|

Posted: 4/24/2015 11:24:36 AM EDT

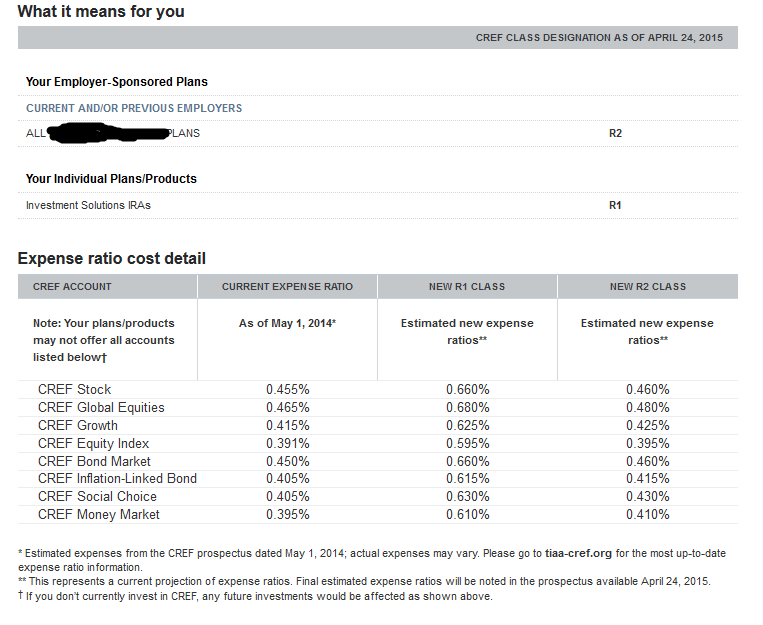

I have a 403(b) and Roth IRA with TIAA-CREF. Apparently they are raising their expense ratios (what I would consider to be fairly significantly)

I can rollover the 403(b) into Fidelity if I want to, but I don't have any experience with Fidelity or know if their expense ratios are better, worse, the same, etc . . . Thoughts?

|

|

|

|

[#1]

Fidelity has been around a long time.

you need to compare there expense ratios before deciding. |

|

|

|

[#2]

Vanguard has very low if not the lowest expense ratios in the industry.

And yes, by rolling over to Vanguard, Fidelity or whomever you choose, you can create an essentially identical portfolio with much lower costs. The management fee for Vanguard's S&P500 ETF, for example, is 0.05%. Most are in the 0.10-0.15% range. |

|

|

|

[#3]

Edit: Nevermind. I see a better explanation above.

|

|

|

|

[#4]

Quoted:

Vanguard has very low if not the lowest expense ratios in the industry. And yes, by rolling over to Vanguard, Fidelity or whomever you choose, you can create an essentially identical portfolio with much lower costs. The management fee for Vanguard's S&P500 ETF, for example, is 0.05%. Most are in the 0.10-0.15% range. Wow, that's outstanding. Part of the problem for me though is that the only other vendor I can roll my 403(b) into is Fidelity. I think I can transfer the IRA anywhere I want because it's not a part of the plan. I'll have to look at Vanguard; those expense ratios are unbelievable. I'm reading through the Bogleheads' Guide to Investing right now, and their info on index funds and expense ratios has been very illuminating. |

|

|

|

[#5]

Quoted:

Wow, that's outstanding. Part of the problem for me though is that the only other vendor I can roll my 403(b) into is Fidelity. I think I can transfer the IRA anywhere I want because it's not a part of the plan. I'll have to look at Vanguard; those expense ratios are unbelievable. I'm reading through the Bogleheads' Guide to Investing right now, and their info on index funds and expense ratios has been very illuminating. Quoted:

Quoted:

Vanguard has very low if not the lowest expense ratios in the industry. And yes, by rolling over to Vanguard, Fidelity or whomever you choose, you can create an essentially identical portfolio with much lower costs. The management fee for Vanguard's S&P500 ETF, for example, is 0.05%. Most are in the 0.10-0.15% range. Wow, that's outstanding. Part of the problem for me though is that the only other vendor I can roll my 403(b) into is Fidelity. I think I can transfer the IRA anywhere I want because it's not a part of the plan. I'll have to look at Vanguard; those expense ratios are unbelievable. I'm reading through the Bogleheads' Guide to Investing right now, and their info on index funds and expense ratios has been very illuminating. ETF's typically have lower expense ratios than mutual funds. Your expense ratios look a bit high to me for index funds. |

|

|

|

[#6]

Quoted:

ETF's typically have lower expense ratios than mutual funds. Your expense ratios look a bit high to me for index funds. Quoted:

Quoted:

Quoted:

Vanguard has very low if not the lowest expense ratios in the industry. And yes, by rolling over to Vanguard, Fidelity or whomever you choose, you can create an essentially identical portfolio with much lower costs. The management fee for Vanguard's S&P500 ETF, for example, is 0.05%. Most are in the 0.10-0.15% range. Wow, that's outstanding. Part of the problem for me though is that the only other vendor I can roll my 403(b) into is Fidelity. I think I can transfer the IRA anywhere I want because it's not a part of the plan. I'll have to look at Vanguard; those expense ratios are unbelievable. I'm reading through the Bogleheads' Guide to Investing right now, and their info on index funds and expense ratios has been very illuminating. ETF's typically have lower expense ratios than mutual funds. Your expense ratios look a bit high to me for index funds. They are high period. Most of Vanguard's mutual funds have the same expense ratios a their ETFs; I only deal in ETFs so habitually typed ETF. |

|

|

|

[#7]

Quoted:

Wow, that's outstanding. Part of the problem for me though is that the only other vendor I can roll my 403(b) into is Fidelity. I think I can transfer the IRA anywhere I want because it's not a part of the plan. I'll have to look at Vanguard; those expense ratios are unbelievable. I'm reading through the Bogleheads' Guide to Investing right now, and their info on index funds and expense ratios has been very illuminating. Quoted:

Quoted:

Vanguard has very low if not the lowest expense ratios in the industry. And yes, by rolling over to Vanguard, Fidelity or whomever you choose, you can create an essentially identical portfolio with much lower costs. The management fee for Vanguard's S&P500 ETF, for example, is 0.05%. Most are in the 0.10-0.15% range. Wow, that's outstanding. Part of the problem for me though is that the only other vendor I can roll my 403(b) into is Fidelity. I think I can transfer the IRA anywhere I want because it's not a part of the plan. I'll have to look at Vanguard; those expense ratios are unbelievable. I'm reading through the Bogleheads' Guide to Investing right now, and their info on index funds and expense ratios has been very illuminating. Why are you restricted to Fidelity? I'm not a 403(b) expert (never had one) but that doesn't sound right to me, but in any case, Fidelity should have competitive expense ratios. Vanguard's keystone is their low expense ratios, so as stated, they are among if not the lowest, but there are others who are trying to match them. |

|

|

|

[#8]

Quoted:

Wow, that's outstanding. Part of the problem for me though is that the only other vendor I can roll my 403(b) into is Fidelity. I think I can transfer the IRA anywhere I want because it's not a part of the plan. I'll have to look at Vanguard; those expense ratios are unbelievable. I'm reading through the Bogleheads' Guide to Investing right now, and their info on index funds and expense ratios has been very illuminating. Quoted:

Quoted:

Vanguard has very low if not the lowest expense ratios in the industry. And yes, by rolling over to Vanguard, Fidelity or whomever you choose, you can create an essentially identical portfolio with much lower costs. The management fee for Vanguard's S&P500 ETF, for example, is 0.05%. Most are in the 0.10-0.15% range. Wow, that's outstanding. Part of the problem for me though is that the only other vendor I can roll my 403(b) into is Fidelity. I think I can transfer the IRA anywhere I want because it's not a part of the plan. I'll have to look at Vanguard; those expense ratios are unbelievable. I'm reading through the Bogleheads' Guide to Investing right now, and their info on index funds and expense ratios has been very illuminating. Could you roll it to Fidelity then a year later roll it to Vanguard? |

|

|

|

[#9]

Quoted:

Why are you restricted to Fidelity? I'm not a 403(b) expert (never had one) but that doesn't sound right to me, but in any case, Fidelity should have competitive expense ratios. Vanguard's keystone is their low expense ratios, so as stated, they are among if not the lowest, but there are others who are trying to match them. Quoted:

Quoted:

Quoted:

Vanguard has very low if not the lowest expense ratios in the industry. And yes, by rolling over to Vanguard, Fidelity or whomever you choose, you can create an essentially identical portfolio with much lower costs. The management fee for Vanguard's S&P500 ETF, for example, is 0.05%. Most are in the 0.10-0.15% range. Wow, that's outstanding. Part of the problem for me though is that the only other vendor I can roll my 403(b) into is Fidelity. I think I can transfer the IRA anywhere I want because it's not a part of the plan. I'll have to look at Vanguard; those expense ratios are unbelievable. I'm reading through the Bogleheads' Guide to Investing right now, and their info on index funds and expense ratios has been very illuminating. Why are you restricted to Fidelity? I'm not a 403(b) expert (never had one) but that doesn't sound right to me, but in any case, Fidelity should have competitive expense ratios. Vanguard's keystone is their low expense ratios, so as stated, they are among if not the lowest, but there are others who are trying to match them. The only two vendors through which the non-profit my wife works at are TIAA-CREF and Fidelity. On TIAA, when I go to initiate a transfer, the only option I can select from the dropdown is Fidelity. |

|

|

|

[#10]

Quoted:

The only two vendors through which the non-profit my wife works at are TIAA-CREF and Fidelity. On TIAA, when I go to initiate a transfer, the only option I can select from the dropdown is Fidelity. Ahhh, got it: you're talking transfer not rollover (one is only eligible for a rollover once you are no longer employed by the employer with which you have the plan...at that point you can roll it over to anyone). In that case, are you restricted to certain Fidelity funds? Fidelity probably has over 100 funds to choose from but I would hazard to guess that all of them are less expensive than the other funds you posted. As stated, you can recreate your current portfolio (or modify accordingly) at Fidelity for significantly reduced management fees. When your wife does leave that particular employer you can leave it in the 403(b) at Fidelity or roll it over to an IRA at Fidelity if you want to invest in Fidelity funds not available through her now former plan. |

|

|

|

[#11]

Quoted:

Ahhh, got it: you're talking transfer not rollover (one is only eligible for a rollover once you are no longer employed by the employer with which you have the plan...at that point you can roll it over to anyone). In that case, are you restricted to certain Fidelity funds? Fidelity probably has over 100 funds to choose from but I would hazard to guess that all of them are less expensive than the other funds you posted. As stated, you can recreate your current portfolio (or modify accordingly) at Fidelity for significantly reduced management fees. When your wife does leave that particular employer you can leave it in the 403(b) at Fidelity or roll it over to an IRA at Fidelity if you want to invest in Fidelity funds not available through her now former plan. Quoted:

Quoted:

The only two vendors through which the non-profit my wife works at are TIAA-CREF and Fidelity. On TIAA, when I go to initiate a transfer, the only option I can select from the dropdown is Fidelity. Ahhh, got it: you're talking transfer not rollover (one is only eligible for a rollover once you are no longer employed by the employer with which you have the plan...at that point you can roll it over to anyone). In that case, are you restricted to certain Fidelity funds? Fidelity probably has over 100 funds to choose from but I would hazard to guess that all of them are less expensive than the other funds you posted. As stated, you can recreate your current portfolio (or modify accordingly) at Fidelity for significantly reduced management fees. When your wife does leave that particular employer you can leave it in the 403(b) at Fidelity or roll it over to an IRA at Fidelity if you want to invest in Fidelity funds not available through her now former plan. I apologize. I was using incorrect terminology. I think I still have the booklet that includes which funds are available, so I'll just check that and see what the expense ratios are. Thanks for all of your help. |

|

|

|

[#12]

There is nothing wrong with Fidelity. Use their Spartan Index funds if available in the 403b.

Fidelity actually beats Vanguard on a few funds when it comes to Expense Ratios, I personally have my IRA at Vanguard, but I wouldn't flinch at moving it to Fidelity if anything were to make me inclined to leave. |

|

|

Win a FREE Membership!

Win a FREE Membership!

Sign up for the ARFCOM weekly newsletter and be entered to win a free ARFCOM membership. One new winner* is announced every week!

You will receive an email every Friday morning featuring the latest chatter from the hottest topics, breaking news surrounding legislation, as well as exclusive deals only available to ARFCOM email subscribers.

AR15.COM is the world's largest firearm community and is a gathering place for firearm enthusiasts of all types.

From hunters and military members, to competition shooters and general firearm enthusiasts, we welcome anyone who values and respects the way of the firearm.

Subscribe to our monthly Newsletter to receive firearm news, product discounts from your favorite Industry Partners, and more.

Copyright © 1996-2024 AR15.COM LLC. All Rights Reserved.

Any use of this content without express written consent is prohibited.

AR15.Com reserves the right to overwrite or replace any affiliate, commercial, or monetizable links, posted by users, with our own.