|

Posted: 2/14/2013 9:23:15 PM EDT

In particular, I have no idea how to put axes on all sides of the graph to form the "box." I see screen shots of excel graphs of edgeworth boxes on google, so I know it can be done, but they do not explain how to do it.

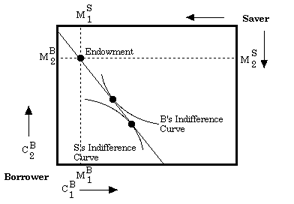

I want to make a graph that looks like this.    If anyone knows how I can make these kinds of axes, I'd greatly appreciate it before I brute force it with multiple graphs in photoshop.  |

|

|

|

[#1]

bump

|

|

|

|

[#2]

You could use the Cobb-Douglas production functions as a simple example:

(1) C = ALCaTC1-a and (1’) F = BLFbTF1-b, where C(F) is the quantity of clothing (food) being produced, LC(LF) is the quantity of labour employed in cloth (food) production, and TC(TF) is the quantity of land employed in cloth (food) production. The coefficient A(B) is a positive constant reflecting technology. First, define the unit isoquants, showing the amount of land used given the employment of labour in producing each unit of cloth (food). These are: (2) TC = [A-1LC-a]1/(1-a) and (2’) TF = [B-1LF-b]1/(1-b) .(1) The first-order conditions, coupled with linear homogeneity, allow the derivation of lines that show factor price ratios that are consistent with various input combinations. Following Krugman and Obstfeld, these are denoted as CC and FF respectively. The equation for the line CC (the cloth industry's expansion path) is: (3) r = (1/a-1)(LC/TC)w , where w is the wage rate (payment per unit of labour) and r is the rental rate (per unit of land). The corresponding FF line, similarly defined, is: (3’) r = (1/b-1)(LF/TF)w. So far, the model transforms the expansion paths in the two industries into equations involving factor prices in each of the two industries. To move closer to closing the model requires that product prices be related to the information above. This is accomplished by imposing equilibrium conditions for competitive markets, that price equals marginal cost (MC) in each industry. Since MC = w/MPL in each industry, this imposition implies the following: (4) PC = w(Aa)-1(1/a-1)a-1(w/r)a-1 and (4’) PF = w(Bb)-1(1/b-1)b-1(w/r)b-1. These two equations provide this critical relationship between the ratio of input prices and that of product prices: (5) (w/r) = [Aa(1/a-1)1-a(Bb-1)-1(1/b-1)b-1(PC/PF)]1/(a-b). Determining how much labour and land are used in each of the two industries can now close the model. The expansion paths give the key to this determination. (6) TC = (w/r)(1/(a-1))LC and (6’) TF = (w/r)(1/(b-1))LF. But, LF = L-LC and TF = T-TC. Appropriate substitution allows TC and TF to be stated as a linear function of LC. The resulting equations are: (7) TC = kLC and (7') TF = mL-mLC where k=(w/r)(1-a)/a and m = (w/r)(1-b)/b. |

|

|

|

[#3]

Why are you doing an Edgeworth? Someone wants to show whats "fair" instead of Pareto efficent?

|

|

|

|

[#4]

I figured out a decent looking solution by just using lines for the other edges. I used Cobb-Douglas functions to illustrate the point.

My primary study strategy is rewriting notes. I've been taking it one step further by typing them in LaTex after rewriting them. We just finished general equilibrium theory and are moving on to game theory, which will be a little harder to represent in excel.  ETA: My professor called the 1st welfare theorem the Republican welfare theorem, and the second welfare theorem the Democratic welfare theorem. While I don't think it helped the Chinese students too much, it certainly helped me memorize them on the spot.  |

|

|

|

[#5]

I tried to help out, look what I found

|

|

|

Win a FREE Membership!

Win a FREE Membership!

Sign up for the ARFCOM weekly newsletter and be entered to win a free ARFCOM membership. One new winner* is announced every week!

You will receive an email every Friday morning featuring the latest chatter from the hottest topics, breaking news surrounding legislation, as well as exclusive deals only available to ARFCOM email subscribers.

AR15.COM is the world's largest firearm community and is a gathering place for firearm enthusiasts of all types.

From hunters and military members, to competition shooters and general firearm enthusiasts, we welcome anyone who values and respects the way of the firearm.

Subscribe to our monthly Newsletter to receive firearm news, product discounts from your favorite Industry Partners, and more.

Copyright © 1996-2024 AR15.COM LLC. All Rights Reserved.

Any use of this content without express written consent is prohibited.

AR15.Com reserves the right to overwrite or replace any affiliate, commercial, or monetizable links, posted by users, with our own.