|

[#1]

You definitely could do a lot worse than a vanguard target date fund. It sounds like you aren't especially interested in being able to handle something more complex on your own, and the worst thing you can do is go with high expense alternatives.

I've been thinking about paying an advisory group to manage it. Don't do that. |

|

|

|

[#2]

If you don't have the time to manage it yourself a target fund is not a bad idea. It takes out the guesswork.

|

|

|

|

[#3]

Quoted: If you don't have the time to manage it yourself a target fund is not a bad idea. It takes out the guesswork. |

|

|

|

[#4]

Make sure you are OK with the loads. If you are planning on keeping it there get the A share. Probably 4.5% front end but some have a back end load where it takes 1% when you sell shares.

|

|

|

|

[#5]

It depends on what your available choices are.

Don't pay advisory fees, that's not necessary, a target fund will be a much better choice. Compared to 2014, so far 2015 has been quite boring - but keep in mind 2014 was a good year. |

|

|

|

[#6]

My Vanguard Target Fund has me happy....Vanguard is good to go in my opinion

they are fairly consistent at outperforming the industry |

|

|

|

[#7]

Thanks for the replies! I'll move everything to the Vanguard 2030.

Quoted:

You definitely could do a lot worse than a vanguard target date fund. It sounds like you aren't especially interested in being able to handle something more complex on your own, and the worst thing you can do is go with high expense alternatives. Don't do that. Quoted:

You definitely could do a lot worse than a vanguard target date fund. It sounds like you aren't especially interested in being able to handle something more complex on your own, and the worst thing you can do is go with high expense alternatives. I've been thinking about paying an advisory group to manage it. Don't do that. It's more that I do not feel qualified to handle the 401k management on my own. I do not know nearly enough about investing and the cost of failure is too great. Just curious, why not the advisory group? Not worth the expense? Quoted:

Make sure you are OK with the loads. If you are planning on keeping it there get the A share. Probably 4.5% front end but some have a back end load where it takes 1% when you sell shares. I'm honestly not quite sure what that means, the cost to move from one fund to another? The fees will be less than what I'm paying now. I'll make the transaction through their website. Hopefully it'll let me know about any fees associated with the move. |

|

|

|

[#8]

The Target fund is fine and can be tweaked based on how aggressive you want to be.

Instead of using the 2030 you could do 2040 or 2050 if wanting to be more aggressive or 2025 to be more conservative. |

|

|

|

[#9]

A 4.5 percent load means when you purchase they take 4.5 percent as a fee. Over the years it works back up but at the start you will be down 4.5.

Some funds give a discount if you buy large amounts. The back end load charges 1 percent on your withdrawal so if you have a huge return this may not be desirable. But yes the website should lay all the transaction details for you to see

|

|

|

|

[#10]

Also once you are in the vanguard family of funds you should be able to move from one fund to another without another load charge. If you wanted to start more aggressive and then go more conservative faster than the one target fund.

I would second the opinion to not go with the advisory thing |

|

|

|

[#11]

Quoted:

Make sure you are OK with the loads. If you are planning on keeping it there get the A share. Probably 4.5% front end but some have a back end load where it takes 1% when you sell shares. Where are you seeing there is a load on the funds he is discussing? VTHRX M* Yes, you are correct that he should be aware of all fees while choosing his fund, but the fund he mentioned has no load. |

|

|

|

[#12]

I don't know what they are just an example. They may have no load

Eta , you are right. His brokerage may charge a no load transaction fee. I know mine would be 50 bucks. |

|

|

|

[#13]

Vanguard funds are no load. No transaction fee either if your account is at vanguard.

|

|

|

|

[#14]

Quoted:

Quoted:

Make sure you are OK with the loads. If you are planning on keeping it there get the A share. Probably 4.5% front end but some have a back end load where it takes 1% when you sell shares. Where are you seeing there is a load on the funds he is discussing? VTHRX M* Yes, you are correct that he should be aware of all fees while choosing his fund, but the fund he mentioned has no load. He is discussing buying a Vanguard fund through a Fidelity account - the load and expense numbers found on M* mean nothing without first referencing the materials from Fidelity, who could add those things. |

|

|

|

[#15]

Loads aside, several articles I've read indicate that the "Target" funds run a bit conservative in their investments. If you're willing to take on more investment risk then pick a target fund with a later year. I selected one with a date about 15 years after I plan to retire, but only because I have other investments that are safer so I can afford to take more risk with that one.

If Fidelity is offering a Vanguard fund as an investment vehicle through their own 401k then there shouldn't be much of a load. OP can check. Full disclosure my personal investments and my IRA are both at Vanguard, my company's 401k is at Fidelity and it only offers Fidelity funds. |

|

|

|

[#16]

Quoted:

He is discussing buying a Vanguard fund through a Fidelity account - the load and expense numbers found on M* mean nothing without first referencing the materials from Fidelity, who could add those things. Quoted:

Quoted:

Quoted:

Make sure you are OK with the loads. If you are planning on keeping it there get the A share. Probably 4.5% front end but some have a back end load where it takes 1% when you sell shares. Where are you seeing there is a load on the funds he is discussing? VTHRX M* Yes, you are correct that he should be aware of all fees while choosing his fund, but the fund he mentioned has no load. He is discussing buying a Vanguard fund through a Fidelity account - the load and expense numbers found on M* mean nothing without first referencing the materials from Fidelity, who could add those things. Good catch and very poor reading comprehension on my part. That $75 transaction fee from Fido is annoying. I tend to save my Vanguard Account for any funds that I am desperate to own with a transaction fee. $20 fee with Vanguard or $75 with Fidelity, it's a no brainer if the purchase options are the same and you can deal with the inconvenience of a couple different account. Of course, if he bought this fund directly from Vanguard, there would be no fee. |

|

|

|

[#17]

Quoted:

The Target fund is fine and can be tweaked based on how aggressive you want to be. Instead of using the 2030 you could do 2040 or 2050 if wanting to be more aggressive or 2025 to be more conservative. I keep trying to explain this to people, but I really don't think a single one has understood me yet. I admit that I am not the greatest teacher in the world, but I guess I will keep on trying. |

|

|

|

[#18]

Quoted:

The Target fund is fine and can be tweaked based on how aggressive you want to be. Instead of using the 2030 you could do 2040 or 2050 if wanting to be more aggressive or 2025 to be more conservative. And depending on what your risk tolerance is, and what else you may know, that might be a good idea. For instance, if you have something else conservative - push it out, get more aggressive. |

|

|

|

[#19]

I initiated the switch today and called to make sure that there's no transaction fees involved. She assured me there isn't any.

Quoted:

Quoted:

The Target fund is fine and can be tweaked based on how aggressive you want to be. Instead of using the 2030 you could do 2040 or 2050 if wanting to be more aggressive or 2025 to be more conservative. I keep trying to explain this to people, but I really don't think a single one has understood me yet. I admit that I am not the greatest teacher in the world, but I guess I will keep on trying. This makes sense to me. I went with 50% in the 2030 and 50% in 2045. |

|

|

|

[#20]

Sounds like a good choice to me, though we won't know for sure for another 15 years.

Congratulations. Since you are making decisions like this on your own, I don't think you need a financial adviser. Which saves a lot of money all by itself. |

|

|

|

[#21]

These target funds are funds of funds so If you look into their holdings you can get an idea where they invest the money. These are the 4 funds your fund holds Vanguard Total Stock Market Index Fund Investor Shares Vanguard Total International Stock Index Fund Investor Shares Vanguard Total Bond Market II Index Fund Investor Shares* Vanguard Total International Bond Index Fund Investor Shares so take the first one which makes up 48% of the portfolio and look up the symbol VTSMX the top holdings are

|

||||||||||||||||||||||||||||

|

|

|

[#22]

Instead of using a target fund, use equivalent ETFs to match the target fund you want and rebalance yourself.

Vanguard's ETF expense ratios are very low... like .05% |

|

|

|

[#23]

Quoted:

Instead of using a target fund, use equivalent ETFs to match the target fund you want and rebalance yourself. Vanguard's ETF expense ratios are very low... like .05% While I agree that this is good advice, let's give the guy a break. After a couple of years, he might be ready for that. People need to learn to crawl before they learn to walk, let alone run. He is now on the right path. |

|

|

|

[#24]

Hard to go wrong with the Vanguard Target Retirement. I use them for my, as well as my children's, retirement funds.

|

|

|

|

[#25]

"why not the advisory group? Not worth the expense?"

Correct. |

|

|

|

[#26]

Quoted:

I spoke with a rep from Fidelity and he recommended that I put everything in the Vanguard Target Fund 2030. The part that I'm confused about is why is a Fidelity rep pushing a Vanguard Target Fund, when Fidelity has their own Target funds, or Spartan funds which are similar to Vanguard's low cost/expense mutual funds and ETFs? |

|

|

|

[#27]

If you want to "load your own" so to speak, take a look at this article.

|

|

|

|

[#28]

Quoted:

The part that I'm confused about is why is a Fidelity rep pushing a Vanguard Target Fund, when Fidelity has their own Target funds, or Spartan funds which are similar to Vanguard's low cost/expense mutual funds and ETFs? Quoted:

Quoted:

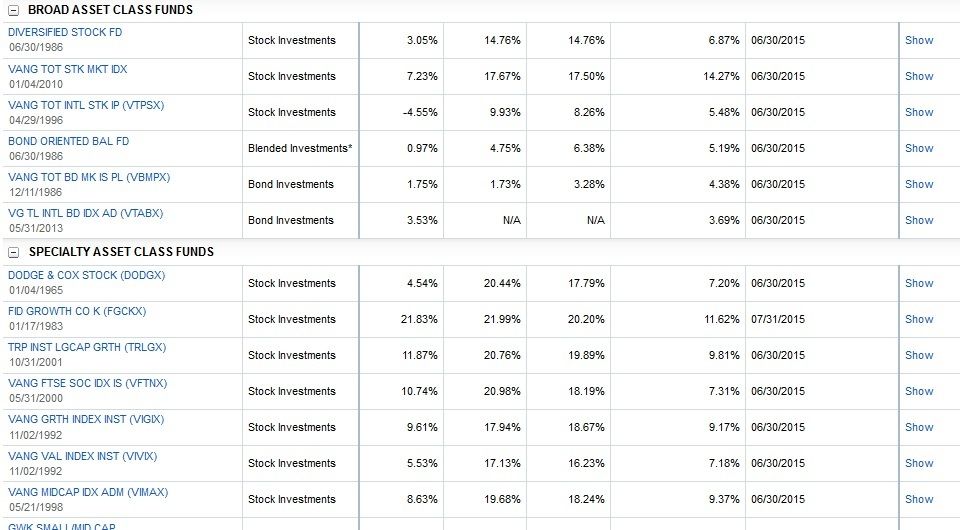

I spoke with a rep from Fidelity and he recommended that I put everything in the Vanguard Target Fund 2030. The part that I'm confused about is why is a Fidelity rep pushing a Vanguard Target Fund, when Fidelity has their own Target funds, or Spartan funds which are similar to Vanguard's low cost/expense mutual funds and ETFs? Now that you mention it, the Fidelity funds aren't even available with my 401K. Here are my choices:

|

|

|

|

[#29]

My work 401k is thru paychex and the vanguard funds just became available. So I allocated 40 percent to it. They do have a low expense ratio.

A lot of the work 401k your kind of stuck with the funds they offer |

|

|

|

[#30]

|

|

|

|

[#31]

I'm with Fidelity and I have been following this thread. I also noticed not so great performance of my ROTH IRA, so I'm thinking about jumping to this Vanguard deal you're talking about.

|

|

|

|

[#32]

What is the upside on not going through Vanguard to get one of their funds?

Why not do it directly? |

|

|

|

[#33]

That's my question, as well.

|

|

|

|

[#34]

I have chase as my brokerage and they charge a transaction fee to buy a vanguard no load fund

|

|

|

|

[#35]

Quoted:

I have chase as my brokerage and they charge a transaction fee to buy a vanguard no load fund Did you look into buying directly through Vanguard? |

|

|

|

[#36]

Quoted: Did you look into buying directly through Vanguard? Quoted: Quoted: I have chase as my brokerage and they charge a transaction fee to buy a vanguard no load fund Did you look into buying directly through Vanguard? |

|

|

|

[#37]

I setup my Vanguard 2045 Target fund earlier this April. I am 28 years old. I just plan on contributing the max every year. How do I know exactly what stocks/mutual funds they are using though? And ensure they are the best? VTIX is the ticker symbol for everything.

|

|

|

|

[#38]

Quoted: I setup my Vanguard 2045 Target fund earlier this April. I am 28 years old. I just plan on contributing the max every year. How do I know exactly what stocks/mutual funds they are using though? And ensure they are the best? VTIX is the ticker symbol for everything. On their site you can see what stocks are in the fund and how many shares of each. Vtix probably has 4 or 5 other vanguard funds in it. Searching those tickers you cand find the stocks they own ETA the 4 funds

|

||||||||||||

|

|

|

[#39]

Quoted:

On the first page of this thread there are links to take you to vanguards site. I think I posted one for the op of this thread. You need to search the ticker for the funds in the 2045 fund On their site you can see what stocks are in the fund and how many shares of each. Vtix probably has 4 or 5 other vanguard funds in it. Searching those tickers you cand find the stocks they own Quoted:

Quoted:

I setup my Vanguard 2045 Target fund earlier this April. I am 28 years old. I just plan on contributing the max every year. How do I know exactly what stocks/mutual funds they are using though? And ensure they are the best? VTIX is the ticker symbol for everything. Vtix probably has 4 or 5 other vanguard funds in it. Searching those tickers you cand find the stocks they own Alright so I think I did this correctly?

|

|

|

|

[#40]

Yes

|

|

|

|

[#41]

So should I keep buying into those?

|

|

|

|

[#42]

I have my work 401k buying 40 %the vanguard 2050 so it will be a little more aggressive. 30 % of an aggressive growth fund and 30% of a dividend fund. I don't have many choices other than what they provide.

My Roth I have taken more individual stocks but had 15 years of saving and the recovery from 08 tobgive me some money to work with.

I would. If You buy stocks over and over without a good chunk of money commissions would eat too much of your account. You could also buy the individual funds if you like. They have index funds which mirror the sp 500 for example. So your portfolio would go up and down with the sp 500 index. Vanguard has low fees and no loads which is good |

|

|

|

[#43]

Is there any chance to change my 2045 to a 2050 so I get more aggressive? I prob should have shot for a 2050 or 2055 to begin with.

|

|

|

|

[#44]

You should be able to exchange funds or even buy half and half if you wanted.

|

|

|

|

[#45]

Quoted:

My Vanguard Target Fund has me happy....Vanguard is good to go in my opinion they are fairly consistent at outperforming the industry My Vanguard Target 2035 fund has been doing well. I put a 401K rollover from a previous employer in it back in 2006. My employer just started offering a Vanguard Target fund for our 401K and I went with that. Think it's Target 2040 for me. |

|

|

Win a FREE Membership!

Win a FREE Membership!

Sign up for the ARFCOM weekly newsletter and be entered to win a free ARFCOM membership. One new winner* is announced every week!

You will receive an email every Friday morning featuring the latest chatter from the hottest topics, breaking news surrounding legislation, as well as exclusive deals only available to ARFCOM email subscribers.

AR15.COM is the world's largest firearm community and is a gathering place for firearm enthusiasts of all types.

From hunters and military members, to competition shooters and general firearm enthusiasts, we welcome anyone who values and respects the way of the firearm.

Subscribe to our monthly Newsletter to receive firearm news, product discounts from your favorite Industry Partners, and more.

Copyright © 1996-2024 AR15.COM LLC. All Rights Reserved.

Any use of this content without express written consent is prohibited.

AR15.Com reserves the right to overwrite or replace any affiliate, commercial, or monetizable links, posted by users, with our own.