked and they lost nothing

|

|

|

|

[#49]

Quoted:

haha, brilliant.. Unfortunately, this has triggered my ptsd and skeletons are flying out of the closet. Won't sleep for a week. I used to work at a hedge fund that had raised all of its money from local doctors. It was market neutral but the number of times I had to listen to some shrill surgeon yelling at me that "my partner's Ameritrade account was up 5% this week and why the hell did I gain less than 1% that week, and what the f*ck was wrong with you, why did I ever give you my money, why do I have to wait three months to pull it out and put it in my own Ameritrade account" has scarred me for life. I also never got a thank you on weeks the market tanked and they lost nothing Quoted:

Quoted:

Quoted:

Quoted:

this is also one of the reason that doctors as a class are among the worst investors --> "if i lose X, i can make 10X later". That's why I regret not taking the MCAT and going to medical school, apparently they teach a course in med school that makes all doctors investing wizards. I really wish they would have that class available for me to take.

overconfidence in skill transference PLUS very high income make for a very dangerous couple. "i am an accomplished surgeon, among the best in my field. what i do is hella complicated and requires extraordinary aptitude, hence the very few of us who can do it. in contrast, investing is not that complicated -- millions of people do it. however, i'm a very smart guy so i can expect great performance from my investment selections. and, since i'm making US$400K per annum, even if i screw up a $50K position, i can earn that back in 6 weeks. but anyway, 4 of the doctors in my practice are going to pool our money and buy an apartment complex. now then i don't know jack about running an apartment complex but i aced medical school and running an apartment complex can't be that hard since people with high school diplomas do it regularly. one partner in my practice says we should net about 40% over expenses per year on this investment." boom. ar-jedi haha, brilliant.. Unfortunately, this has triggered my ptsd and skeletons are flying out of the closet. Won't sleep for a week. I used to work at a hedge fund that had raised all of its money from local doctors. It was market neutral but the number of times I had to listen to some shrill surgeon yelling at me that "my partner's Ameritrade account was up 5% this week and why the hell did I gain less than 1% that week, and what the f*ck was wrong with you, why did I ever give you my money, why do I have to wait three months to pull it out and put it in my own Ameritrade account" has scarred me for life. I also never got a thank you on weeks the market tanked and they lost nothing Everyone looks like a mogul when it's a bull market. From your bank broker, insurance agent, to your day trader. 999, there is a placed saved for you up above.

god forbid they have a friend who really trades in their "TD Ameritrade" account and occasionally picks a real winner. That's all they hear from the friend is how they bought XYZ Pharmaceuticals and made 500% return in 3 months. The friend never tells them about their other holdings which got taken to the cleaners.

|

|

|

|

[#50]

Quoted:

Everyone looks like a mogul when it's a bull market. From your bank broker, insurance agent, to your day trader. 999, there is a placed saved for you up above.

god forbid they have a friend who really trades in their "TD Ameritrade" account and occasionally picks a real winner. That's all they hear from the friend is how they bought XYZ Pharmaceuticals and made 500% return in 3 months. The friend never tells them about their other holdings which got taken to the cleaners.

Quoted:

Quoted:

Quoted:

Quoted:

Quoted:

this is also one of the reason that doctors as a class are among the worst investors --> "if i lose X, i can make 10X later". That's why I regret not taking the MCAT and going to medical school, apparently they teach a course in med school that makes all doctors investing wizards. I really wish they would have that class available for me to take.

overconfidence in skill transference PLUS very high income make for a very dangerous couple. "i am an accomplished surgeon, among the best in my field. what i do is hella complicated and requires extraordinary aptitude, hence the very few of us who can do it. in contrast, investing is not that complicated -- millions of people do it. however, i'm a very smart guy so i can expect great performance from my investment selections. and, since i'm making US$400K per annum, even if i screw up a $50K position, i can earn that back in 6 weeks. but anyway, 4 of the doctors in my practice are going to pool our money and buy an apartment complex. now then i don't know jack about running an apartment complex but i aced medical school and running an apartment complex can't be that hard since people with high school diplomas do it regularly. one partner in my practice says we should net about 40% over expenses per year on this investment." boom. ar-jedi haha, brilliant.. Unfortunately, this has triggered my ptsd and skeletons are flying out of the closet. Won't sleep for a week. I used to work at a hedge fund that had raised all of its money from local doctors. It was market neutral but the number of times I had to listen to some shrill surgeon yelling at me that "my partner's Ameritrade account was up 5% this week and why the hell did I gain less than 1% that week, and what the f*ck was wrong with you, why did I ever give you my money, why do I have to wait three months to pull it out and put it in my own Ameritrade account" has scarred me for life. I also never got a thank you on weeks the market tanked and they lost nothing Everyone looks like a mogul when it's a bull market. From your bank broker, insurance agent, to your day trader. 999, there is a placed saved for you up above.

god forbid they have a friend who really trades in their "TD Ameritrade" account and occasionally picks a real winner. That's all they hear from the friend is how they bought XYZ Pharmaceuticals and made 500% return in 3 months. The friend never tells them about their other holdings which got taken to the cleaners.

I think working with retail investors would be a difficult job. They are alway geniuses when the market goes up and their advisor is always at fault when it goes down. Have had a few weak moments when I think I would like to help people and then I remind myself of this and realize it's not for me. |

|

|

Win a FREE Membership!

Win a FREE Membership!

Sign up for the ARFCOM weekly newsletter and be entered to win a free ARFCOM membership. One new winner* is announced every week!

You will receive an email every Friday morning featuring the latest chatter from the hottest topics, breaking news surrounding legislation, as well as exclusive deals only available to ARFCOM email subscribers.

AR15.COM is the world's largest firearm community and is a gathering place for firearm enthusiasts of all types.

From hunters and military members, to competition shooters and general firearm enthusiasts, we welcome anyone who values and respects the way of the firearm.

Subscribe to our monthly Newsletter to receive firearm news, product discounts from your favorite Industry Partners, and more.

Copyright © 1996-2024 AR15.COM LLC. All Rights Reserved.

Any use of this content without express written consent is prohibited.

AR15.Com reserves the right to overwrite or replace any affiliate, commercial, or monetizable links, posted by users, with our own.